Utilizing free cash flow (FCF) to evaluate a company’s quality can be a powerful way to identify financially resilient businesses. Unlike earnings, which can be influenced by accounting practices, FCF provides a clearer picture of a company’s ability to generate cash after covering essential expenses and investments.

In our paper published this year, we demonstrated this approach with large-cap companies using the S&P 500®. In the mid- and small-cap spaces, where earnings can be more volatile and transparency may be lower, using FCF may be even more valuable to help identify businesses with sustainable growth while offering stronger potential downside protection.

As of July 28, 2025, S&P DJI expanded the S&P Quality FCF Aristocrats® Index Series to include the S&P MidCap 400® Quality FCF Aristocrats Index and the S&P SmallCap 600® Quality FCF Aristocrats Index. In this blog, we will explore the design, performance, and sector and factor characteristics of these indices, alongside the S&P 500® Quality FCF Aristocrats Index.

Index Design

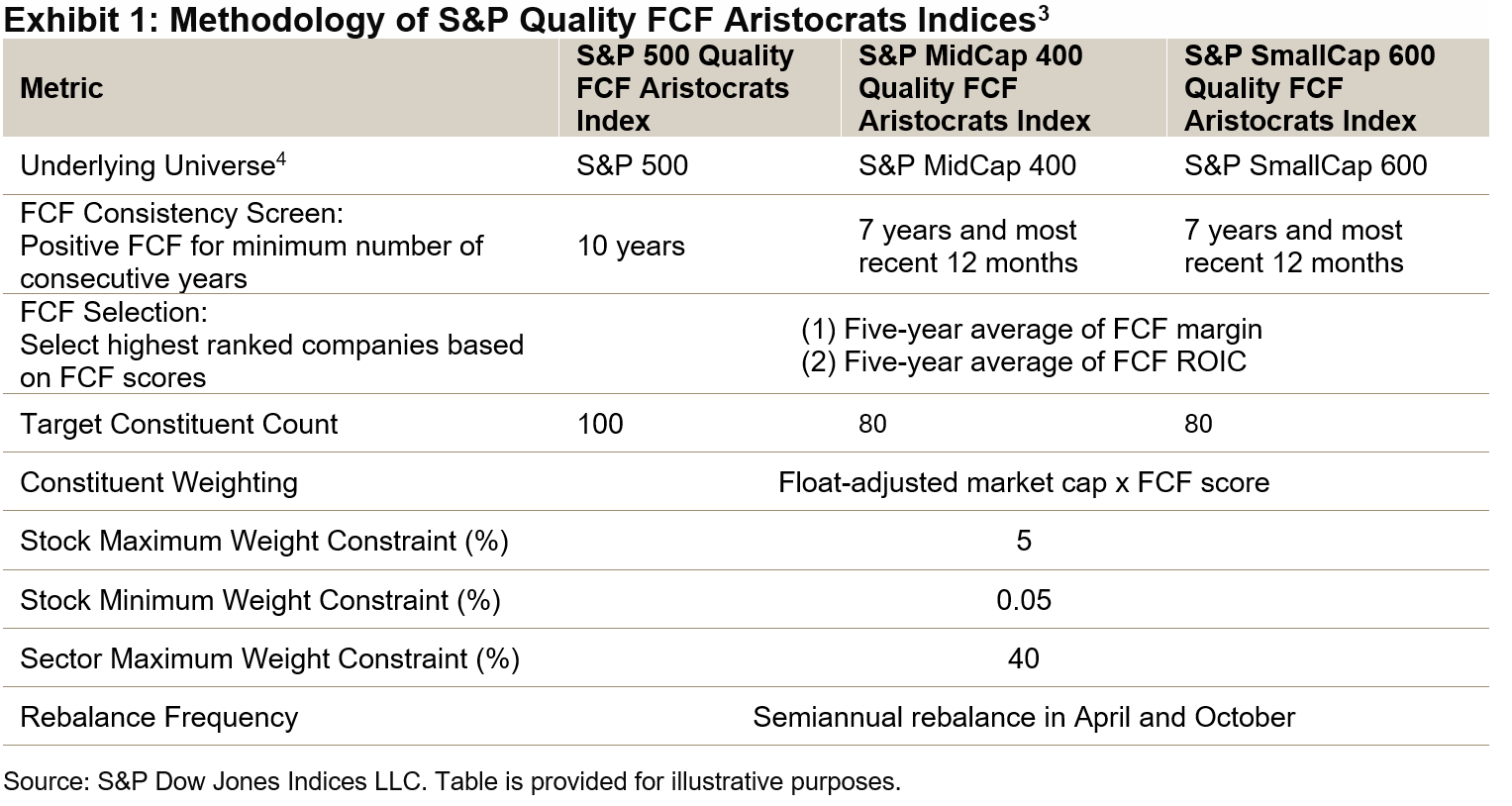

