U.S. large-cap growth has been outperforming this quarter, thanks in part to unusually strong contributions from a few single-stock winners. With higher dispersion among performance, market participants might conclude that it’s a good time to pick stocks or appoint a fund manager to do it for them. However, while the rewards for picking winners may be greater, it may not be any easier than usual to sort the wheat from the chaff.

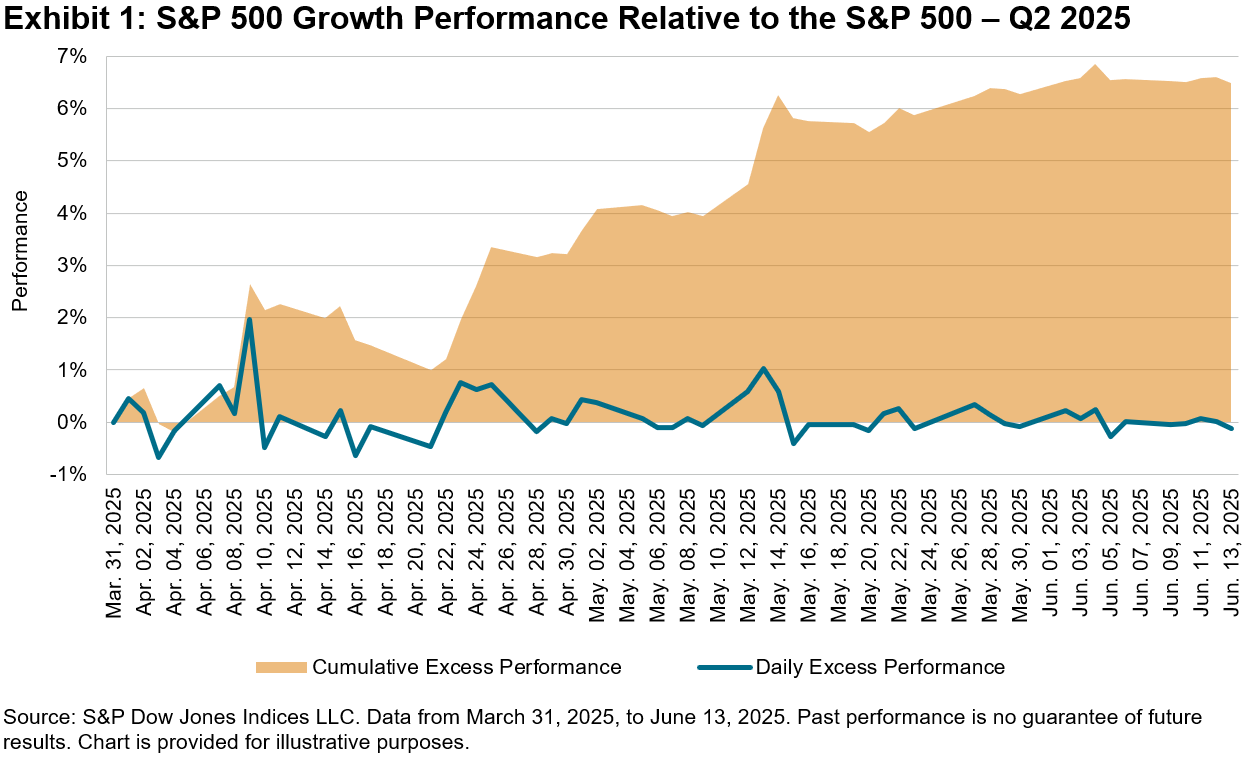

Exhibit 1 shows the daily and cumulative relative QTD performance of the S&P 500® Growth as compared to the S&P 500. Much of the outperformance was concentrated in April and mid-May, but it has steadily outperformed over the period, for a cumulative 6.3% excess return.

