In a previous analysis, we examined the S&P MidCap 400® Scored & Screened Index, derived from the S&P MidCap 400 broad market benchmark. The S&P MidCap 400 Scored & Screened Index showed key characteristics such as lower concentration compared to the S&P 500®, as well as similar industry weights to the S&P MidCap 400.

In this analysis, we turn our attention to a new sustainability benchmark for the mid-cap segment—the S&P MidCap 400 Scored & Screened Leaders Index—and highlight its key features.

Launched on April 9, 2025, the S&P MidCap 400 Scored & Screened Leaders Index measures the performance of securities with higher-than-average ESG scores, while excluding companies deriving revenue from specified business activities or that are non-compliant with United Nations Global Compact.1

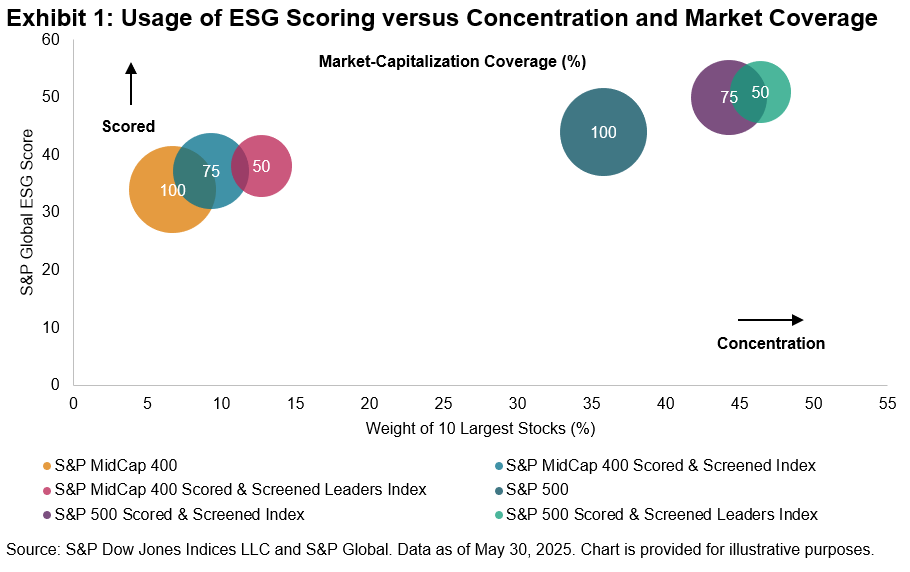

Exhibit 1 summarizes the relationship between the usage of ESG scores, concentration and market-capitalization coverage for various indices in the mid- and large-cap segments, as of May 30, 2025. References to “Scored” below and in the index name indicate the use of S&P Global ESG Scores to select index constituents, while concentration (measured on the x-axis) is based on the total weight of the top 10 largest stocks in each index. The size of the bubbles reflects the market-capitalization coverage.

From Exhibit 1, we observe that the mid-cap indices showed relatively lower concentration compared to the S&P 500®-based indices—this pattern was also identified in our previous analysis. Specifically, the S&P MidCap 400 Scored & Screened Leaders Index had a concentration of 12.7% for its 10 largest stocks, the highest among the mid-cap indices, but also distinctly lower than the 46.4% concentration of the S&P 500 Scored & Screened Leaders Index.

Furthermore, the exhibit reveals that as concentration increased, ESG scores tended to rise, while market-capitalization coverage decreased.

The S&P MidCap 400 Scored & Screened Leaders Index achieved the highest ESG score among the mid-cap indices at 38.1, compared to the S&P MidCap 400’s score of 34.0. However, it also exhibited the lowest market-capitalization coverage of 50%.

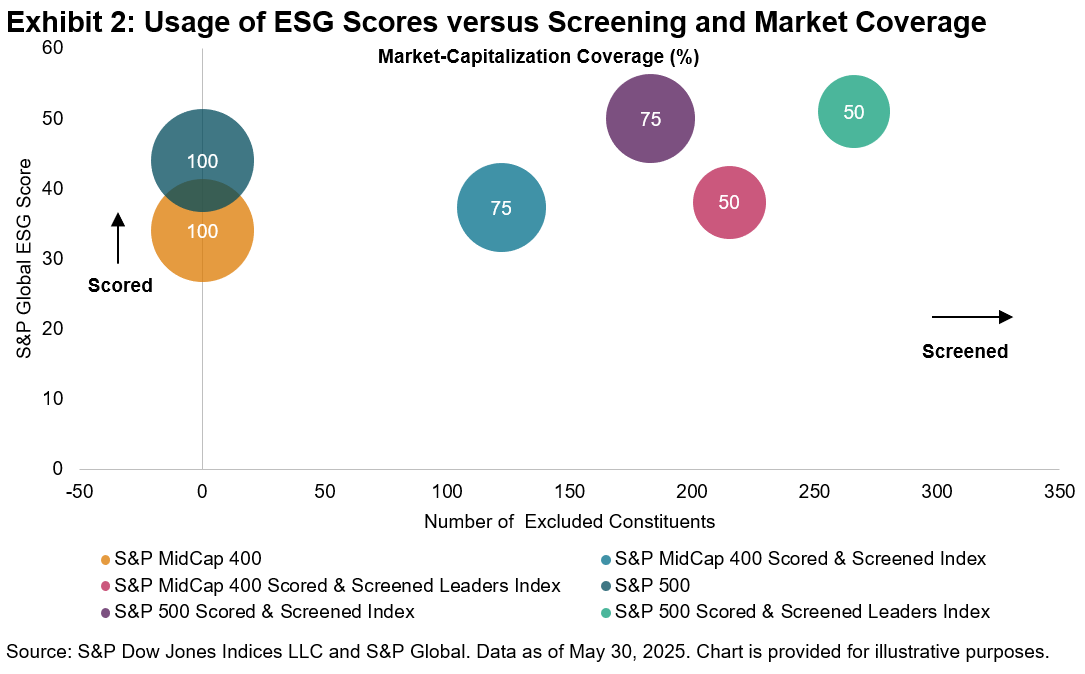

Exhibit 2 further explores this relationship by analyzing the connection between ESG scores, market-capitalization coverage and the number of excluded constituents for each index. References to “Screened” below and in the index name refer to those constituents excluded based on specific eligibility criteria. In this case, the S&P MidCap 400 Scored & Screened Leaders Index stood out among the mid-cap indices with the highest number of exclusions, at 215, in contrast to just 122 for the S&P MidCap 400 Scored & Screened Index. This large number of exclusions aligns with its construction methodology, which aims to measure the performance of securities that meet stricter ESG criteria.

In summary, Exhibits 1 and 2 together show that the S&P MidCap 400 Scored & Screened Leaders Index not only aligns with key characteristics of the S&P MidCap 400—like maintaining lower concentration compared to the S&P 500—but also includes constituents that exhibit stronger-than-average ESG characteristics as measured by S&P Global ESG Scores.

1See the S&P Scored & Screened Leaders Indices Methodology.

The posts on this blog are opinions, not advice. Please read our Disclaimers.