Climate resilience refers to the ability of a system to anticipate, prepare for and respond to the impacts of climate change.1 As the world grapples with the adverse effects of a changing climate, climate resilience stands front and center in collective efforts from governments, corporations and the investment community2 alike. This blog is the first of a two-part series exploring a forward-looking framework to assess companies’ climate action across different dimensions. Our next blog will examine how this framework can be used to create index strategies in a rules-based, transparent way.

Measuring Companies’ Readiness for the Transition to a Low Carbon Economy

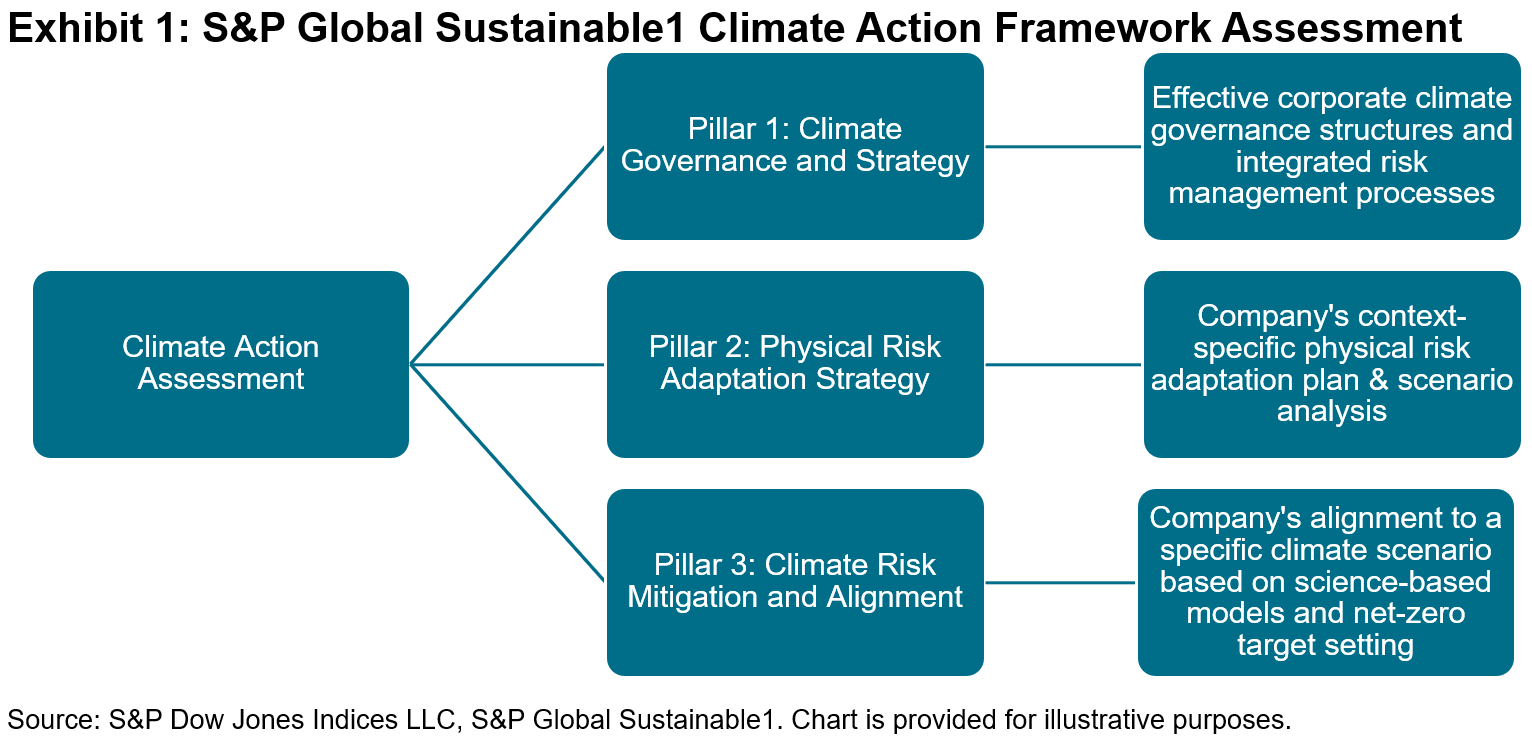

The S&P Global Sustainable1 Climate Action Framework is an innovative dataset that assesses companies’ ability to manage the risks of transitioning to a low-carbon economy through the lens of three key dimensions:

- Climate Governance and Strategy;

- Physical Risk Adaptation Strategy; and

- Climate Risk Mitigation and Alignment.