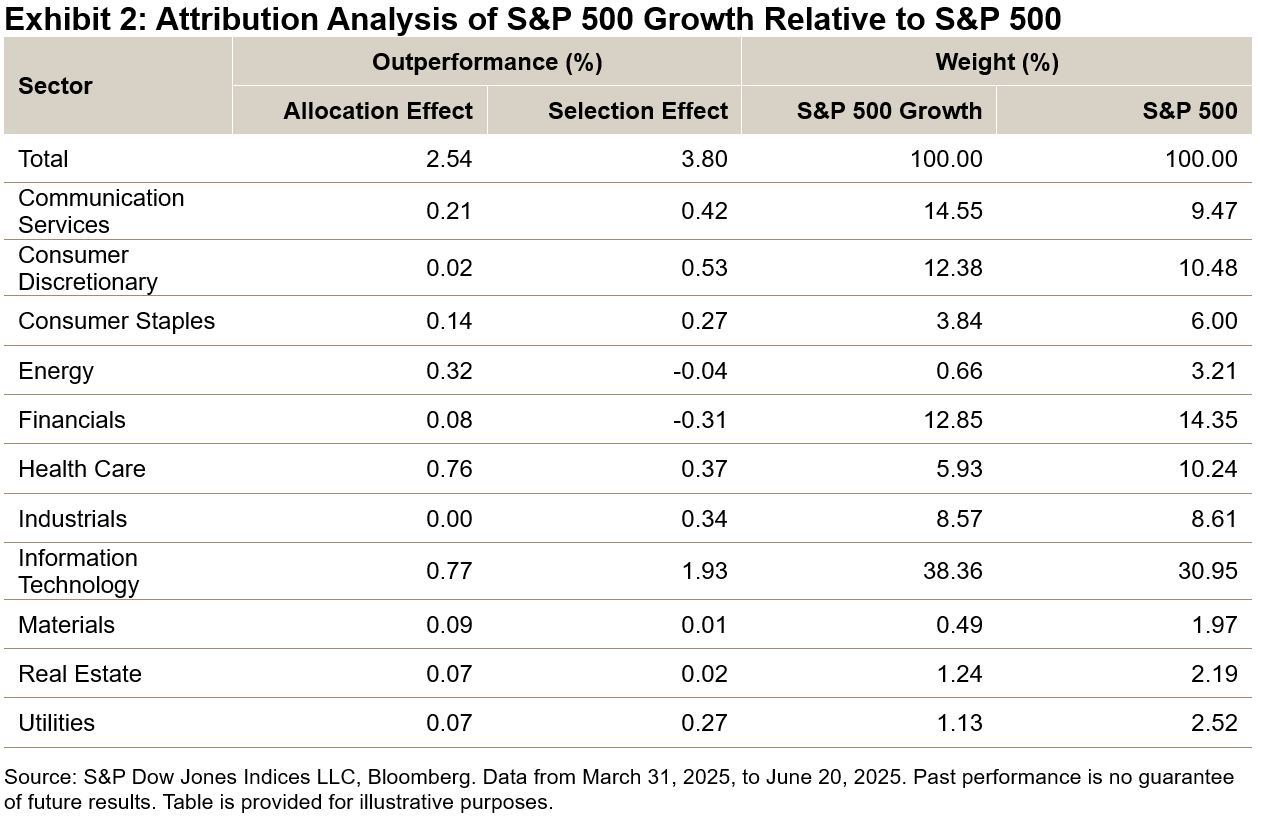

While sectors traditionally associated with growth—such as Information Technology—also performed well during the period, Exhibit 2 shows that single-stock selections, rather than sectoral effects, made the greater contribution to growth’s outperformance. Overall, single-stock effects accounted for 3.8%, while sector effects totaled the remaining 2.5%.

