The author would like to thank Arlene Habib for her contributions to this blog.

Diversification is a foundational principle within asset allocation, as it seeks to reduce risk and mitigate drawdowns by combining exposure across different asset classes—like equities, fixed income and commodities—that generally do not move in tandem. Commodities, like energy and precious metals, tend to exhibit low correlations to equities and fixed income. Therefore, they have long played a part in asset allocation for their potential diversification and inflation protection benefits.

The recently launched S&P Commodity Risk Premia Diversifier TCA Index offers diversified commodity exposure via four underlying alternative risk premia indices, based on the S&P GSCI. Commodity alternative risk premia strategies refer to isolating exposure to specific risk sources, typically categorized by style, such as carry and momentum.

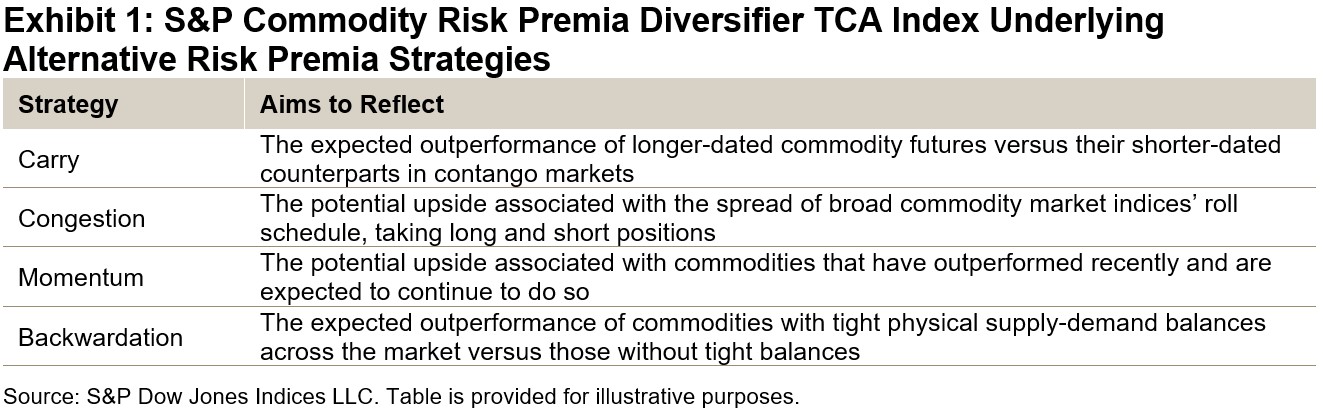

The S&P Commodity Risk Premia Diversifier TCA Index targets an annualized volatility of 5% by combining commodity elements with cash and adjusts its weight to its underlying individual alternative risk premia indices (see Exhibit 1).

The index aims for a risk contribution of 50%-25%-25% based on realized volatility across the underlying strategies of carry-congestion, momentum and backwardation, respectively.

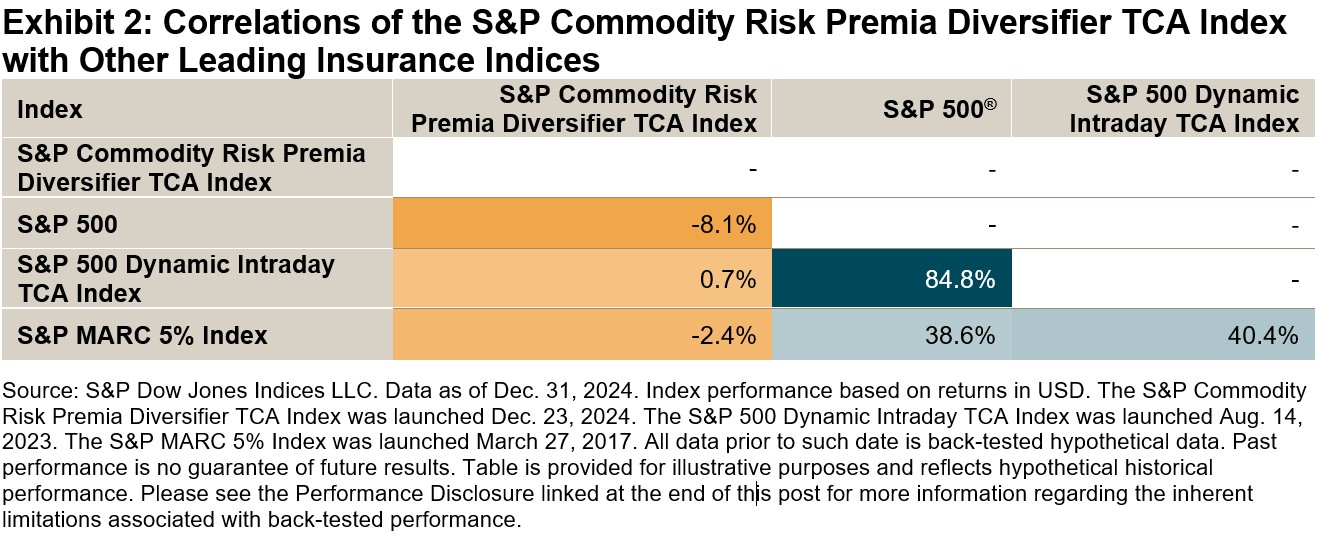

Based on back-tested data, the index reduced sensitivity to large equity market movements and demonstrated low or even negative correlations to other leading indices found within index-linked insurance products.

