How are multi-asset indices with built-in adaptability and risk mitigation helping market participants? Meet the S&P Global Diversified 7.5% Index, a multi-asset index designed for today’s markets, reflecting diversification across regions and asset classes and incorporating dynamic signals to help mitigate market uncertainty.

The posts on this blog are opinions, not advice. Please read our Disclaimers.A Diversified Strategy for the 21st Century

Customizing Bitcoin Exposure to Mitigate Risk Systematically

Introducing the S&P 500 Market Leaders Index

Introducing the S&P 500 Realized Dispersion Indices

Defining Outcomes Systematically with Indices

A Diversified Strategy for the 21st Century

Customizing Bitcoin Exposure to Mitigate Risk Systematically

Bitcoin and lower volatility may seem like opposites, but could it be time to rethink that perspective? S&P DJI’s Michael Mell and Cyber Hornet ETFs’ Mike Willis look inside a blended custom index with 75% weighted to the S&P 500 and 25% weighted to Bitcoin futures as a unique approach to risk management.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

Introducing the S&P 500 Market Leaders Index

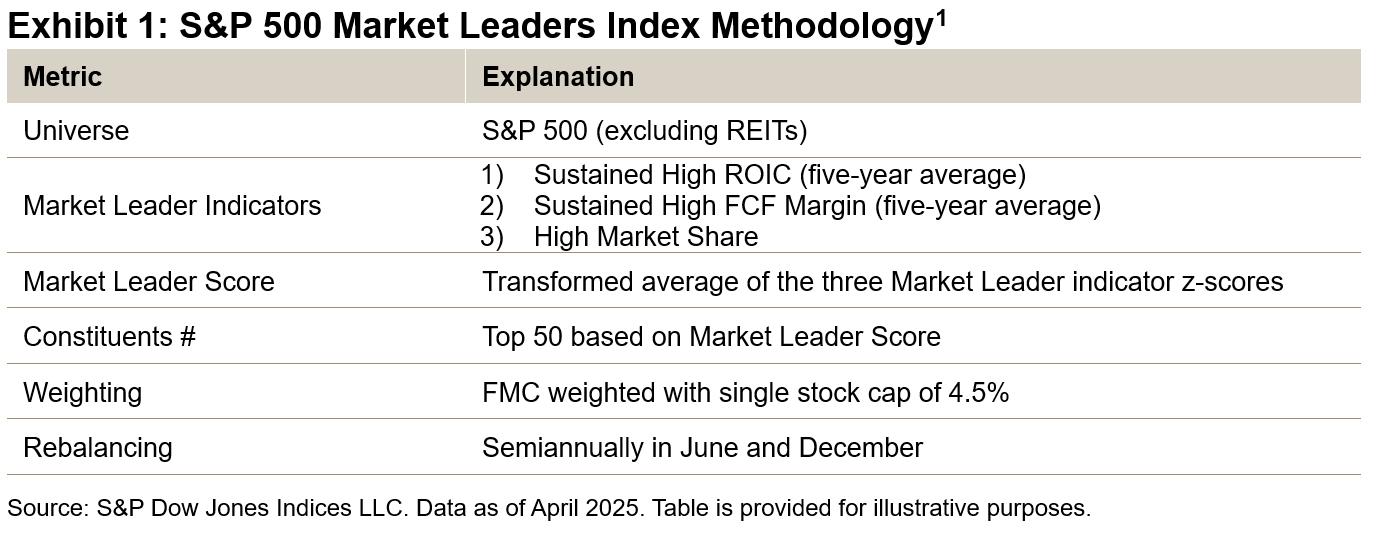

The S&P 500® Market Leaders Index is designed to track companies within the S&P 500 that hold significant market share and sustainable competitive advantages. Unlike the broader S&P 500, this index zeroes in on companies that consistently outperform their peers in terms of return on invested capital (ROIC), free cash flow (FCF) generation and substantial market presence. In this blog, we will delve into how this index is constructed, examine its back-tested performance and highlight its unique characteristics.

Methodology Overview

The S&P 500 Market Leaders Index selects companies using a Market Leader Score based on the average of three key metrics.

- High Market Share: This metric may indicate competitive advantages like economies of scale, network effects or strong brand power. Companies with high market share often have better pricing power and higher returns.

- Sustained High ROIC: Calculated as the five-year average of net income divided by total equity plus total debt, this metric assesses profitability and reflects a company’s efficiency in capital utilization. Market leaders often exhibit stronger ROIC due to their dominant market positions.

