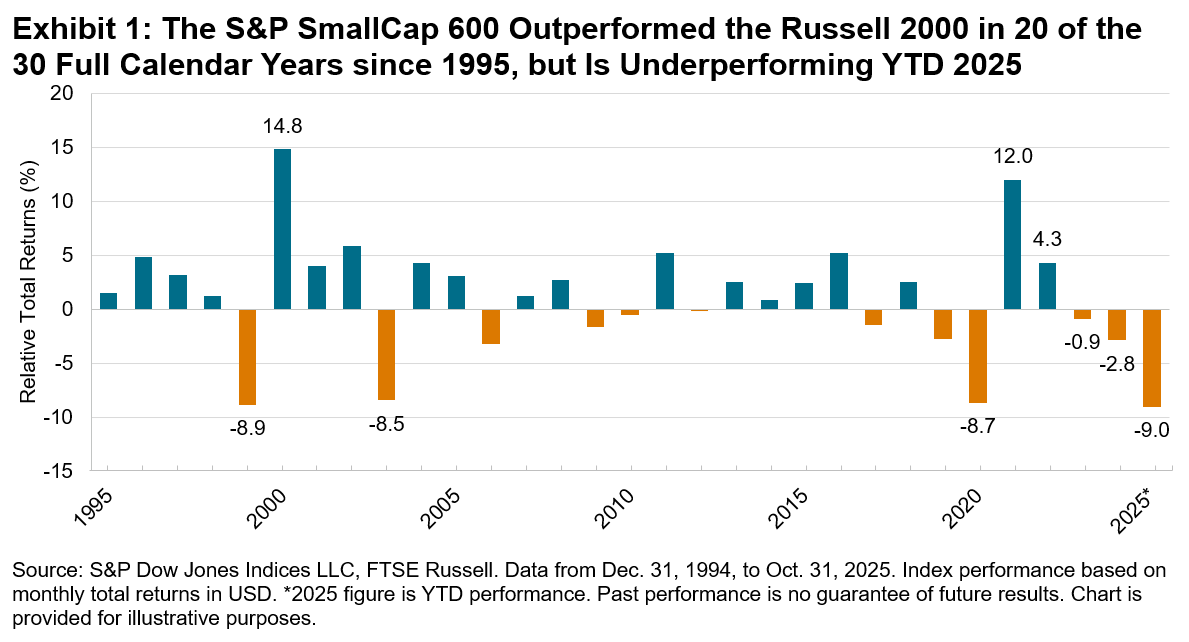

Prior to the start of 2025, the S&P SmallCap 600® outperformed the Russell 2000—another prominent small-cap U.S. equity index—in 20 of the full calendar years to December 2024. However, the S&P SmallCap 600 has underperformed the Russell 2000 by 9% YTD, putting it on track to record its worst year of relative performance since its launch in October 1994 (see Exhibit 1). This reversal reflects an unusual market phase in which quality has fallen out of favor and risk appetite has grown, fueling what could be described as a “junk rally.”1

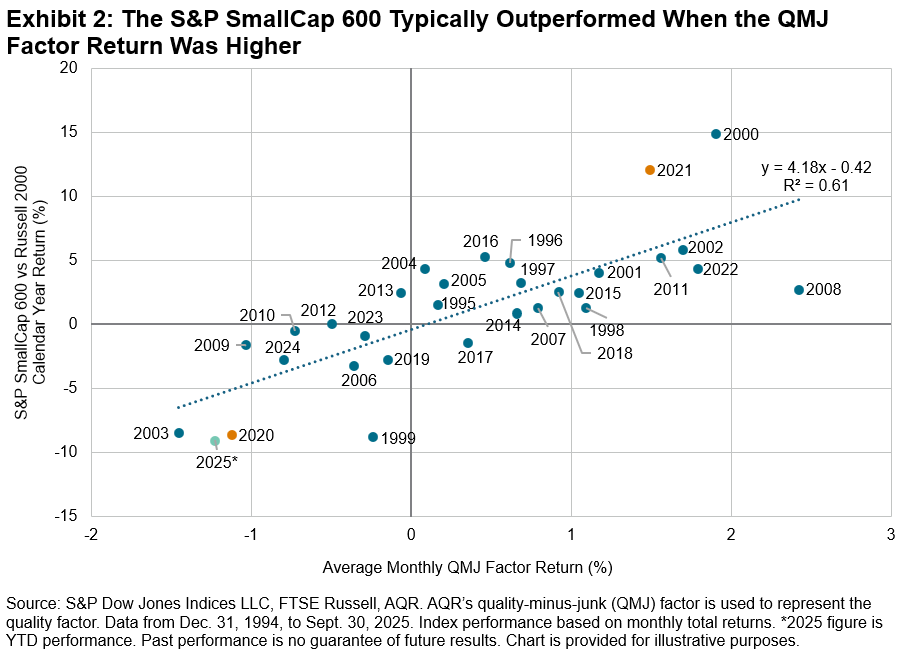

Historically, the S&P SmallCap 600’s quality-by-design construction has contributed to its outperformance.2 Unlike the Russell 2000, new additions to the S&P SmallCap 600 must have a history of positive earnings,3 giving the index a statistically significant tilt toward the quality factor. Exhibit 2 shows that this helped to explain the S&P SmallCap 600’s relative performance: the S&P SmallCap 600 typically outperformed the Russell 2000 by a greater amount in years when the average monthly quality-minus-junk (QMJ) factor performance was higher.