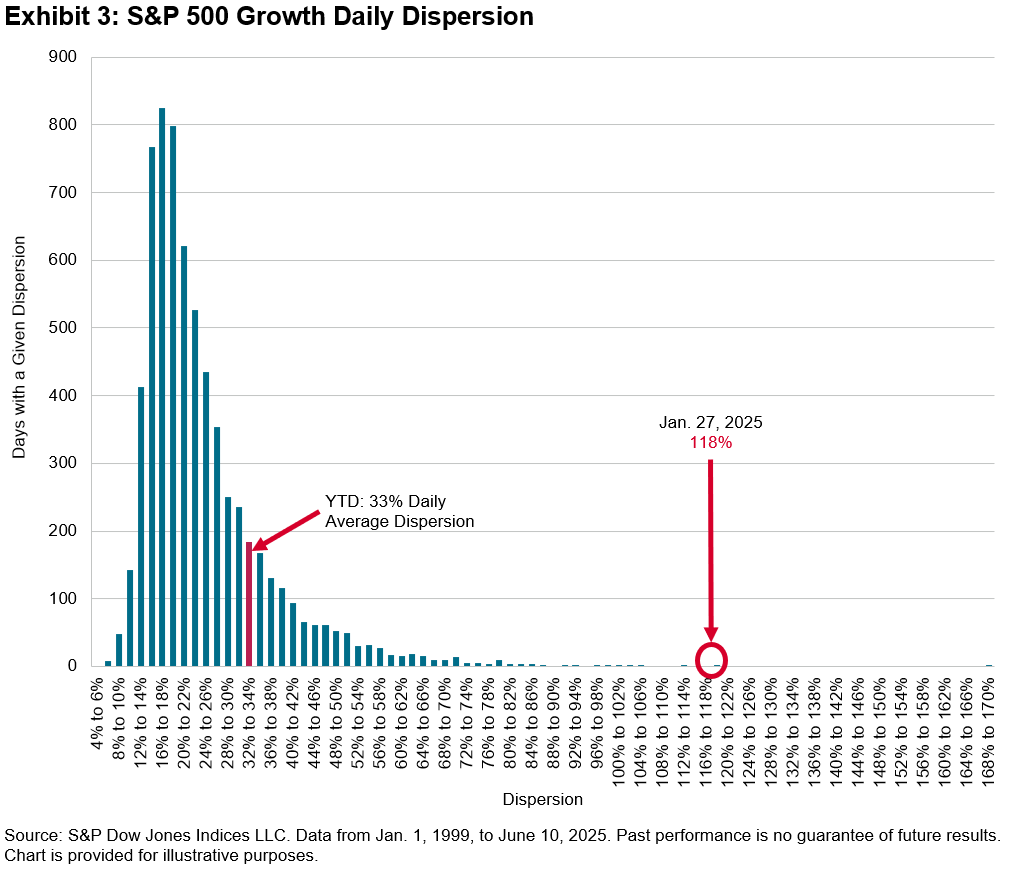

On a related note, overall performance dispersion in growth names has been higher than usual. Exhibit 3 shows the average daily dispersion in the S&P 500 Growth YTD, as compared to the daily index dispersion since 1999. So far in 2025, annualized daily dispersion averaged 33%, far above the median and higher than 83% of historical days.

