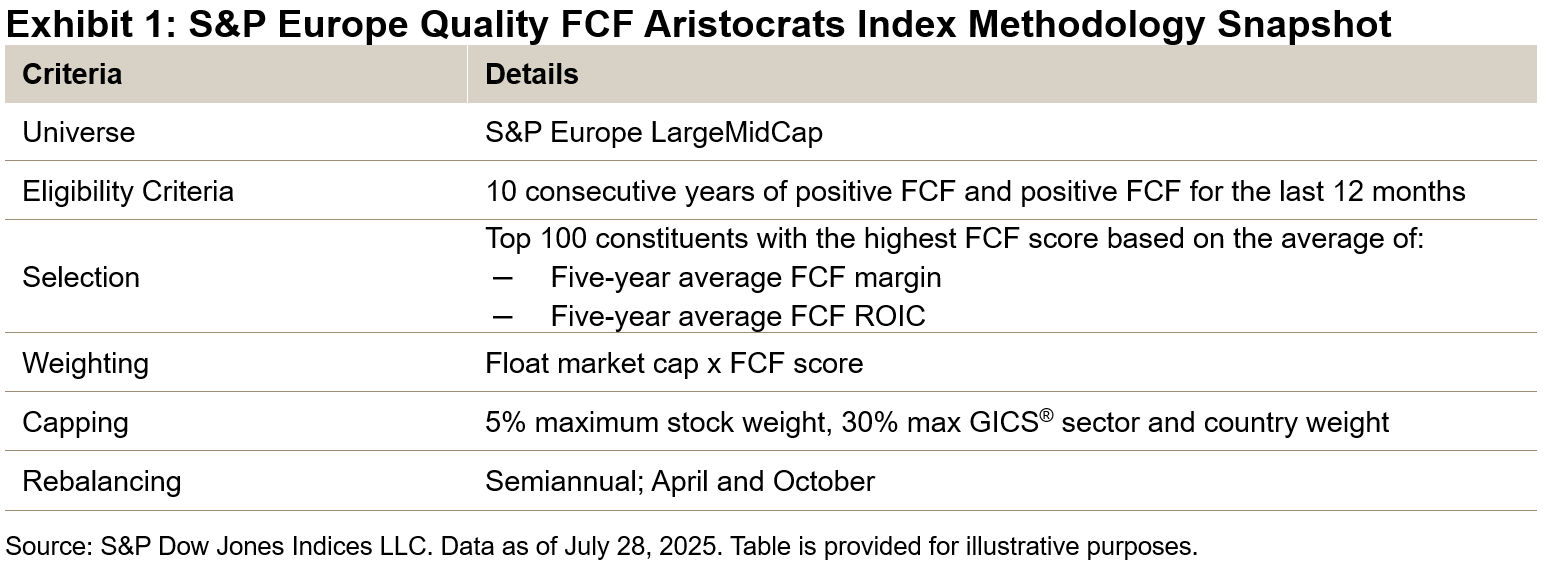

The S&P Europe Quality FCF Aristocrats® Index introduces the quality free cash flow (FCF) methodology to the European region. The index methodology selects high quality companies in the S&P Europe LargeMidCap universe that emphasize consistent and efficient free cash flow (FCF) generation.1 Our recent education paper explores the use of FCF metrics in creating indices with quality factor characteristics.

As with the existing S&P Quality FCF Aristocrats Indices, the new European index starts by selecting those companies that have 10 years of positive FCF generation, including positive FCF for the last 12 months. The constituents are then selected using the FCF score metrics, FCF ROIC and FCF margin, and weighted by float market cap multiplied by FCF score.

