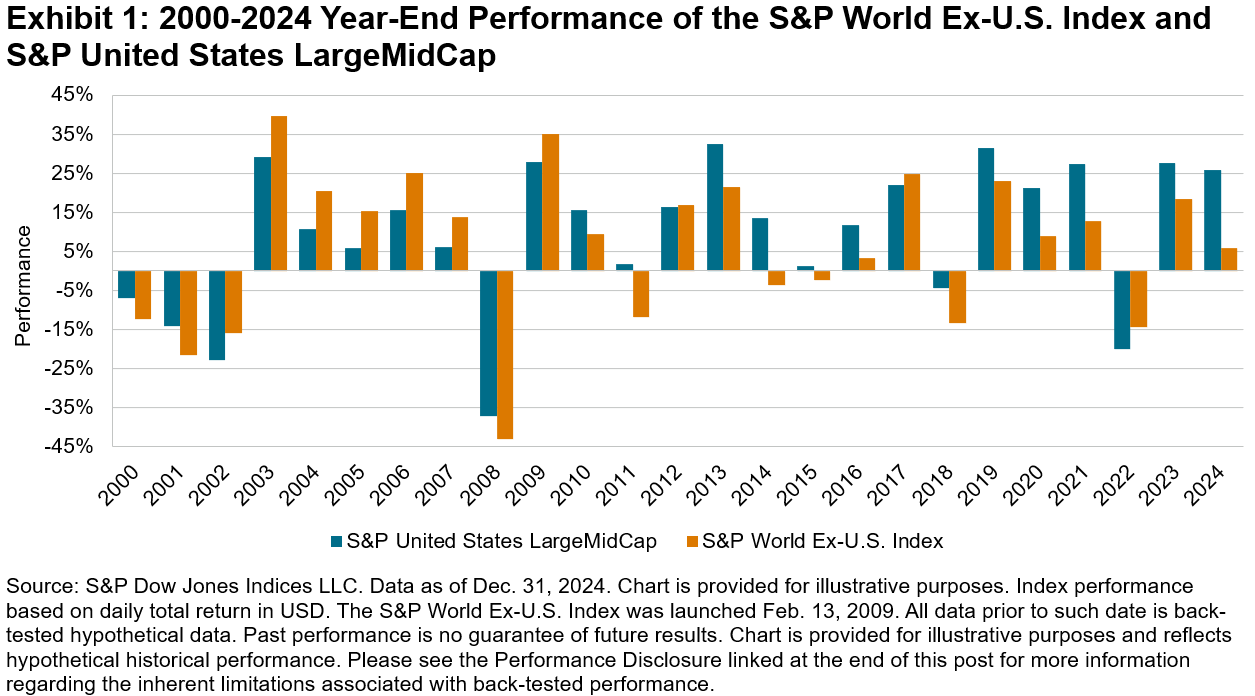

Since 2000, annual returns of international equities have been better than those of the U.S. only nine times, as shown by Exhibit 1. After the Global Financial Crisis of 2009, the S&P United States LargeMidCap outperformed the S&P World-Ex-U.S. Index in most years.

