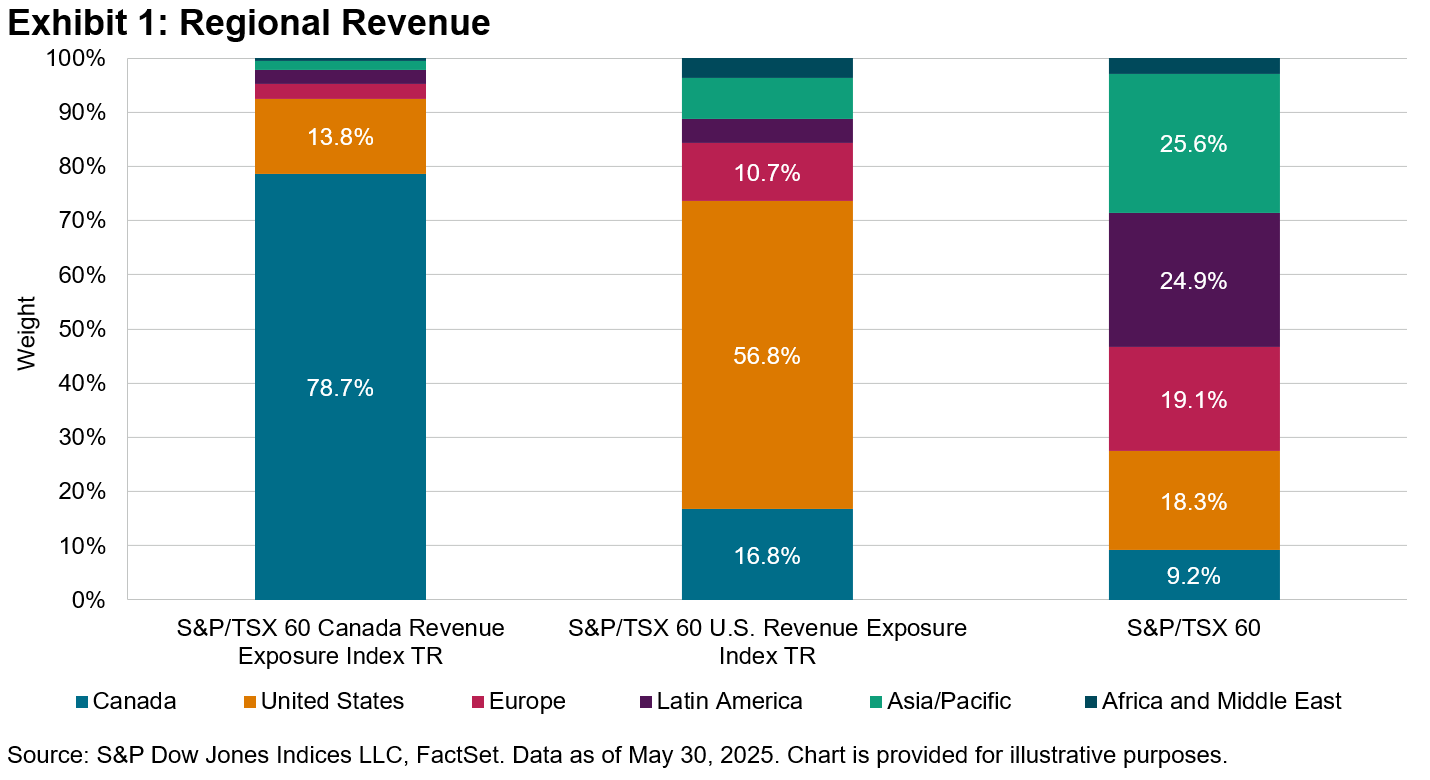

In a globalized economy with tariff policies under the spotlight, understanding where companies generate their revenues has become increasingly important when it comes to asset allocation. The S&P/TSX Geographic Revenue Exposure Indices offer an innovative approach to measuring and tracking Canadian companies based on their revenue sources, whether primarily domestic or international. These indices provide market participants tools to make more informed decisions about their potential geographic exposure, while maintaining exposure to a domestic basket of listed Canadian companies.