The S&P Quality FCF Aristocrats Indices highlight high-quality companies by focusing on the consistency and efficiency of FCF generation. To qualify, companies must first demonstrate a minimum number of consecutive years of positive FCF. From this subset, the top constituents are selected based on the average of their FCF margin1 and FCF return on invested capital (ROIC).2 These constituents are then weighted by their float market cap multiplied by their FCF score (see Exhibit 1).

Performance Comparison

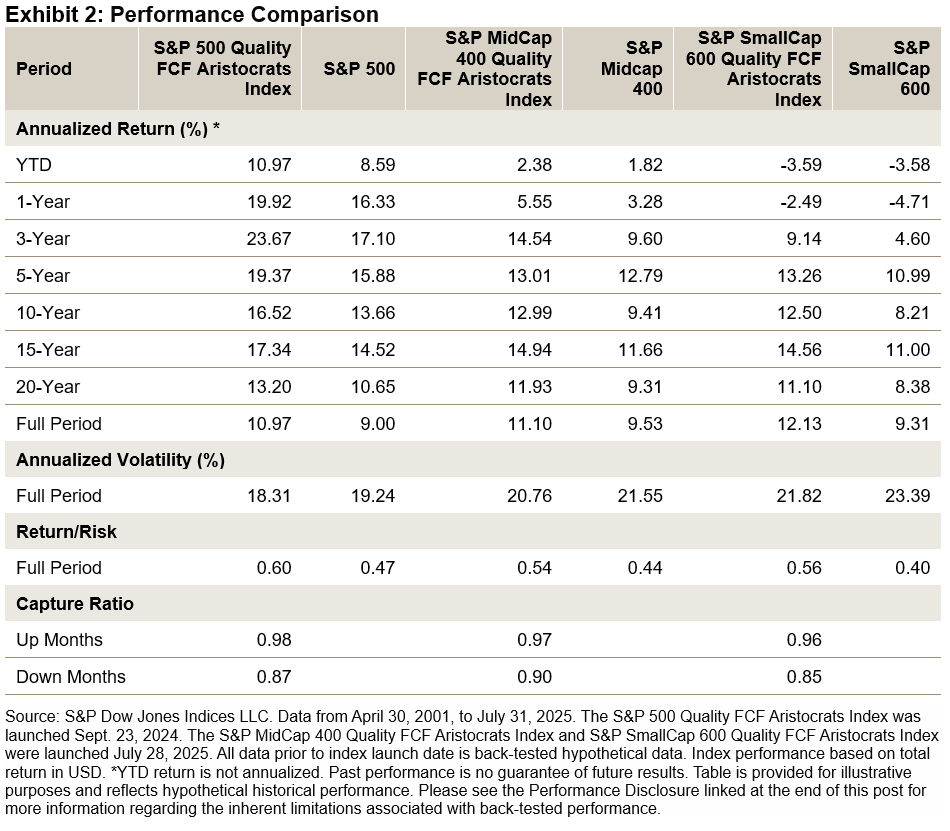

Historically, the S&P Quality FCF Aristocrats Indices have outperformed their respective underlying benchmarks across all market capitalizations, outperforming on both a total return and risk-adjusted return basis while exhibiting reduced volatility over short- and long-term horizons (see Exhibit 2).

Importantly, each of these indices exhibits consistent capture ratios relative to their benchmark universes, achieving nearly one-for-one participation in up markets while outperforming in down markets. This highlights the historical effectiveness of this framework and its ability to identify companies with quality growth potential and resilient characteristics across market cap segments.