The assessment leverages raw data collected from S&P Global’s Corporate Sustainability Assessment (CSA), which underpins the S&P Global ESG Scores. Additionally, it integrates established metrics such as implied temperature rise, revenue exposure from business activities and various environmental indicators to provide a comprehensive evaluation of a company’s risk management capabilities, adaptability to physical risks and strategies for mitigating future climate challenges.

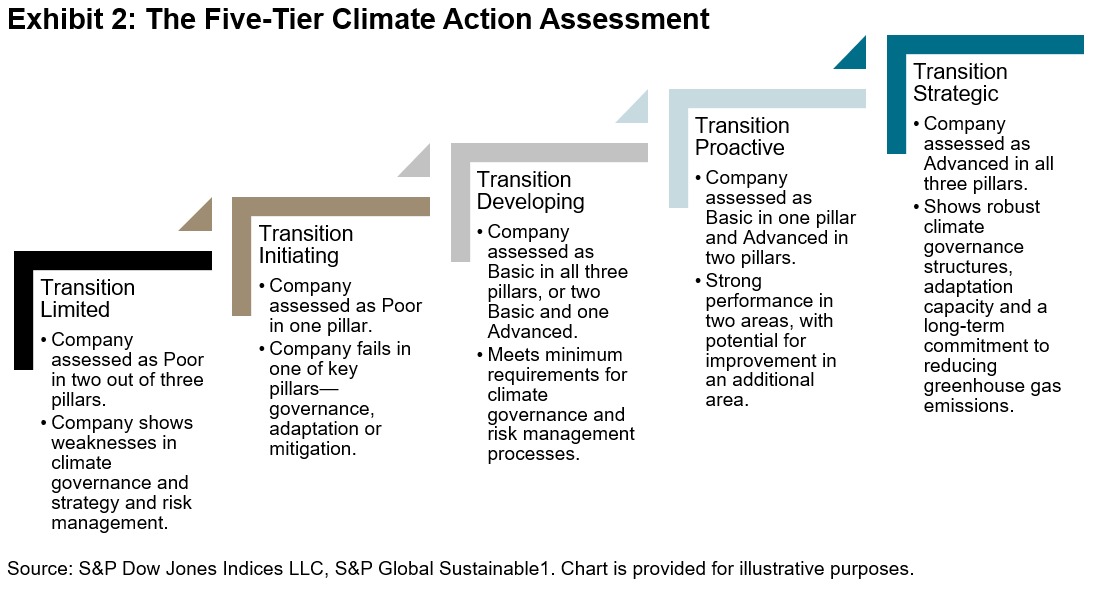

The framework categorizes companies’ performance across each of the three key pillars, as well as on an aggregate-level assessment. Companies can be classified as having “Advanced,” “Basic” or “Poor” performance across the pillars. Combined, these classifications result in a five-tier aggregate assessment (see Exhibit 2) ranging from “Transition Limited,” where companies lack basic governance structures, climate risk management processes and target-setting, to “Transition Strategic,” in which companies demonstrate robust climate strategies, comprehensive risk management plans and a long-term commitment to achieve net zero emissions.