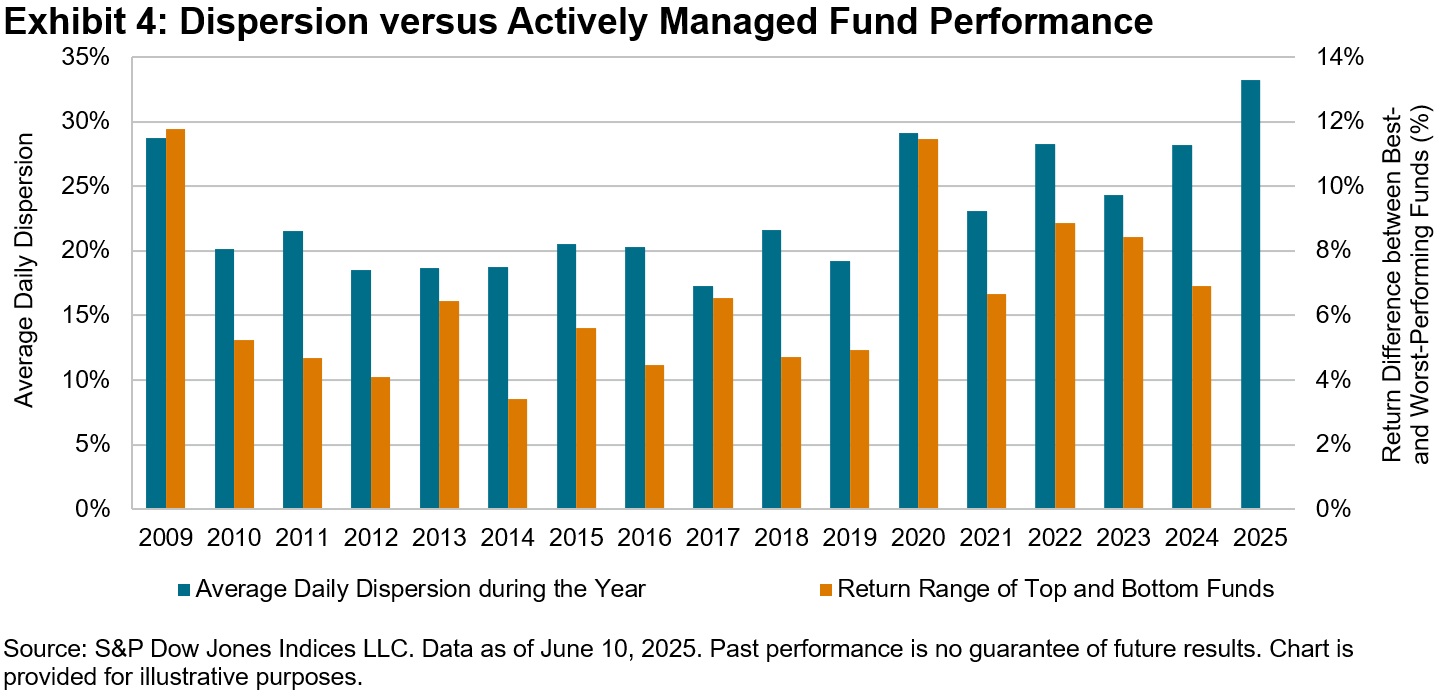

What does higher-than-average dispersion mean for stock pickers? A common assumption is that higher-dispersion environments favor active management, offering a higher degree of potential upside through astute stock selection. Examining the SPIVA® U.S. Year-End Scorecard results from 2003 to 2024 for the Large-Cap Growth fund category, we find that the range of manager outcomes has often risen and fallen in tandem with the prevalent levels of stock dispersion in the S&P 500 Growth. Specifically, Exhibit 4 compares the annual interquartile range among actively managed Large-Cap Growth funds to the average daily dispersion levels for the S&P 500 Growth by calendar year. During years characterized by unusually high dispersion, active funds often exhibited greater variability among their performances.

However, did this equate to higher rates of success among active funds? Opportunities may have been more common, but so was the risk associated with making the wrong selections. Again, SPIVA Scorecards bring this question into focus; wider dispersion did not increase the active manager outperformance rate. In fact, in the U.S. Large-Cap Growth active fund category, the average fund underperformance rate was 63% in the years of above-median dispersion and 55% in the years of below-median dispersion.

As the adage goes, “measuring twice” may prevent a costly mistake. Higher dispersion in growth may continue, along with some positive performance. Participating in winners could mean big rewards, but a hasty decision might be unwise, as shown by the historical SPIVA Scorecard results, 20 years of which are available here to assist market participants with their final cuts.

The posts on this blog are opinions, not advice. Please read our Disclaimers.