- Consistent High FCF Margin: Companies that maintain consistently high FCF margins over five years, combined with high ROIC, tend to be able to effectively redeploy cash flow, helping them maintain market share.

The top 50 companies ranked by Market Leader Score are included in the index and are weighted by float-adjusted market capitalization (FMC).

Historical Performance Characteristics

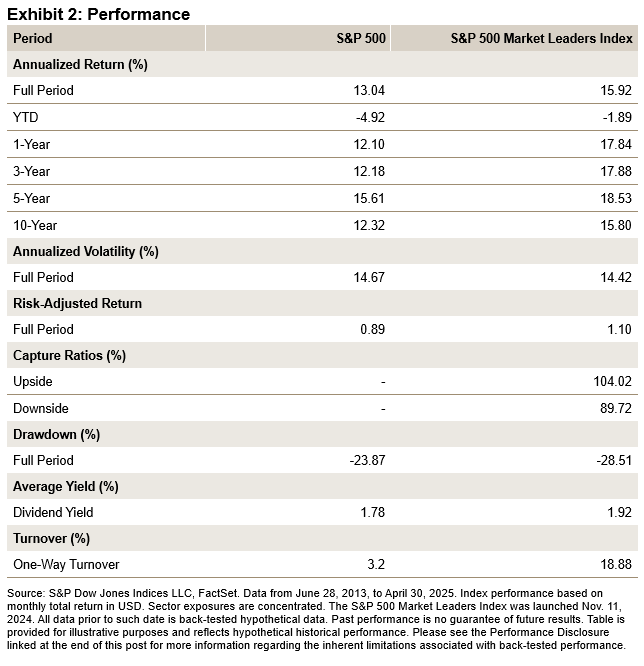

The S&P 500 Market Leaders Index has demonstrated impressive long-term performance compared to the benchmark. As shown in the back-tested period covered in Exhibit 2, it has outperformed with lower volatility, leading to better risk-adjusted returns. The index not only offered greater upside potential but also a defensive stance. Notably, during the recent tariff-related drawdowns, the S&P 500 Market Leaders Index outperformed the benchmark by 2.23%

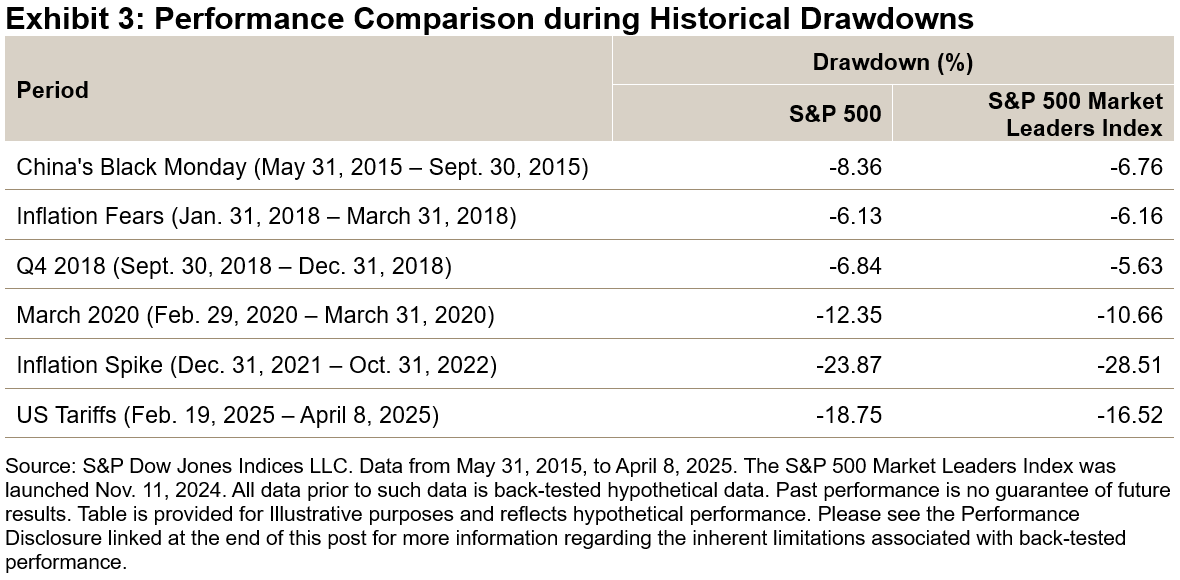

Historical Drawdowns

The S&P 500 Market Leaders Index has often benefited from downside protection during past market sell-offs.