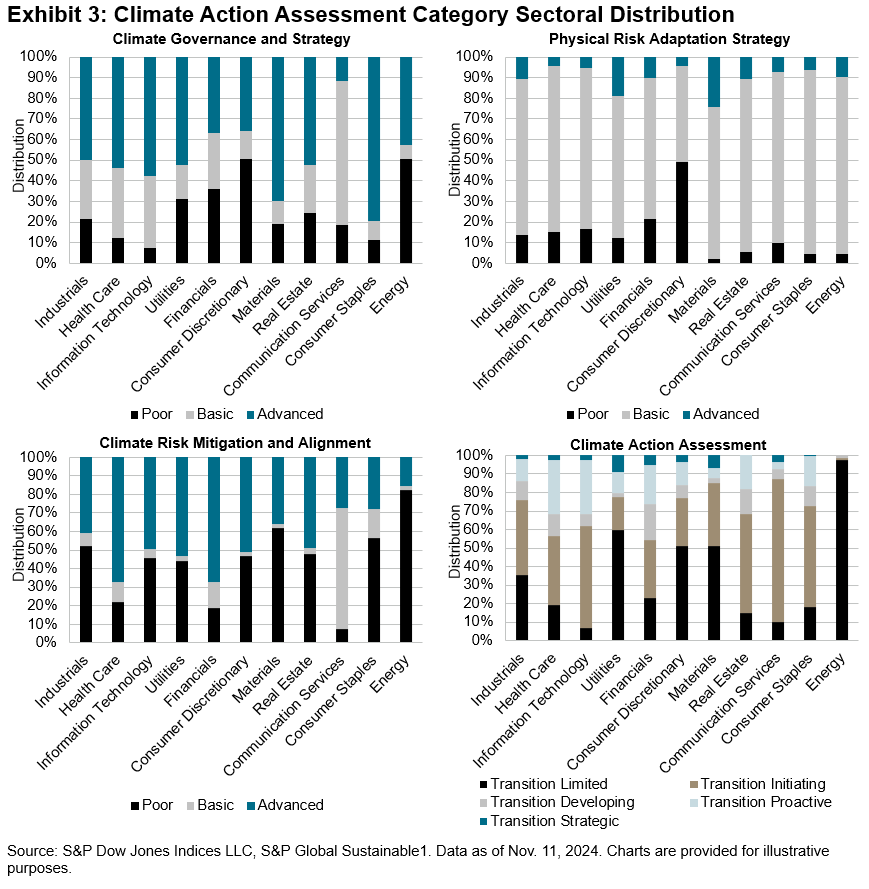

We examined the sectoral breakdown of each of the pillars and the final Climate Action Framework assessment within the S&P World Index (see Exhibit 3). Across sectors, we see a wide distribution of outcomes for each of the categories.

In general, we observe a considerable portion of companies across sectors that were assessed as Poor and Advanced for the Climate Governance and Strategy and Climate Risk Mitigation Pillars. However, most companies have a Basic physical risk adaptation strategy, and very few can be considered Advanced, suggesting that generally, companies lack context-specific adaptation plans. Aggregating the pillars, we see most companies classified at the bottom two tiers as either Transition Limited or Transition Initiating, reflecting the increasing climate action ambition required by the top tiers.

Taking the Energy sector as an example, we see that:

- Roughly 50% of companies lack adequate climate governance practices, classifying them as Poor within Pillar 1;

- The vast majority have sufficient overall physical risk adaptation plans and conducted scenario analysis, classifying them as Basic within Pillar 2; and

- Approximately 80% of companies are classified as Poor within Pillar 3, most likely due to their higher implied temperature alignment and the lack of net zero targets covering Scope 3 emissions.

On an aggregate level, we observe that 97% of energy companies are ranked as Transition Limited, suggesting that there is still much room for improvement on the climate front for most companies in the sector.

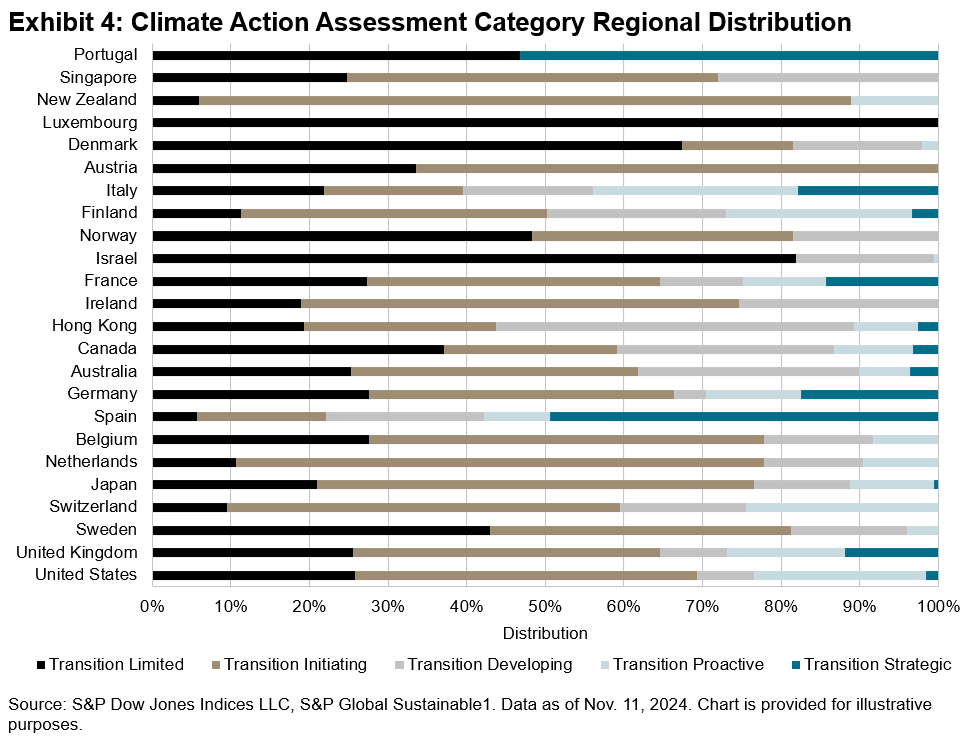

From a regional perspective, we observe a similar pattern in which there is a varied distribution of categories across regions (see Exhibit 4). Exploring the U.S., which comprises around 70% of the S&P World Index by market capitalization, we see most companies classified as either Transition Limited or Transition Initiating (i.e., the bottom two categories), and only 2% achieved the highest rank of Transition Strategic.

