The growing adoption of model portfolios among wealth managers has spurred asset managers, home offices and other model providers to expand their offerings. Accessing quality data on underlying indices is essential to model development—and in some cases can be a barrier to product innovation.

A recent whitepaper by Cerulli Associates1 examines the challenges asset managers and home offices face in accessing quality data and highlights the role index providers with expansive, user-friendly data capabilities can play in helping model providers differentiate their offerings.

Why Advisors Are Increasingly Using Models

Many advisors now view financial planning as their primary differentiator, instead of investment management, as their clients are focused more on achieving specific financial goals than outperforming benchmarks.2 As a result, model portfolios have emerged as an efficient way for advisors to outsource portfolio construction and spend more time serving clients and growing their practices.

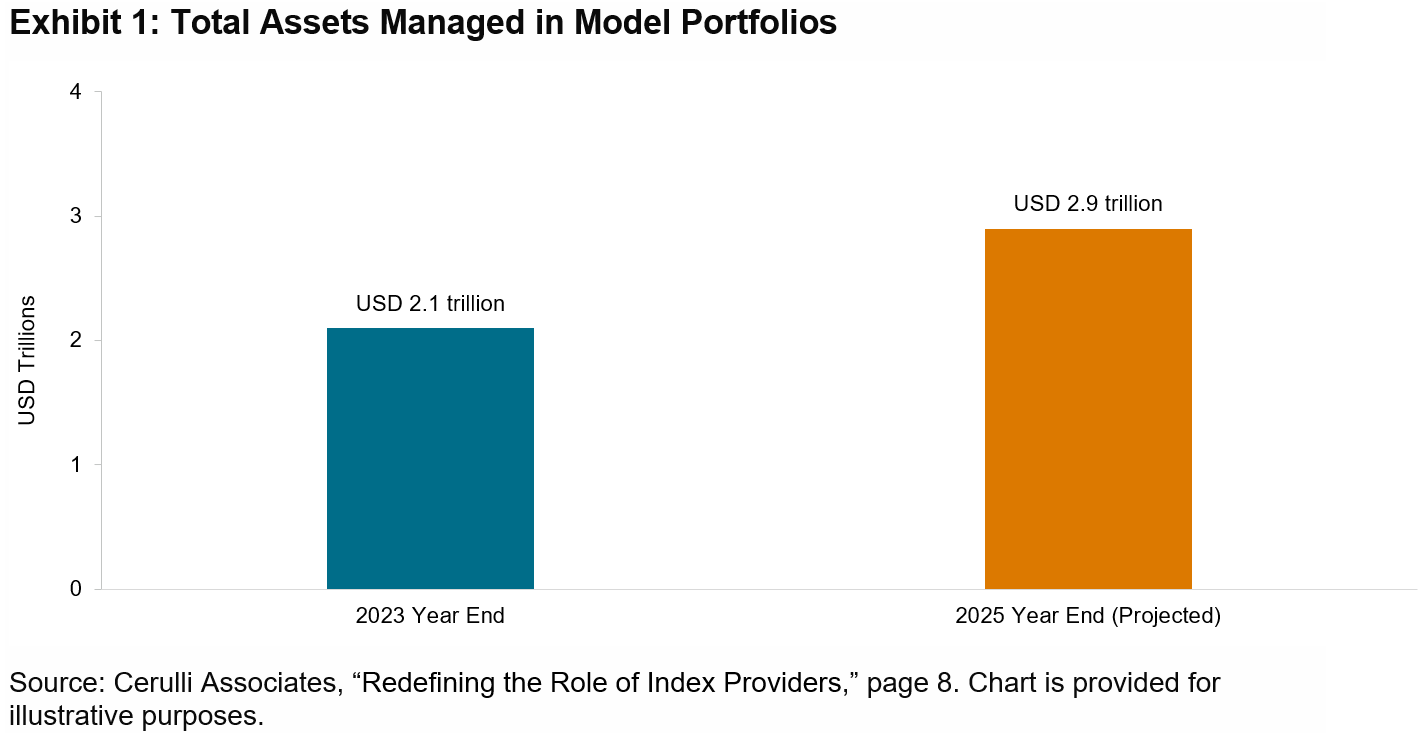

Home offices are encouraging their advisors to incorporate models, as well. Models can help advisors scale their practices by providing a more consistent client experience, centralizing investment decision-making and reducing compliance risks. Cerulli expects these dynamics to drive the amount of assets managed through models to grow to USD 2.9 trillion by the end of 2025, up 38% since 2023.3

Unpacking the Model Data Challenge

As home offices and asset managers seek to expand and differentiate their model platforms, many are working with index providers to source data that is used to develop capital market assumptions and construct models.4

Index providers’ ability to deliver the data that model providers need, however, can vary significantly. To utilize index data effectively in model portfolio construction, Cerulli’s research5 suggests model providers focus on four important factors:

- Quality: Encompassing reliable index performance, attribution analyses and timely rebalancing updates

- Cost-effectiveness: Balancing licensing fees with data utility

- Breadth: Providing comprehensive data across asset classes and geographies

- Ease of use and access: Enabling efficient consumption and processing through effective delivery methods

These last two items are particularly important for model managers to consider as they evaluate organizations to source data from efficiently. Working with index providers that offer comprehensive data across asset classes—including more fragmented markets such as fixed income, international equity and alternatives—may help to streamline model development, eliminate data gaps and reduce the risk of incongruent or overlapping investment data from multiple sources.6

Model providers also need data suppliers who can deliver this information via efficient, user-friendly channels. Managing models requires frequent, seamless data updates to facilitate quick responses to market shifts, and outdated and manual delivery methods can create friction. Cerulli notes that streamlined data intake and tech integration allow model providers to construct portfolios faster, enhancing operational efficiency.7

Collaborating to Enhance Data Intelligence and Delivery

As model portfolio assets rise, model providers can enhance their portfolio construction processes by working with index providers that address data challenges effectively.

Index providers with robust data spanning multiple asset classes and flexible, tech-enabled delivery options are well-positioned to support these needs. Model managers need consistent, timely and reliable data for tracking global financial markets, including comprehensive performance and constituent data. Furthermore, the integration of flexible, tech-enabled delivery options, such as API-driven tools, allows for seamless access to this valuable information, enhancing the ability of model providers to leverage data within their internal systems.

Explore the Cerulli Associates whitepaper “Redefining the Role of Index Providers” for deeper insights on optimizing index data to strengthen model portfolio construction.

1 The Cerulli Associates’ whitepaper “Redefining the Role of Index Providers” was sponsored by S&P Dow Jones Indices. Please see page 2.

2 Please see page 4 of Cerulli Associates’ “Redefining the Role of Index Providers.”

3 Please see page 8 of Cerulli Associates’ “Redefining the Role of Index Providers.”

4 Please see pages 8 and 16 of Cerulli Associates’ “Redefining the Role of Index Providers.”

5 Please see page 16 of Cerulli Associates’ “Redefining the Role of Index Providers.”

6 Please see pages 16–17 of Cerulli Associates’ “Redefining the Role of Index Providers.”

7 Please see page 17 of Cerulli Associates’ “Redefining the Role of Index Providers.”

The posts on this blog are opinions, not advice. Please read our Disclaimers.