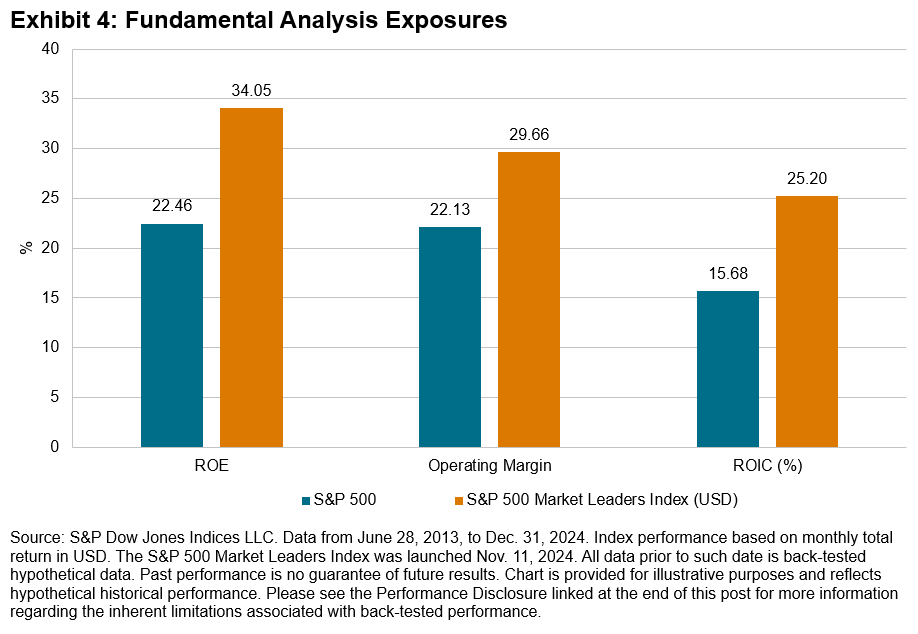

Higher Quality Constituents

Historical fundamental analysis of the index reveals a greater focus on profitability metrics that align closely with the quality factor.

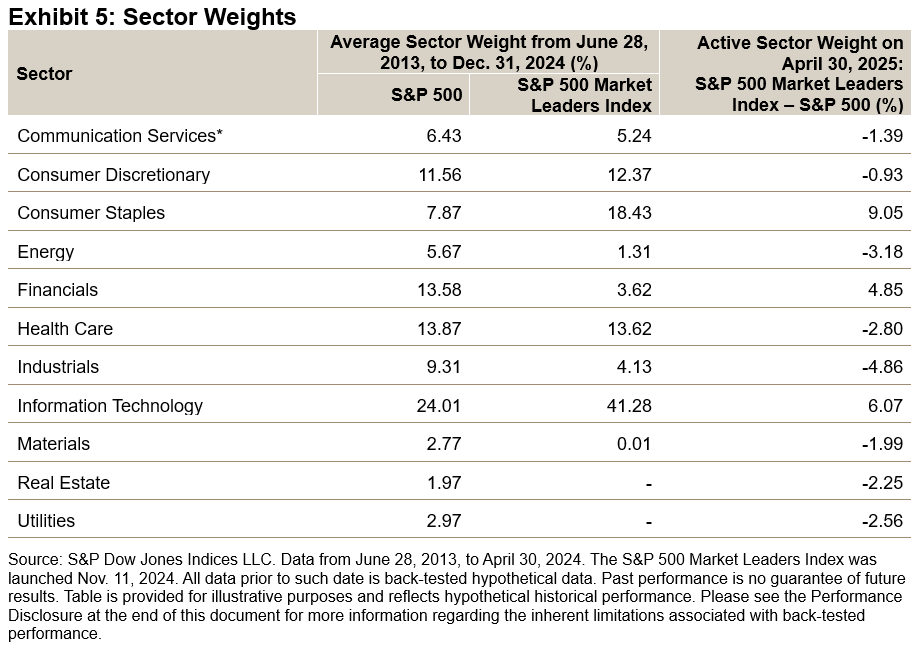

Sector weights have been diversified and historically skewed toward Consumer Staples, Health Care and Information Technology compared to the benchmark, with underweights in Energy and Industrials. As of Dec. 31, 2024, the index showed overweights in Consumer Staples, Financials and Information Technology, while Health Care was underweight.