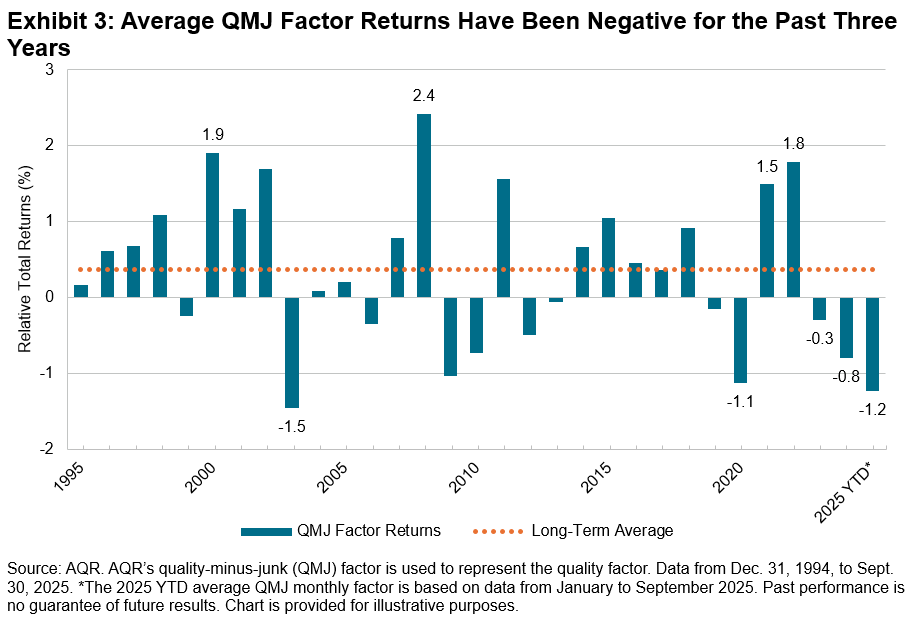

However, the performance associated with quality has been lower in recent times. Over the past three years, average monthly QMJ returns were negative (see Exhibit 3) as investor sentiment rotated toward the lower-quality segment of the market. This shift appears to have created headwinds for the S&P SmallCap 600 whose quality tilt limited its weight in the most speculative performers, potentially driving the Russell 2000’s recent performance gains.

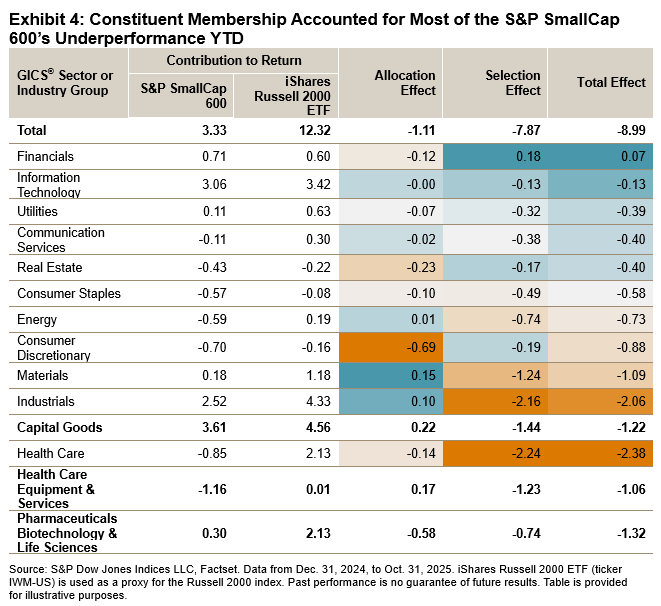

A Brinson performance attribution sheds further light on the S&P SmallCap 600’s underperformance so far in 2025. Constituent membership accounted for most of the index’s lag, with four industry groups of Materials, Health Care and Industrials collectively contributing -4.7% to the total effect (see Exhibit 4). In each of these sectors, the attribution suggests that leadership came from companies excluded from the S&P SmallCap 600 due to weaker fundamentals or inconsistent profitability.

A similar pattern emerged during the COVID-19 pandemic, when sharp shifts in sentiment and rapid rebounds disproportionately rewarded lower-quality companies.4 In those episodes, the S&P SmallCap 600’s earnings screen also limited weight in the most speculative names driving performance, creating short-lived performance gaps versus the Russell 2000 (see Exhibit 2). When market sentiment later rebounded in 2021 toward a preference for profitability, the S&P SmallCap 600 recovered more strongly than its peer index. Recent shifts toward higher-risk, lower-quality stocks reflect comparable swings in relative performance between the two indices.

In summary, the S&P SmallCap 600’s relative performance so far in 2025 highlights the importance of index construction and its impact on index characteristics. In a market driven by risk over quality, it is somewhat unsurprising that the S&P SmallCap 600’s significant quality tilt did not prove to be a tailwind. Yet, history reminds us of the potential outperformance effects of incorporating an earnings screen to distinguish between small companies that have never posted positive earnings and those that have.5

The author would like to thank Cristopher Anguiano for his contributions to this blog.

1 “It’s a junk rally.” Financial Times. Oct. 29, 2025.

2 See Anguiano, Cristopher. “Quality by Design: A Deep Dive into the S&P SmallCap 600.” S&P Dow Jones Indices. July 30, 2025.

3 For full details of the S&P SmallCap 600 Index methodology, please see S&P U.S. Indices Methodology. For full details of the Russell 2000 methodology, please see Russell US Equity Indexes.

4 See Preston, Hamish. “S&P SmallCap 600: A Pandemic Case Study.” S&P Dow Jones Indices. Jan. 26, 2022.

5 See Preston, Hamish. Fei Wang and Sherifa Issifu. “Celebrating 30 Years of the S&P SmallCap 600®.” S&P Dow Jones Indices. Oct. 31, 2024.

The posts on this blog are opinions, not advice. Please read our Disclaimers.