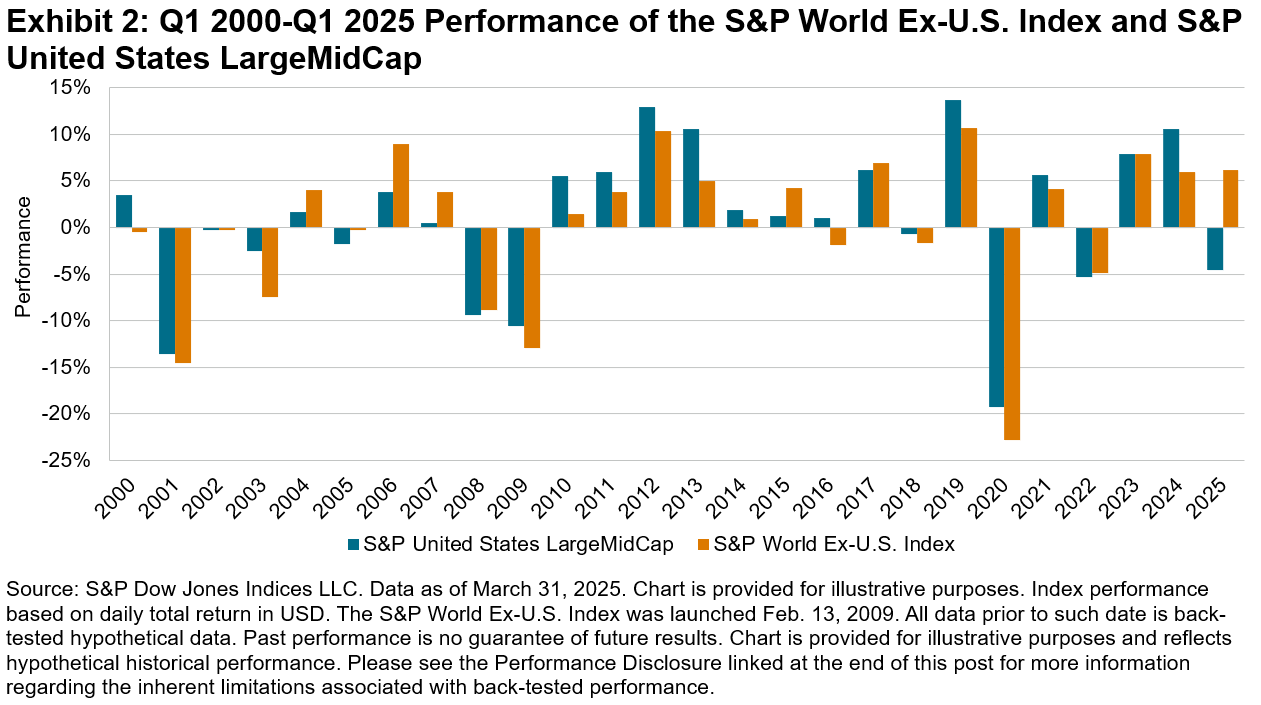

However, for the first time since 2017, developed market equities have ended the first quarter outperforming the U.S. As concerns grow about the impact of tariffs on the economy and uncertainty looms, market participants appear to be reducing their weight in the U.S. In fact, as illustrated by Exhibit 2, the S&P World Ex-U.S. Index had one of its best first quarters in recent times, while the S&P United States LargeMidCap started in the red. A strong start to the year is not always a definitive predictor of year-end performance, but what might this data suggest about the S&P World Ex-U.S. Index’s current outperformance?

The first quarter of the year was marked by uncertainty caused by geopolitical and economic developments. Tariff threats from the new U.S. administration, talks to end the war in Ukraine, shifting diplomatic relations, political changes in Germany and Canada, and reignited tensions in the Middle East were all part of a challenging beginning of the year. On the monetary front, central banks across the globe may diverge in their decisions around interest rates, but they are expected to proceed with caution due to inflation and recession concerns.

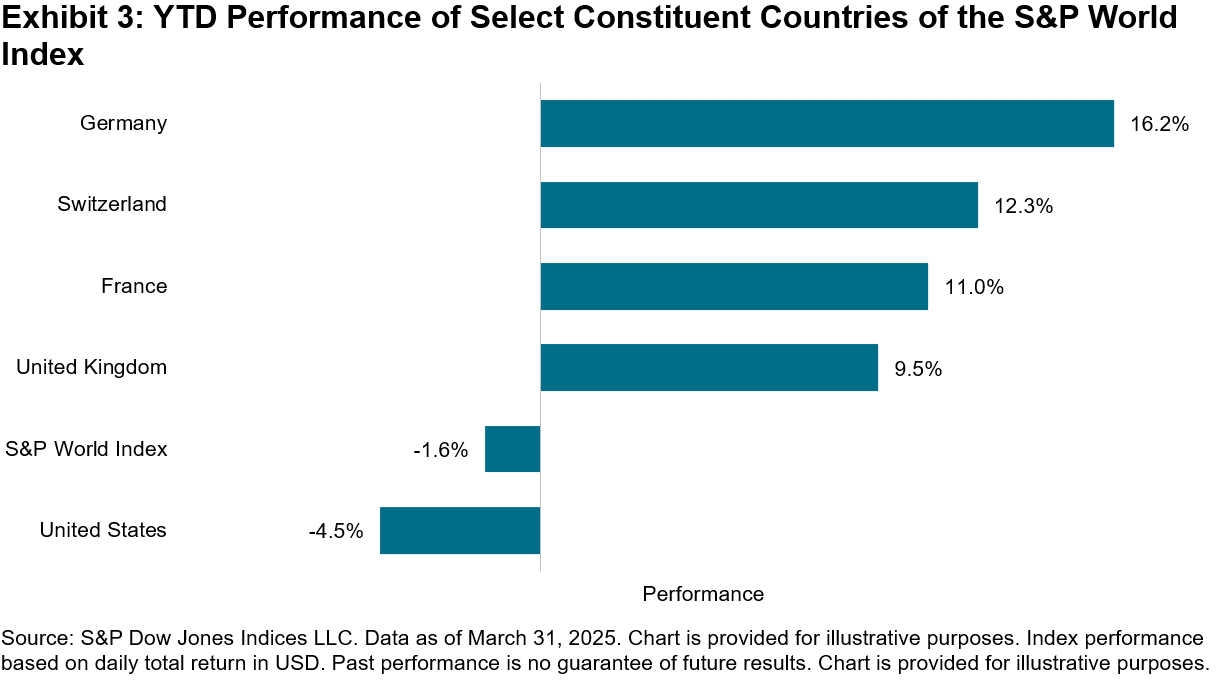

As of end of March, almost all European countries that constitute the S&P World Index started on a positive note. Germany, the U.K., France and Switzerland have been the main contributors to the outperformance of the S&P World Ex-U.S. Index. In contrast, the S&P United States LargeMidCap was among the worst performers in developed markets, decreasing 4.5%.

Among the GICS® sectors in the S&P World Ex-U.S. Index, which mostly had positive performance, there is one that stands out: Financials. The S&P World Ex-U.S. Financials (Sector) Index rose 12.2% in Q1 2025. This sector has been the main driver behind the outperformance of the S&P World Ex-U.S. Index, contributing to almost half of its increase (46%). This growth may possibly be attributed to positive economic surprises, resilience in European bank earnings and the effects on the economy of a potential end to the war in Ukraine.

Additionally, the Industrials sector, which gained 6.1%, has been an important contributor to the performance of the S&P World Ex-U.S. Index, as defense spending is expected to increase. Utilities and Energy were also among the best-performing sectors of the first quarter, as the European Commission launched a plan that aims to increase investments that contribute to energy security in the region.

Amid geopolitical tensions and evolving trade policies, international equities from developed markets in 2025 have outperformed the U.S. YTD, as some market participants are turning their focus to other geographies. Given the recent economic landscape in the U.S. and around the world, the S&P World Ex-U.S. Index is a relevant benchmark for the current market environment.

The posts on this blog are opinions, not advice. Please read our Disclaimers.