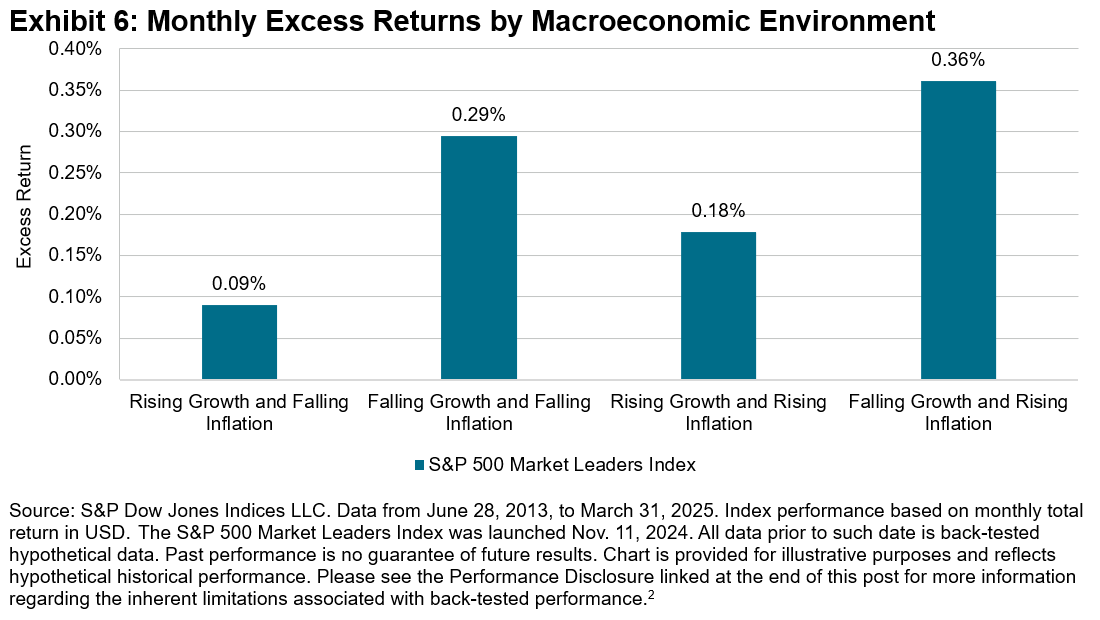

Historical Macroeconomic Performance

The S&P 500 Market Leaders Index tended to outperform the benchmark in most market environments but had the highest performance in periods of falling growth, regardless of inflation.

Conclusion

The S&P 500 Market Leaders Index tracks 50 of the most consistently high-performing companies in the U.S. equity market. By focusing on ROIC, FCF margin and market share, the index seeks to identify market leaders with sustainable competitive advantages. Historically, this approach has identified higher-quality companies that exhibited defensive qualities and strong risk-adjusted performance.

1 For more information please see the full methodology.

2 Further explanation of the macroeconomic analysis is available in the blog A Historical Perspective on Factor Index Performance across Macroeconomic Cycles.

The posts on this blog are opinions, not advice. Please read our Disclaimers.Introducing the S&P 500 Realized Dispersion Indices

Market participants are continuously seeking innovative tools to better understand market dynamics and manage risk. This week marks the launch of the S&P 500® Realized Dispersion Indices. These indices are designed to measure the historical dispersion of The 500™ over various time periods, providing valuable insights into market volatility and the performance of individual stocks relative to the broader market. They also serve as an analytical complement to the Cboe S&P 500 Dispersion Index (DSPX), which measures implied dispersion over the next 30 days.

Understanding Dispersion and Its Importance

Dispersion is an important statistical measure that quantifies the range of outcomes among the components of an index during a specific period. By evaluating how individual stocks perform in relation to the overall index, it’s possible to gain insights into individual patterns and underlying risks.

The S&P 500 Realized Dispersion Indices offer two primary measures: the S&P 500 1-Day Realized Dispersion Index, which reflects historical dispersion over a single trading day; and the S&P 500 30-Day Realized Dispersion Index, which provides insights over a rolling 30-calendar day period. The full universe is used for the S&P 500 1-Day Realized Dispersion Index, while the 30-day version is limited to stocks that remain in the index for the entire rolling period and maintain non-zero weights; corporate actions like spin-offs are excluded to avoid distortions. These indices utilize daily and monthly returns, as well as adjusted close weights of each S&P 500 constituent, alongside the daily and monthly returns of The 500 itself. This comprehensive approach makes it possible for market participants to gain a nuanced understanding of market behavior and the performance of individual stocks.

