Since its launch in July 2022 to year-end 2024, the S&P 500® Equal Weight ESG Index achieved a cumulative outperformance of 0.86% compared to its benchmark, the S&P 500 Equal Weight Index. Gaining insight into the factors behind this outperformance highlights important aspects of environmental, social and governance (ESG) attributes that function differently from those in market-cap indices like the S&P 500 ESG Index.

To investigate the ESG attributes contributing to the S&P 500 Equal Weight ESG Index’s performance, we created hypothetical ESG quintile compositions by count and reconstituted them annually. This was done by ranking the S&P 500 Equal Weight Index’s constituents based on their ESG scores and assigning them to one of the five compositions, from highest to lowest ESG score, akin to previous assessments1 conducted on the S&P 500 ESG Index. The hypothetical equal-weighted performance of these compositions was then calculated and used to create a Brinson-like ESG attribution analysis,2 teasing out the importance of ESG score exposures in the performance of the S&P 500 Equal Weight ESG Index.

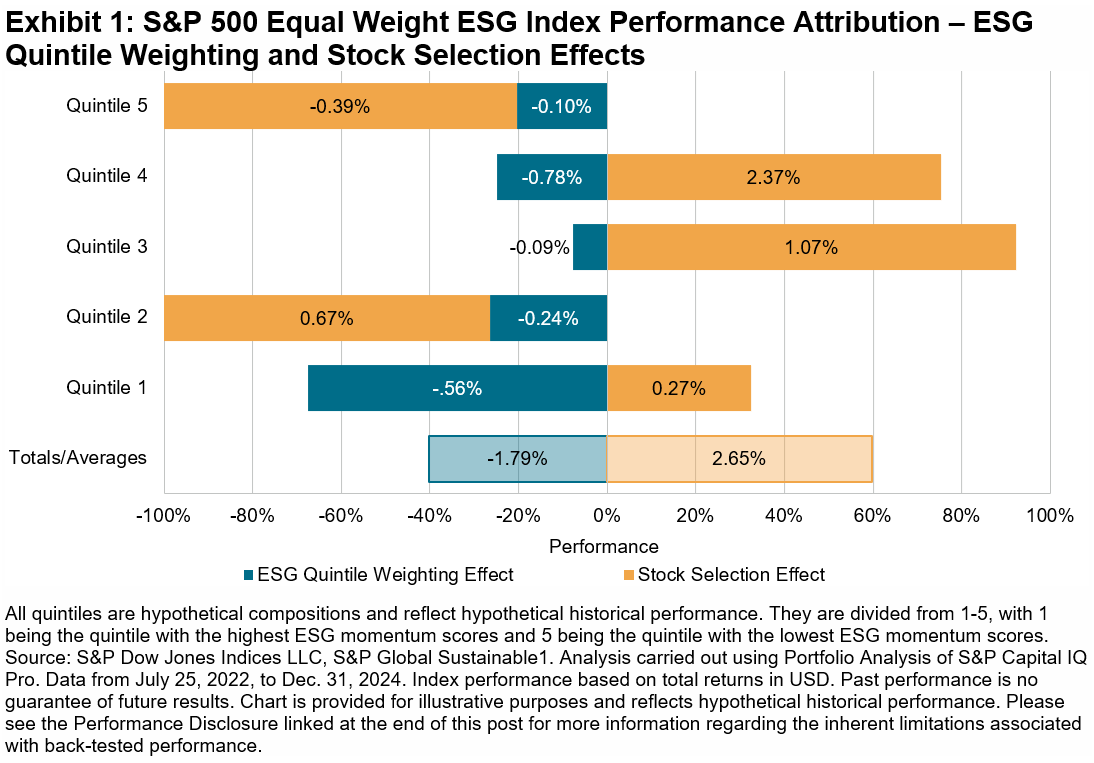

Exhibit 1 illustrates the results of this analysis, measuring the contribution of ESG quintile weighting and stock selection effects to the S&P 500 Equal Weight ESG Index’s excess return relative to the S&P 500 Equal Weight Index since its launch.3 To emphasize the relative impact of ESG quintile weighting and stock selection effects, the exhibit shows the proportion of the total impact, with their absolute values summing to 100% and the actual return impact shown in the labels.

Our findings reveal that the S&P 500 Equal Weight ESG Index’s performance was predominantly driven by stock selection effects rather than ESG quintile weighting effects. Specifically, stock selection contributed 2.65% to the index’s excess return, while ESG quintile weighting had a negative impact of 1.79%. This resulted in a total cumulative excess return of 0.86%. Of the five ESG quintiles, the ESG quintile weighting effect exceeded the stock selection effect in just one: Quintile 1.

