The private equity (PE) industry has experienced a notable shift with a growing wave of high-profile public listings worldwide. This trend traces back to the mid-2000s, with Blackstone being among the first major firms to list its shares on the NYSE. This unlocked an era where industry giants such as KKR and Carlyle followed suit with their own IPOs. A decade later, European PE firms dominated headlines with their own IPOs. This blog explores the trend of public listings within the private markets space and dives into the S&P Listed Private Equity Index as a tool to track and gain insight into this expanding market segment.

Brief History of Private Equity Funds

PE funds invest in private companies through leveraged buyouts, venture and growth capital, using funds raised from limited partners, including institutional investors and high-net-worth individuals. The asset class, characterized by longer capital lock-up periods and limited liquidity, has fostered active ownership with portfolio companies to drive long-term operational enhancements, often outperforming public-market benchmarks.

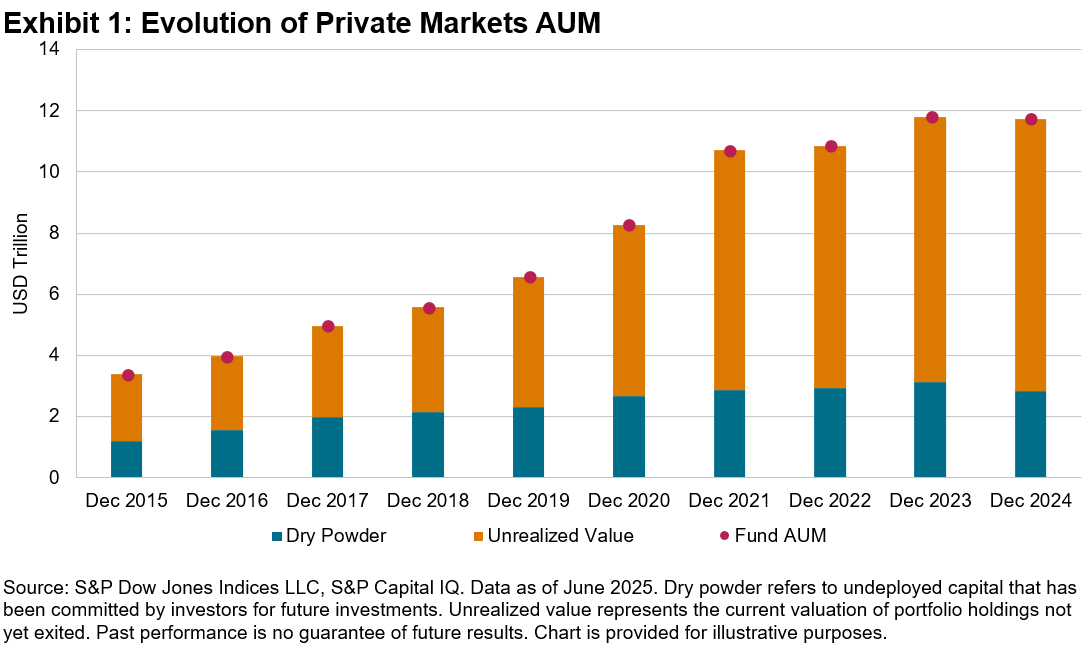

Historically structured as limited partnerships, many private capital firms have transitioned into publicly listed companies to benefit from an influx of long-term capital and access to liquidity; to facilitate founders’ ownership transition; and to enhance brand recognition. This coincides with a broader surge in appetite for this alternative asset class, which has grown to USD 12 trillion in AUM globally (see Exhibit 1).

Indexing Listed Private Markets

Indexing the broader private markets space has been notoriously difficult due to the lack of directly comparable data. Unlike public companies, whose share price can be accessed real-time as a gauge of market sentiment, private assets’ returns are derived from valuations of portfolio holdings, typically assessed on an annual or quarterly basis. However, a more comparable subset emerges through listed private markets companies, which may offer a bridge between private market exposure and public market accessibility.