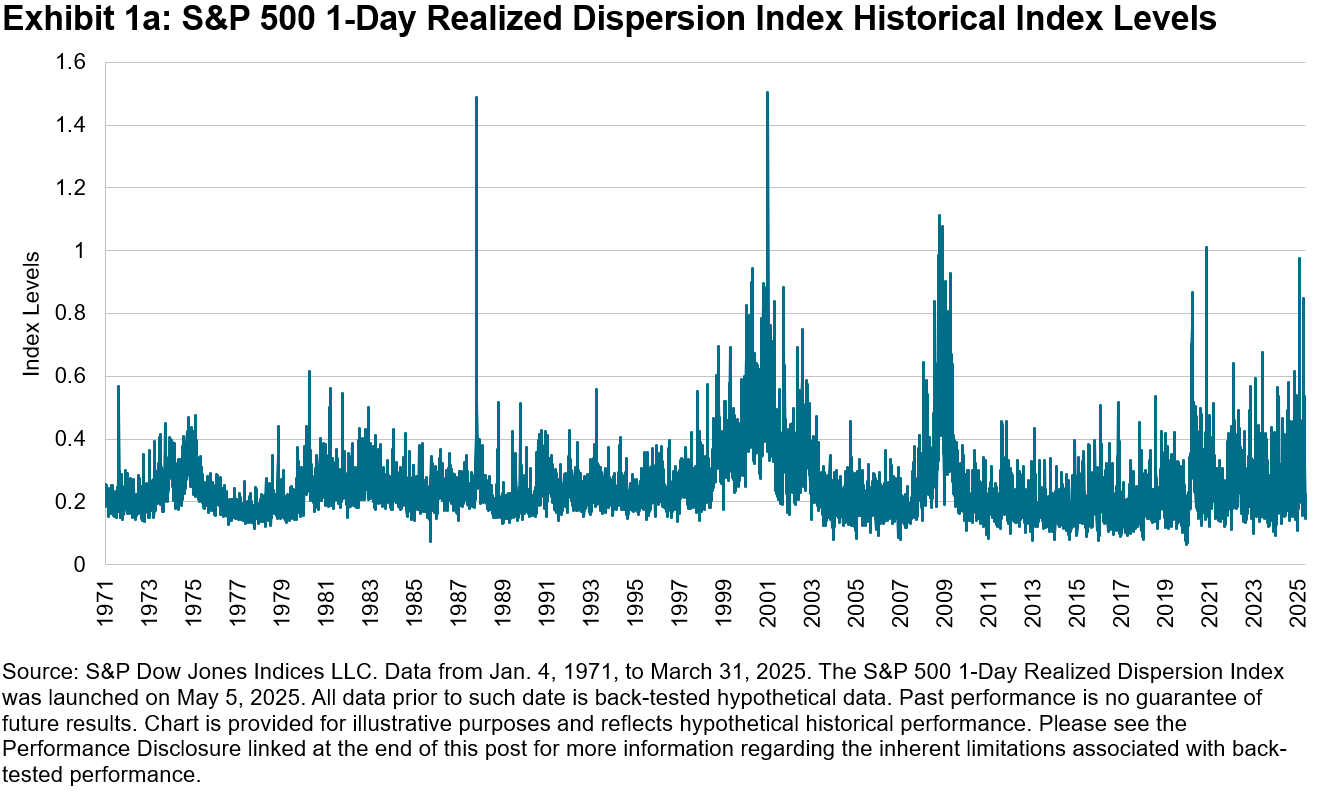

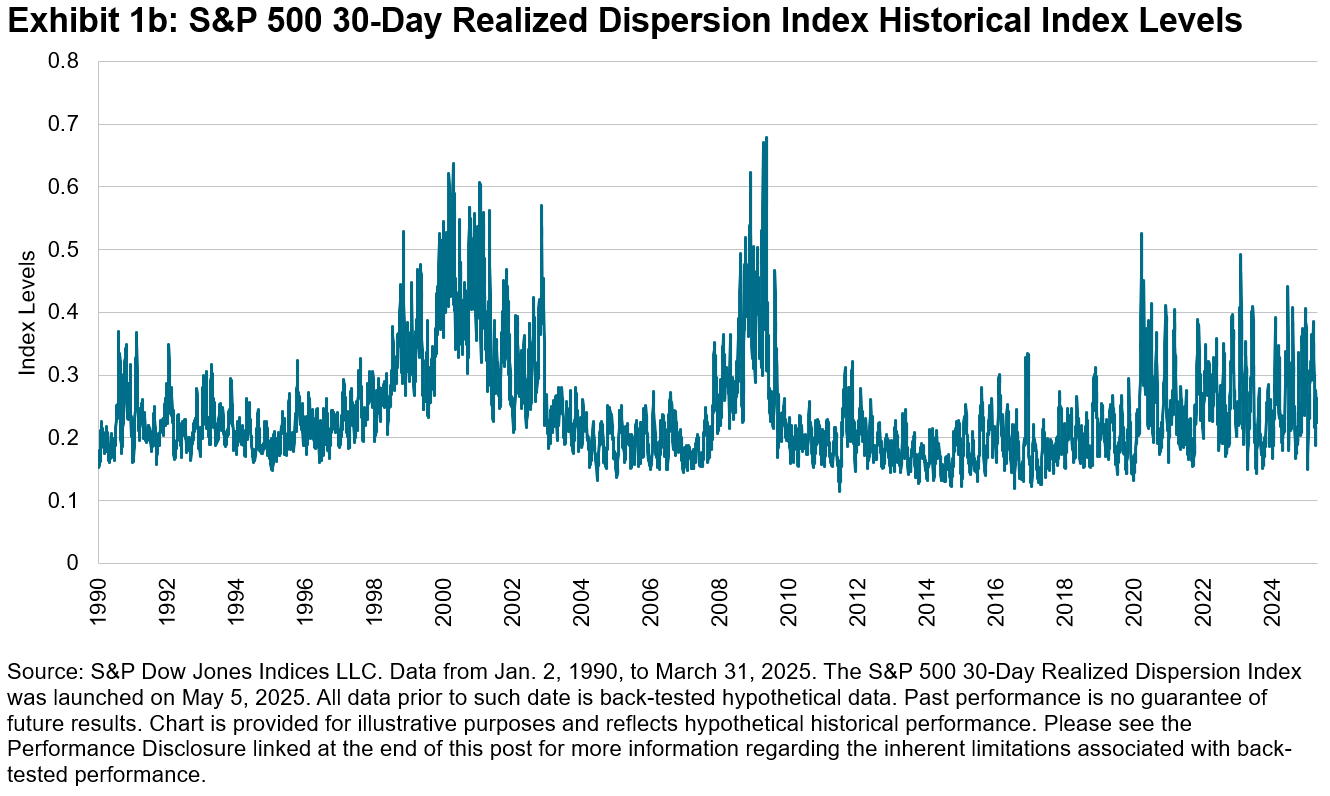

Exhibits 1a & 1b show the historical hypothetical levels of the index over the period for which data is available. The spikes highlight volatile market conditions where individual stocks experienced varying degrees of price movements, which often resulted in greater differences in performance. This divergence in stock returns relative to one another typically manifested as increased dispersion, making patterns and underlying risks across the market easier to observe.

It’s useful to highlight the difference between macro volatility and dispersion, particularly through the lens of historical market events. Dispersion reflects how differently individual stocks move from one another, while volatility captures the overall intensity of market movement. Correlation measures the degree to which two securities move in relation to each other. During the Black Monday crash of 1987 and the Dot-Com burst of March 2000, dispersion reached an all-time high as stock performance diverged significantly—some soared while some crashed, driven by lower correlations. In contrast, events like the Global Financial Crisis of 2008 and COVID in 2020 were marked by high volatility and high correlations, where most stocks moved in the same direction. Recognizing these patterns could provide insights into the fundamental drivers of equity market risk and return.