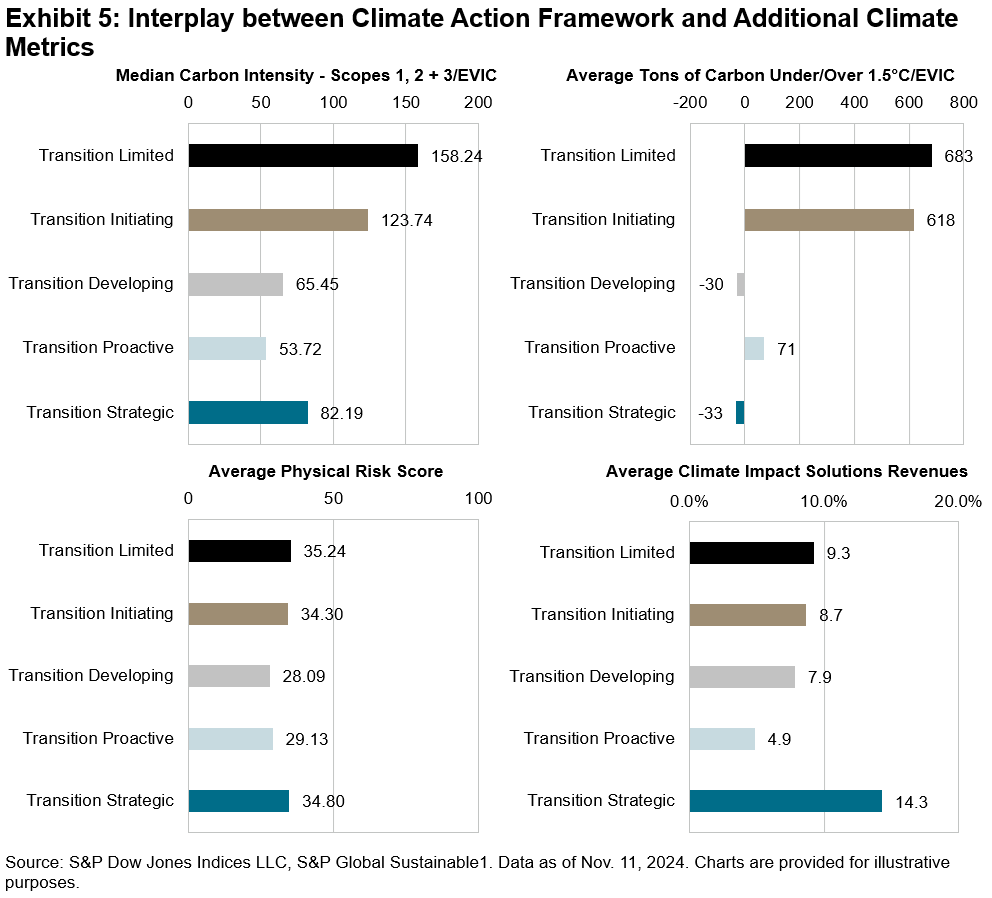

Analyzing the interplay between the Climate Action Framework assessment and other climate data points reveals interesting insights (see Exhibit 5).

- There was a positive pattern between carbon efficiency and climate action, in which companies with enhanced climate governance and risk management structures also tend to be relatively more carbon efficient.

- There was a relationship between forward-looking temperature rise and climate action practices—we see that Transition Strategic companies were under their 1.5°C carbon budget, indicating forward-looking alignment with the Paris Agreement goals.

- There was not a strong pattern regarding physical risk, suggesting that physical risk may need to be addressed separately in an index that incorporates climate action assessments, to mitigate tail risk.

- It is worth noting that Transition Strategic companies displayed the highest revenue alignment with climate impact solutions, such as renewable energy, sustainable transportation and battery technology.

In the second part of this blog series, we will explore the recently launched S&P World Climate Resilience Tilted Index, which incorporates elements of the S&P Climate Action Framework and additional climate datapoints to tilt toward companies that are relatively more climate resilient and carbon efficient, and that have higher exposure to climate impact solutions.

1 Intergovernmental Panel on Climate Change. “Climate Change 2022: Impacts, Adaptation and Vulnerability.” 2022.

2 Vijayakumar, C. “Collective action is the key to drive urgency in building climate resilience.” World Economic Forum. Jan. 19, 2025.

The posts on this blog are opinions, not advice. Please read our Disclaimers.