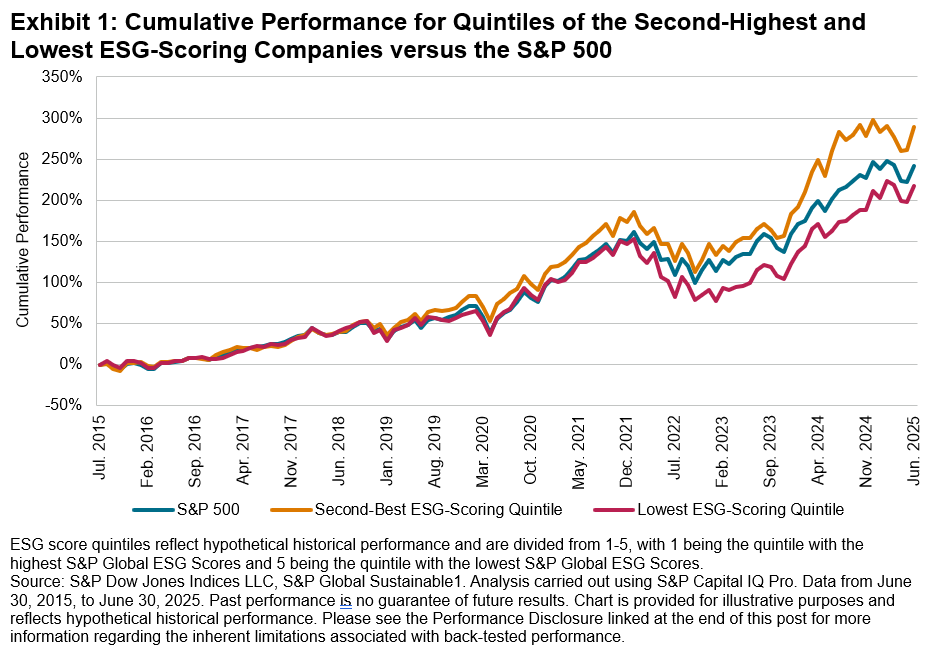

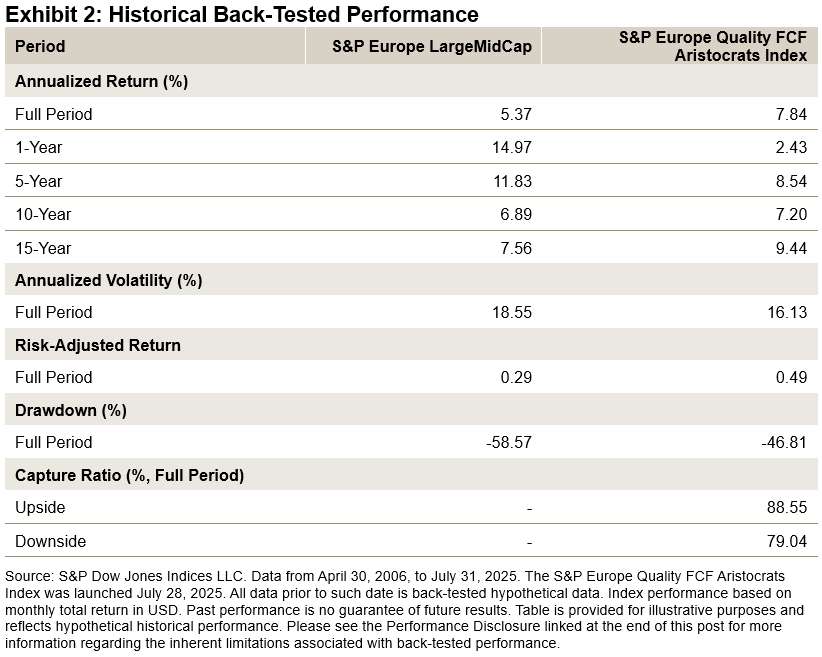

Over the long term back-tested period, the index outperformed its benchmark by 150 bps since April 30, 2006, while also demonstrating lower volatility with reduced drawdowns. The historical capture ratio also demonstrates the index’s upside potential with defensiveness against downside risk.

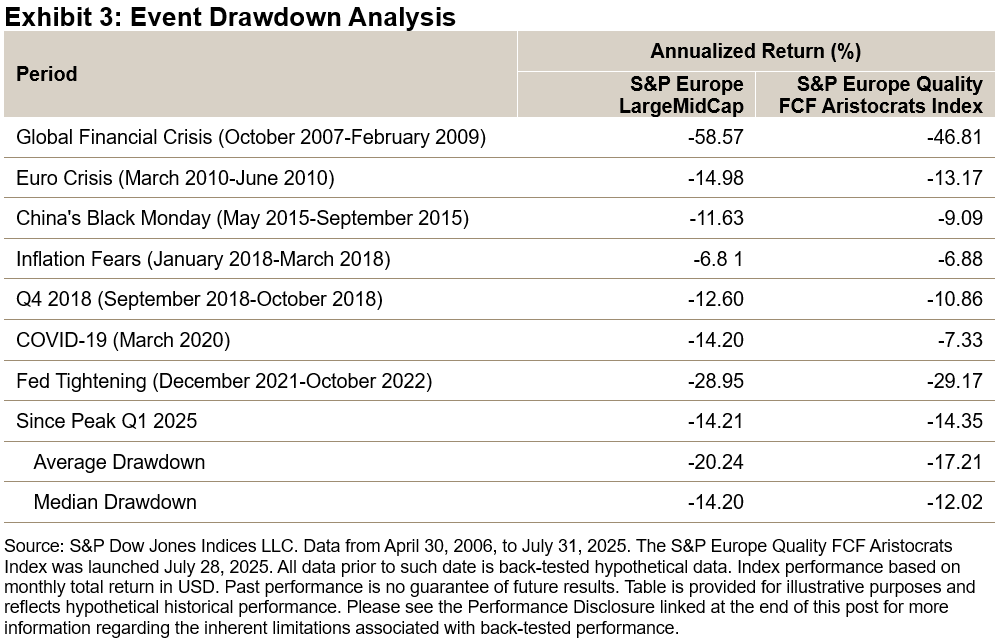

Over the period studied, in the majority of cases when the market saw large drawdowns, the S&P Europe Quality FCF Aristocrats Index saw a lower drawdown than the benchmark. The most noticeable of these was during the onset of COVID-19 when the index only matched approximately 50% of the market fall realized by the benchmark.