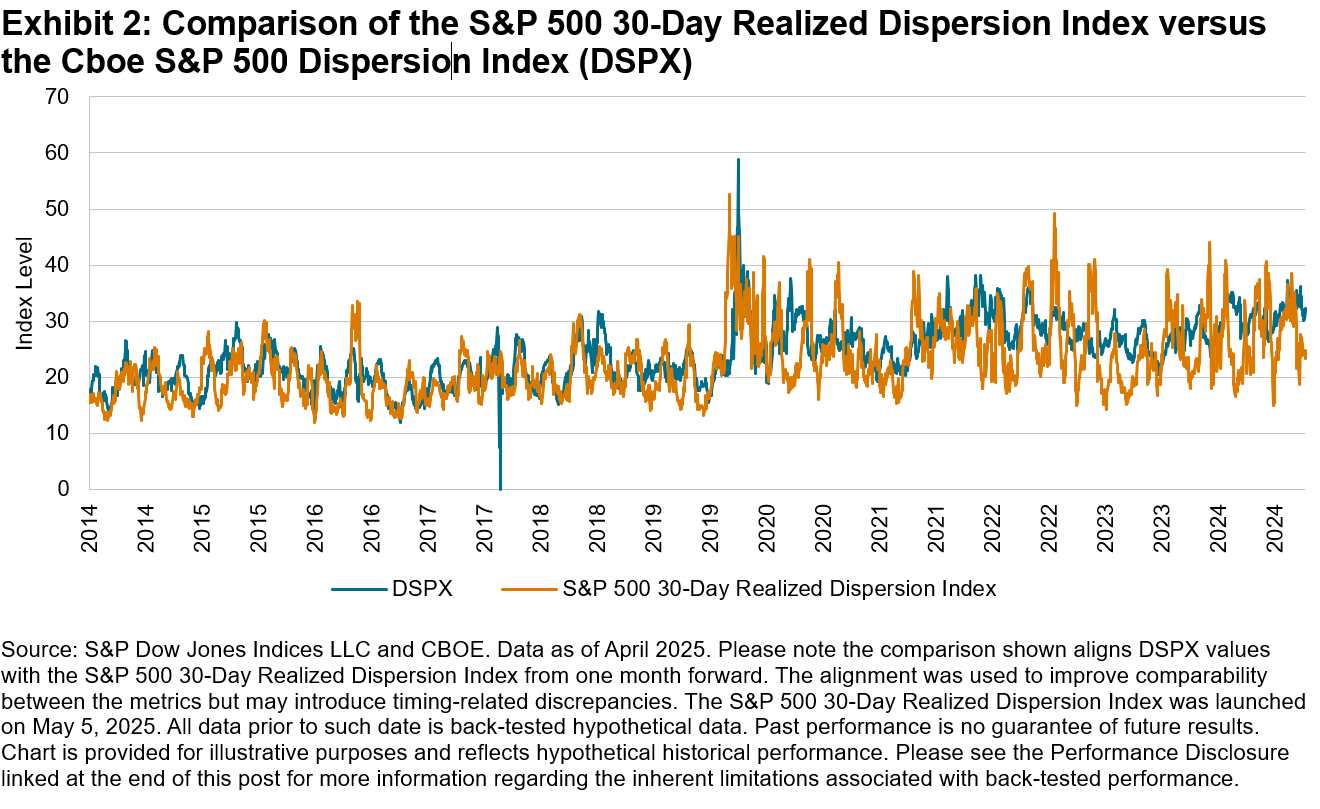

Exhibit 2 compares the S&P 500 30-Day Realized Dispersion Index with the DSPX, highlighting the relationship between historical and implied dispersion over time. Realized dispersion reflects the variability of individual stock returns over the past 30 days, while DSPX reflects the market’s expectation for dispersion over the next 30 days. The two series generally moved together but there were notable gaps during periods of heightened uncertainty. These divergences can offer insights into shifts in market sentiment and can help identify when the market overestimated or underestimated future stock return differences.

Conclusion: A Practical Addition to the Investment Analytics Toolkit

The launch of the S&P 500 Realized Dispersion Indices marks a notable development in the tools available to investors seeking to navigate market volatility. By providing a transparent measure of realized dispersion, these indices may help investors better understand the underlying dynamics of risk and return in the U.S. equity market.

For more information on the S&P 500 Realized Dispersion Index Methodology, please refer to the S&P U.S. Indices Methodology, available at www.spglobal.com/spdji.

The posts on this blog are opinions, not advice. Please read our Disclaimers.Defining Outcomes Systematically with Indices

How are index innovations helping market participants address volatility and uncertainty? S&P DJI’s Anu Ganti and Calamos Investments’ Matt Kaufman discuss index-based approaches to defined outcomes.

The posts on this blog are opinions, not advice. Please read our Disclaimers.