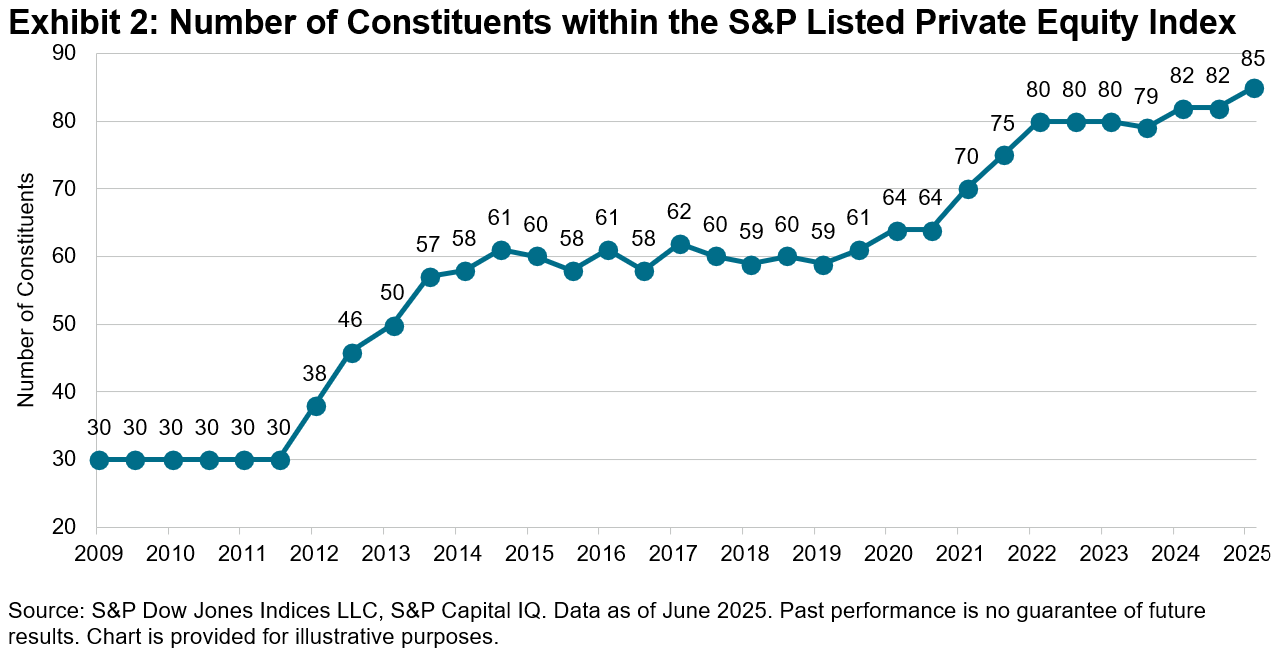

The S&P Listed Private Equity Index tracks leading public companies engaged in private markets activities, namely private credit, venture capital, buyouts and seed investments, given specific market-capitalization and liquidity thresholds and exchange listing requirements. The index membership has grown from 30 constituents in 2009 to 85 as of 2025, reflecting the rising number of private capital firms undergoing IPOs (see Exhibit 2).