Sector Profiles

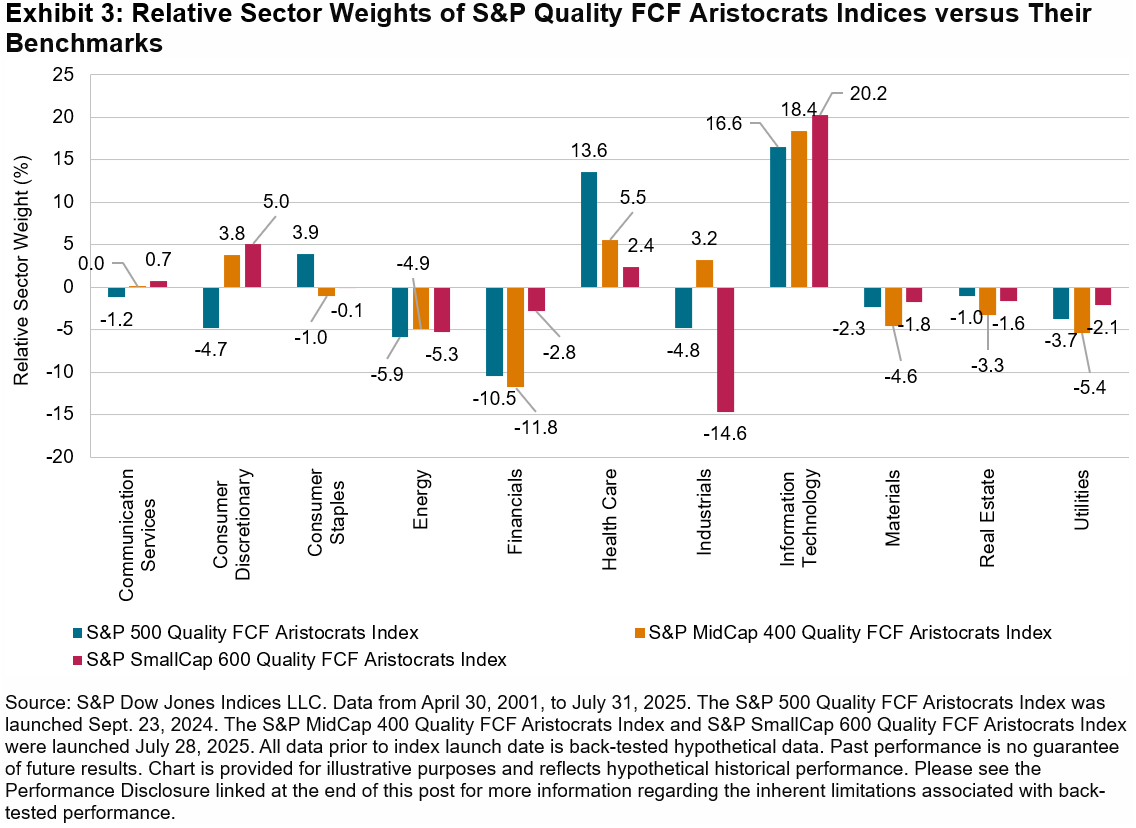

Next, we examine the relative sector weights5 of the S&P Quality FCF Aristocrats Indices in comparison to their corresponding underlying benchmarks. As shown in Exhibit 3, each of the indices has historically maintained a significant overweight in Information Technology, followed by Health Care, while exhibiting a notable underweight in Financials and Energy.