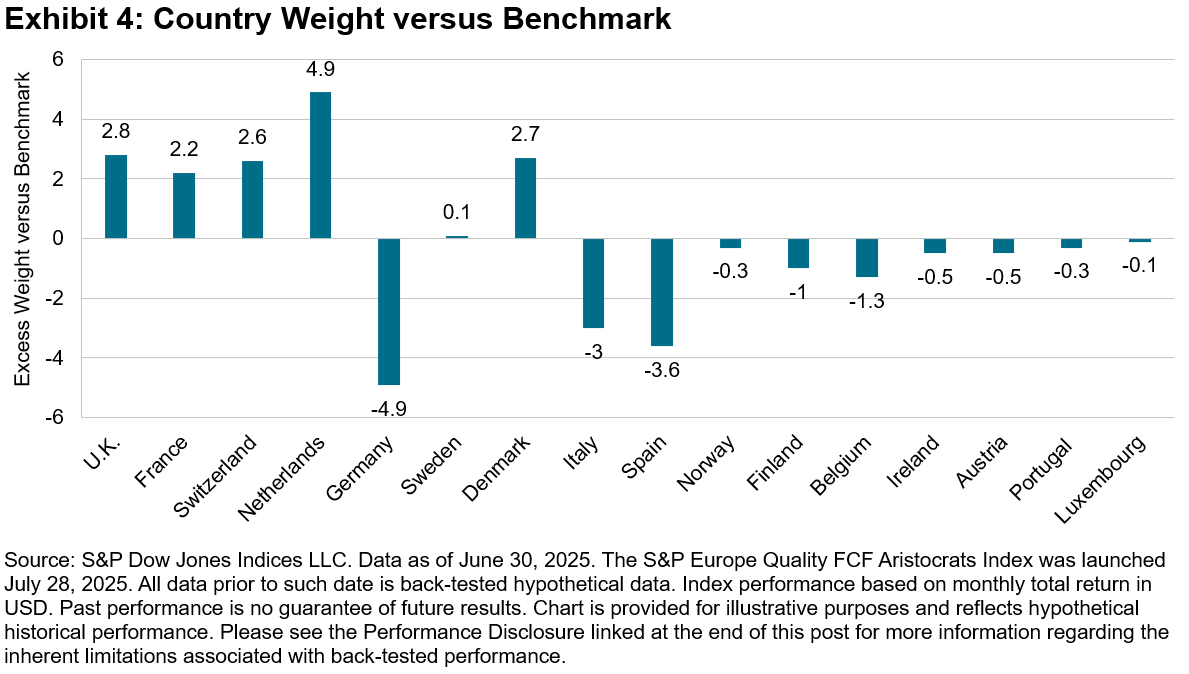

As of the most recent rebalance, the index had higher tilts toward the U.K., Switzerland, Denmark and the Netherlands compared to the benchmark, which has more weight in Germany and Southern European markets.