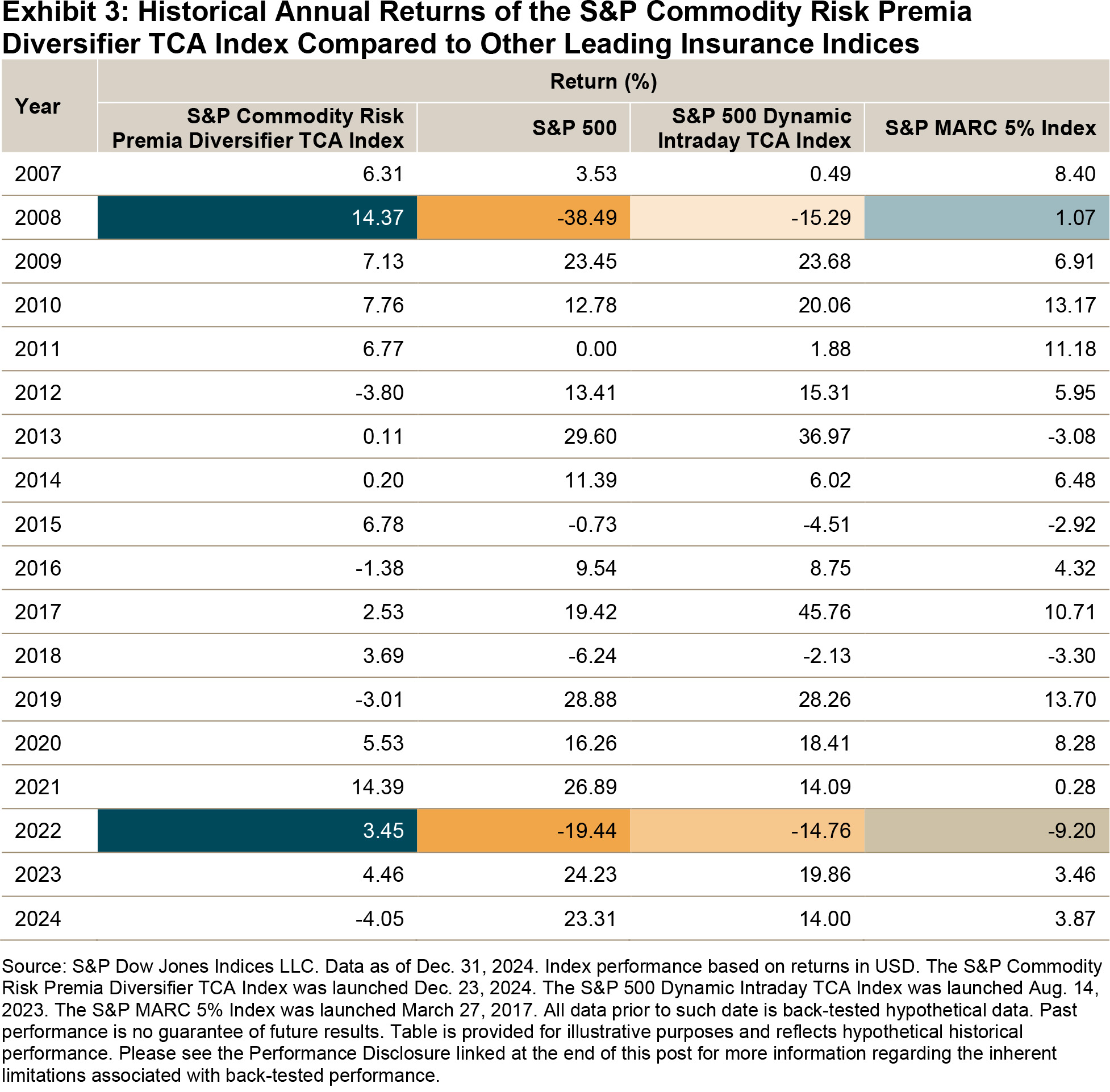

A comparison of annual returns of the S&P Commodity Risk Premia Diversifier TCA Index and several other mainstream indices highlights the potential diversification benefits of the index during market downturns. For example, in 2008 and 2022, which were particularly challenging years for equity markets, the S&P Commodity Risk Premia Diversifier TCA Index gained 14.37% and 3.45%, respectively, based on back-tested data.

In conclusion, the framework of the S&P Commodity Risk Premia Diversifier TCA Index seeks to stabilize volatility through diversified commodity risk premia exposure. By employing alternative risk premia strategies, the index may help mitigate risk during equity market downturns and provide protection during inflationary environments. This index emphasizes the importance of diversification in achieving a well-rounded strategy.

The posts on this blog are opinions, not advice. Please read our Disclaimers.