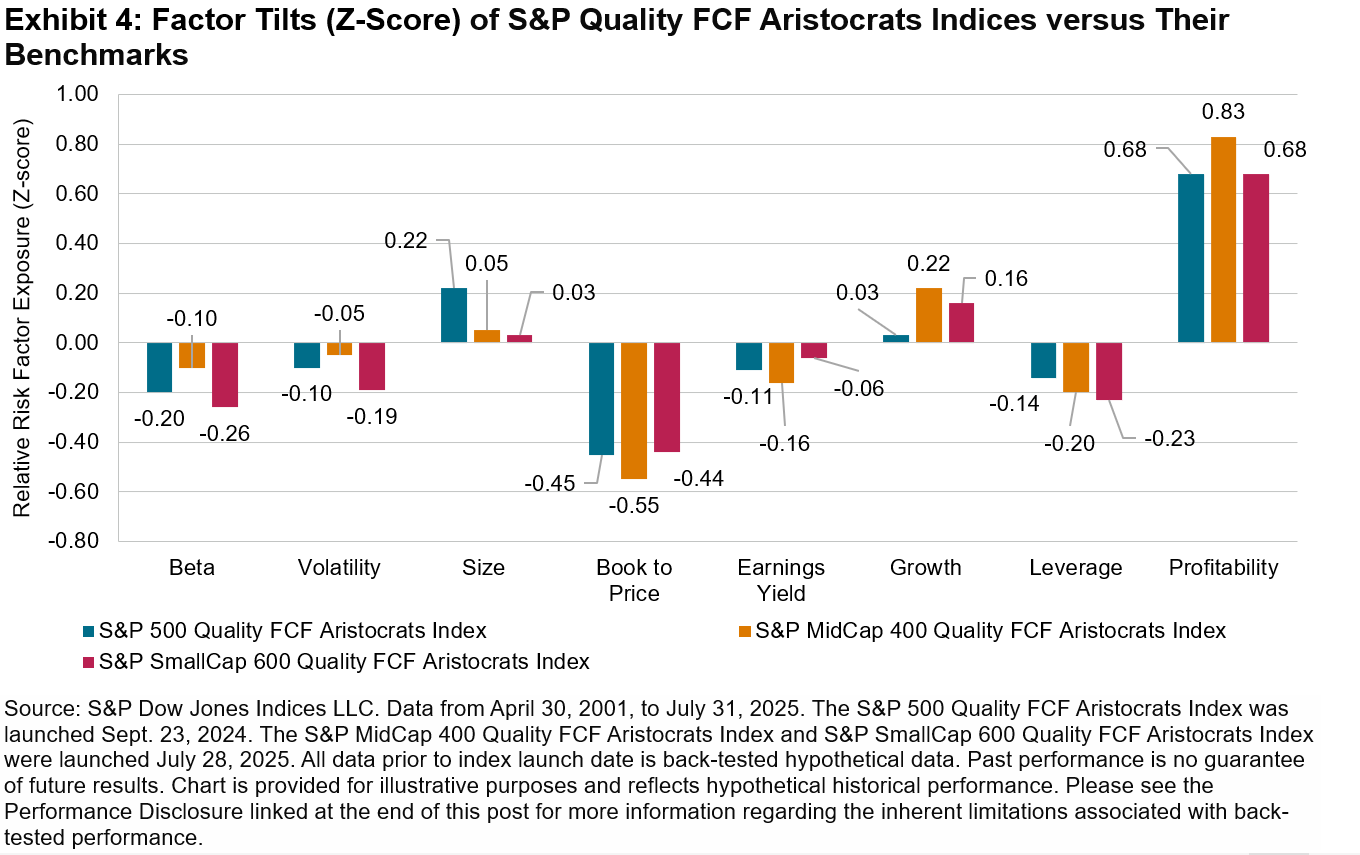

Factor Tilts

Exhibit 4 illustrates the factor tilts of the S&P Quality FCF Aristocrats Indices versus their respective benchmarks in terms of the FactSet Global Risk Model Factor Z-scores. Historically, they have exhibited lower volatility, larger size, higher growth, lower leverage and higher profitability tilts.

Conclusion

FCF serves as a valuable metric for identifying high quality companies across the large-, mid- and small-cap segments. By emphasizing consistent and efficient FCF generation, the S&P Quality FCF Aristocrats Indices offer a robust framework that has historically shown outperformance, defensive characteristics and solid fundamentals across all U.S. market capitalizations.

1 FCF margin is defined as FCF-to-revenue ratio.

2 FCF ROIC is defined as FCF-to-(total debt + equity) ratio.

3 For further details, please refer to S&P Quality FCF Aristocrats Indices Methodology.

4 All stocks classified in the following GICS® categories are not eligible for index inclusion: Real Estate (60), Banks (4010), Insurance (4030), Mortgage Real Estate Investment Trusts (REITs) (402040), Specialized Finance (40201040), Asset Management & Custody Banks (40203010) and Investment Banking & Brokerage (40203020). For more details, please see the index methodology.

5 Relative sector weight = Quality FCF Aristocrats sector weight – corresponding benchmark sector weight

The posts on this blog are opinions, not advice. Please read our Disclaimers.