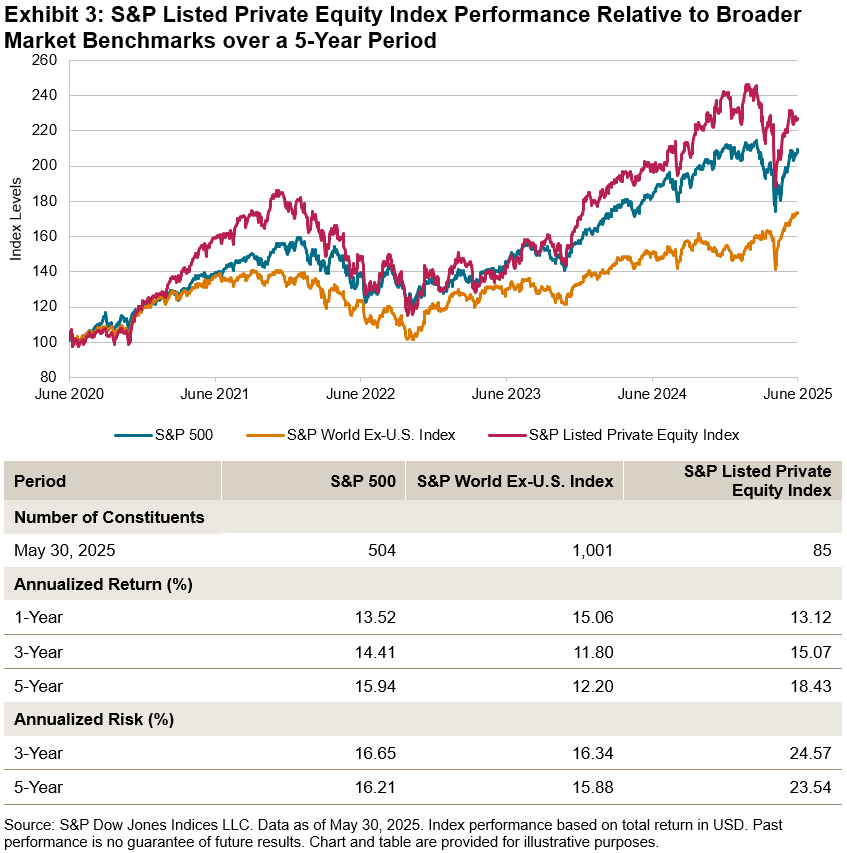

The S&P Listed Private Equity Index has outperformed both the S&P 500 and the S&P World Ex-U.S. Index over the past five years, albeit with increased volatility; potentially driven by favorable market perception, fueling rising demand for access to the asset class (see Exhibit 3). Diversification characteristics and access to high-growth companies that are staying private for longer represent some of the key drivers explaining the growing interest in private markets.

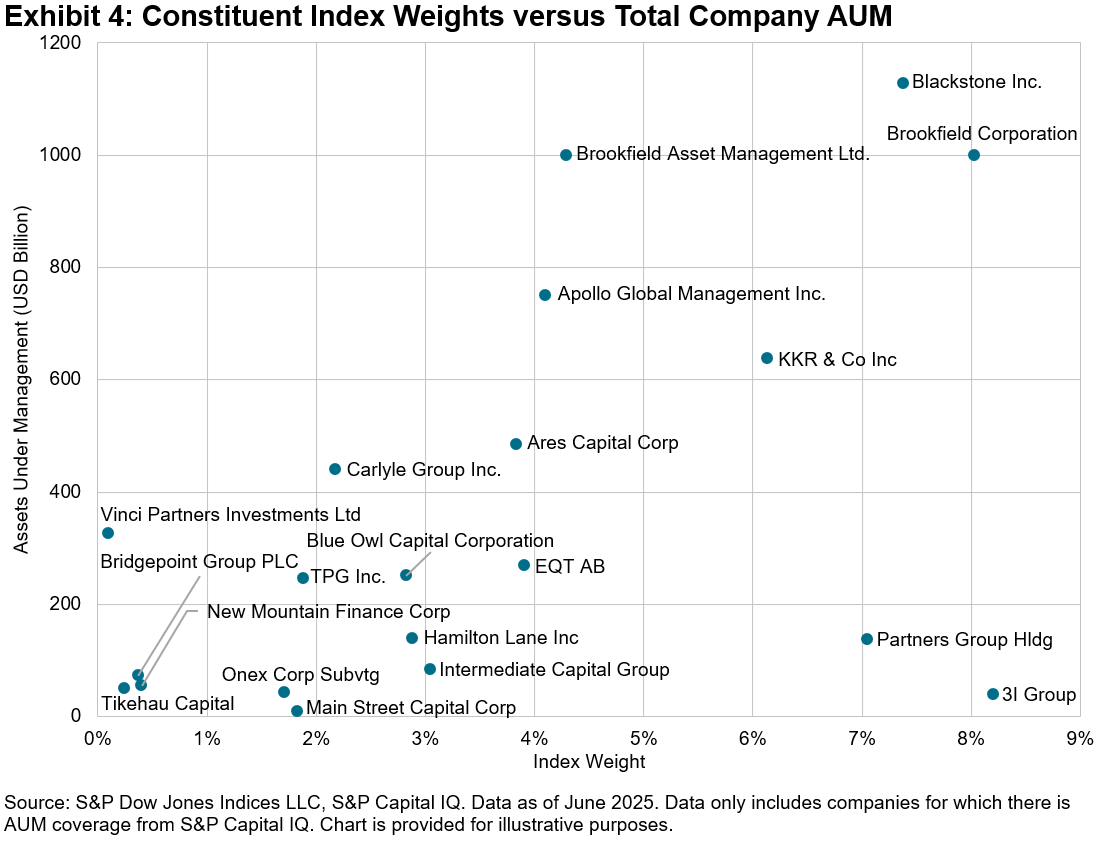

On a constituent level, it may not come as a surprise that the main listed PE firms by AUM represent some of the largest index weights, with Blackstone, KKR and Brookfield standing out within the top five constituents by index weight (see Exhibit 4).

As demand for alternative assets continues to grow, listed private equity may offer a bridge to indirect participation in private markets. The S&P Listed Private Equity Index may serve as a tool to track this dynamic segment, while offering a framework to assess the long-term potential of private markets with the liquidity of public equities.

The posts on this blog are opinions, not advice. Please read our Disclaimers.