As of May 30, 2025, the S&P/TSX 60 Canada Revenue Exposure Index had a strong tilt toward Canadian-sourced revenues, with approximately 78% of its revenue derived domestically. Meanwhile, the benchmark S&P/TSX 60 offered broader global diversification, with contributions from Europe, Asia and emerging markets. These distinctions provide market participants with targeted tools for aligning their regional revenue preferences with their global or domestic investment outlook.

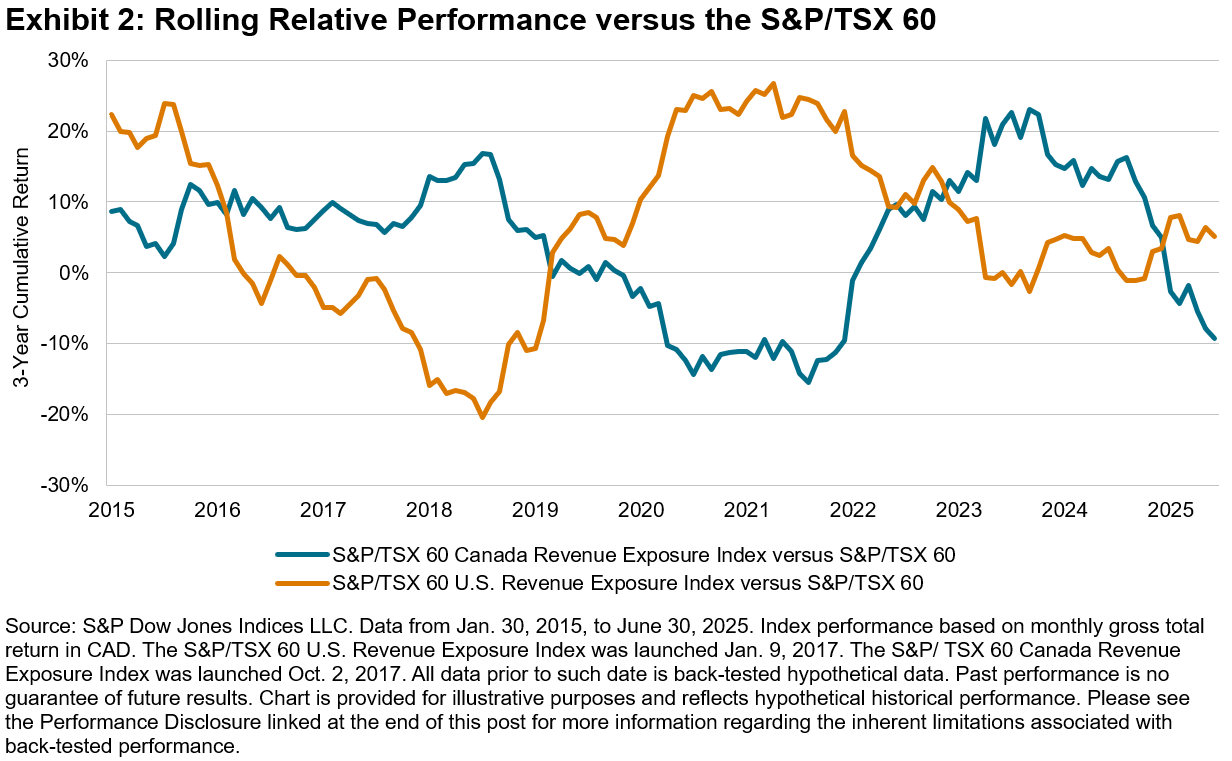

Exhibit 2 highlights the dynamic nature of geographic revenue exposure and its influence on performance relative to the S&P/TSX 60. Over the past decade, the S&P/TSX 60 U.S. Revenue Exposure Index mostly outpaced the benchmark during periods of strong U.S. equity performance—notably during the post-COVID-19 recovery, when U.S.-listed companies with global tech and healthcare exposure rebounded sharply. More recently, shifting trade dynamics and industrial policy developments have begun to alter the landscape, contributing to renewed strength in Canadian revenue exposure. These patterns illustrate how revenue origin can serve as a useful lens through which to analyze index behavior across varying market environments.