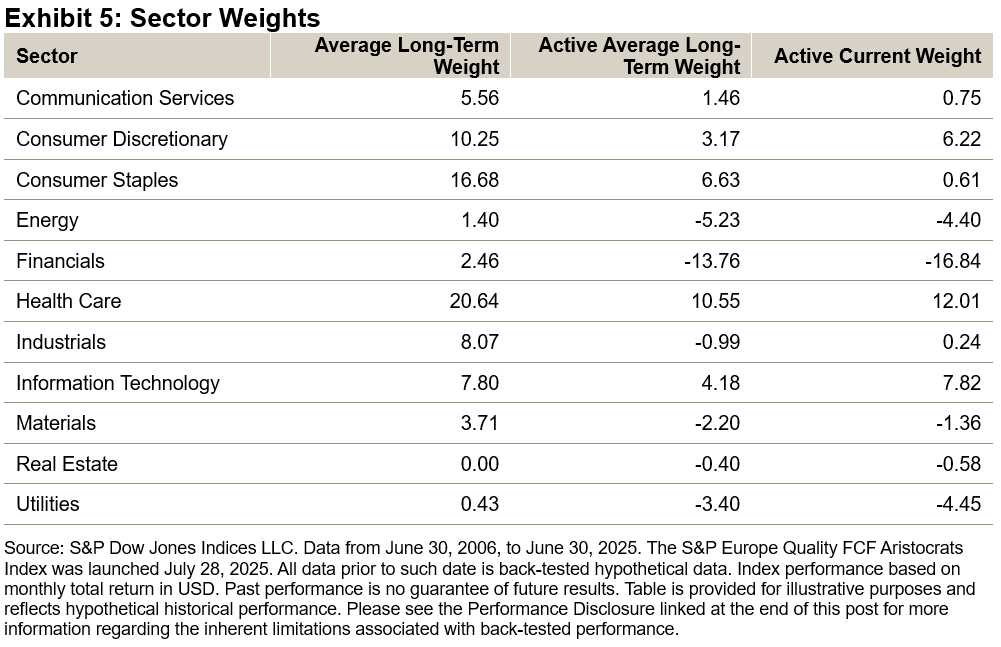

Active sector weights are shown in Exhibit 5. Historically, there were higher allocations on average to Health Care, Consumer Staples, Consumer Discretionary and Information Technology, with a significant tilt away from Financials and Energy.

More recently, the weights in Consumer Discretionary and Information Technology increased significantly, showing higher weights compared to the benchmark. Meanwhile, the weights to the Consumer Staples and Health Care sectors decreased. Underweights in Financials2 and Energy remained significant.

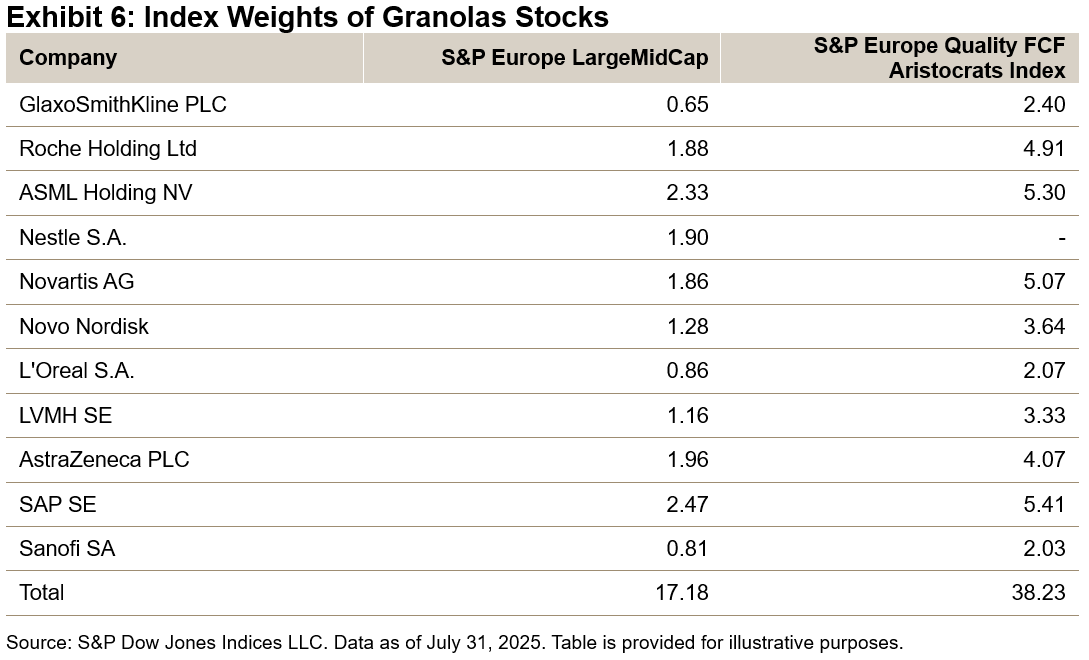

The Magnificent 7 stocks have been the topic of much discussion for their impact on the S&P 500. In Europe, the 11 companies that have led market performance are known as the “Granolas.” The index has representation in almost all these companies (excluding Nestlé) and has more than double the weight of the underlying benchmark, recognizing the high FCF scores and quality of these companies over the long term (see Exhibit 6).

The S&P Europe Quality FCF Aristocrats Index is the newest addition to the S&P Aristocrats Index Suite. This regional index has demonstrated a strong quality tilt across its back-tested history, providing a benchmark that uses FCF as proxy for long-term quality in the European market.

1 The S&P 500® Quality FCF Aristocrats Index and S&P Developed Quality FCF Aristocrats Index were both launched in December 2024.

2 Some Financials stocks are excluded due to the availability of metrics (see methodology). All Real Estate sector constituents are excluded.

The posts on this blog are opinions, not advice. Please read our Disclaimers.