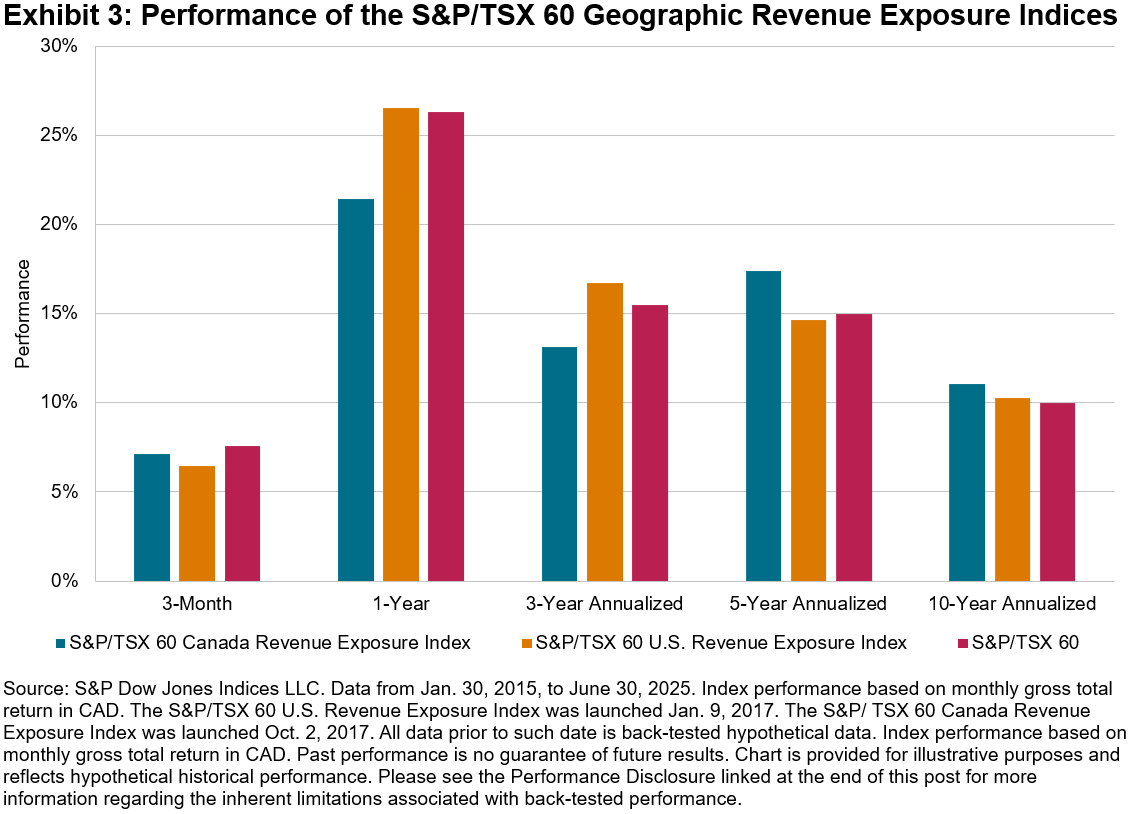

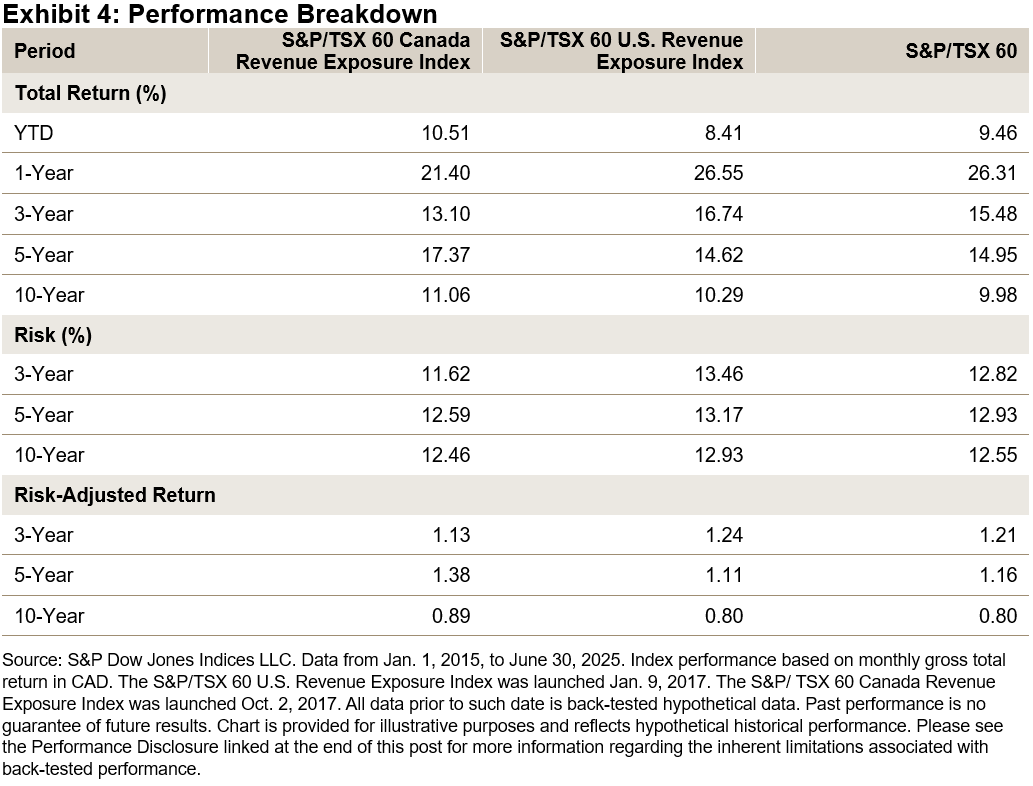

The S&P/TSX 60 U.S. Exposure Index outperformed the benchmark over the past 1- and 3-year periods, albeit with higher volatility, while the S&P/TSX 60 Canada Revenue Exposure Index outperformed over the longer 5- and 10-year periods. These patterns suggest that domestically focused companies may provide more stable long-term returns, while companies with U.S. revenue exposure tend to lead during periods of U.S. market momentum.

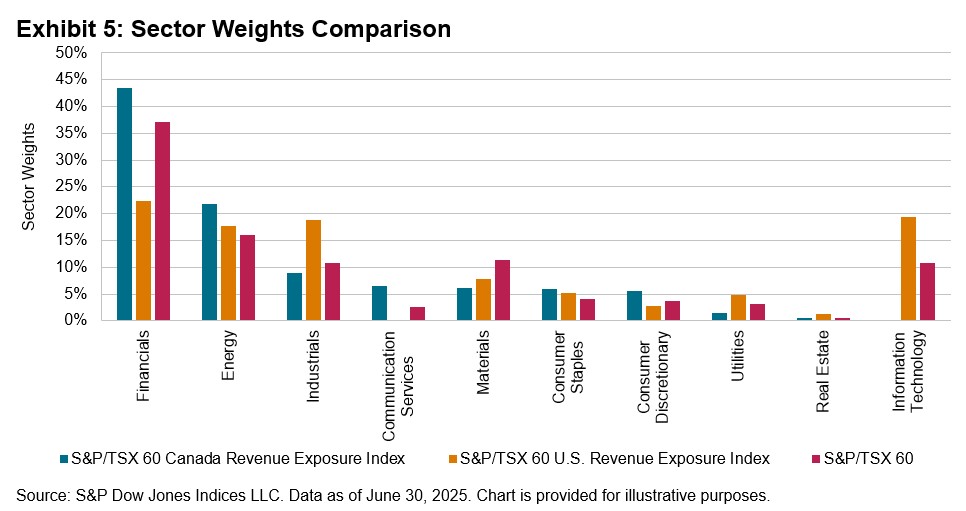

While the S&P/TSX 60 reflects Canada’s large-cap equity landscape, its revenue-based counterparts reveal distinct sector tilts tied to geographic exposure. The S&P/TSX 60 Canada Revenue Exposure Index has leaned heavily into the Financials and Energy sectors, aligning with Canada’s domestic economic strengths. In contrast, the S&P/TSX 60 U.S. Revenue Exposure Index has been weighted more toward the Information Technology and Industrials sectors, which are often linked with international business and global demand.

The S&P/TSX 60 Geographic Revenue Exposure Indices highlight how differing revenue origins shape index characteristics. Global exposure has generally aligned more closely to market momentum shifts, while domestic exposure has tended to reflect long-term economic stability.

The posts on this blog are opinions, not advice. Please read our Disclaimers.