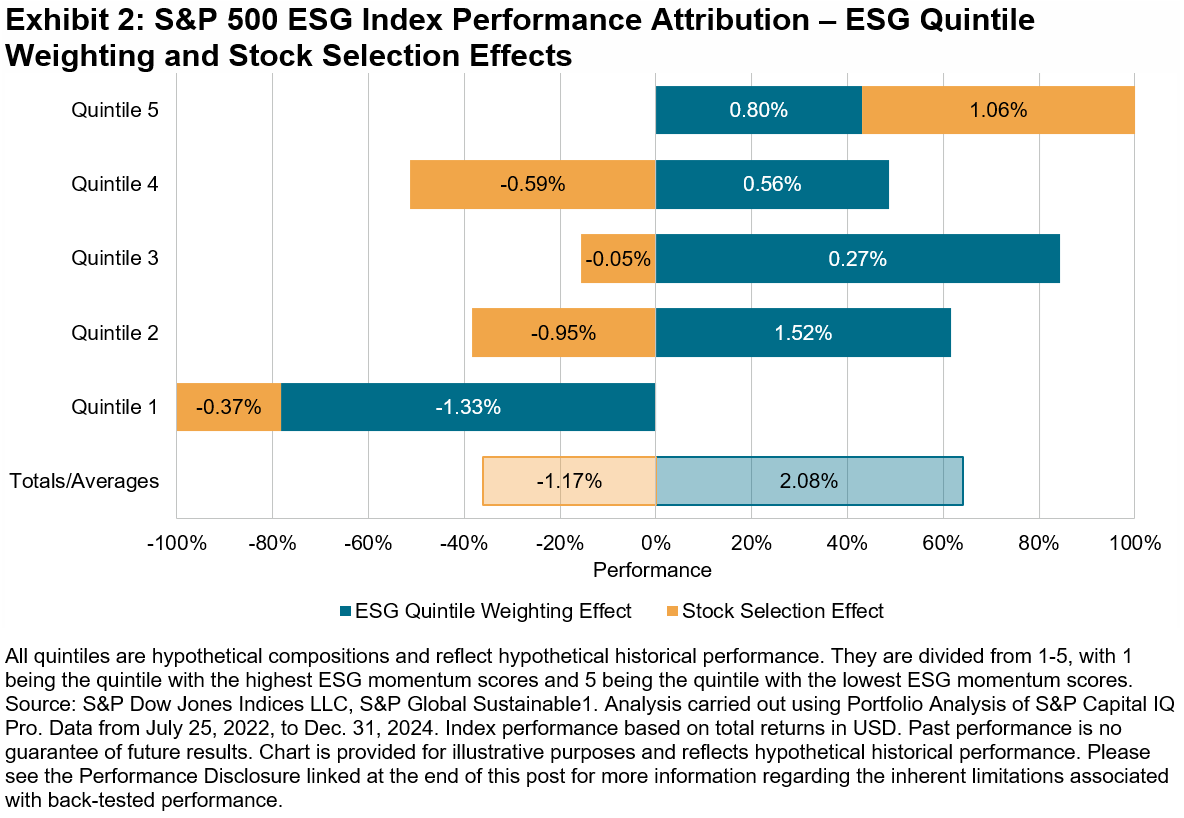

This conclusion contrasts with the performance drivers observed in the S&P 500 ESG Index during the same period, as illustrated in Exhibit 2. The S&P 500 ESG Index achieved a cumulative excess return of 0.91% against the S&P 500, with more than 60% of this excess return driven by ESG quintile weighting effects. 4

The varied performance drivers highlight the significant impact that index construction methodologies can have on performance. The S&P 500 Equal Weight ESG Index5 can benefit from an approach that emphasizes the selection of companies with higher ESG scores across market capitalizations. This could enable it to tap into the value generated by smaller firms, which can be overlooked in cap-weighted indices.

As the growing emphasis on sustainable investing continues to shape market participants’ preferences and the drivers of relative performance in the S&P 500 Equal Weight Index6 continue to attract attention, these findings could serve as a crucial reference for market participants looking into this index’s ESG variant. For those interested in exploring more about S&P DJI’s sustainability-focused indices, additional information is available in the Sustainability Index Dashboard.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

1 For a thorough description of the hypothetical ESG quintile compositions and the drivers behind the excess return in the S&P 500 ESG Index, see Beyhan, Maya, “Charting New Frontiers,” S&P Dow Jones Indices LLC, Sept. 06, 2024.

2 For more information on this widely used performance attribution model, see Brinson, Gary P., L. Randolph Hood and Gilbert L. Beebower, “Determinants of Portfolio Performance,” Financial Analysts Journal, July-August, 1986.

3 Analysis carried out using Portfolio Analytics on S&P Capital IQ Pro.

4 Analysis carried out using Portfolio Analytics on S&P Capital IQ Pro.

5 See the S&P Equal Weight ESG Indices Methodology.

6 For a thorough overview of the potential sources and drivers of relative performance in the S&P 500 Equal Weight Index, see Ganti, Anu R., Tim Edwards and Hamish Preston, “Worth the Weight,” S&P Dow Jones Indices LLC, July 23, 2024.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

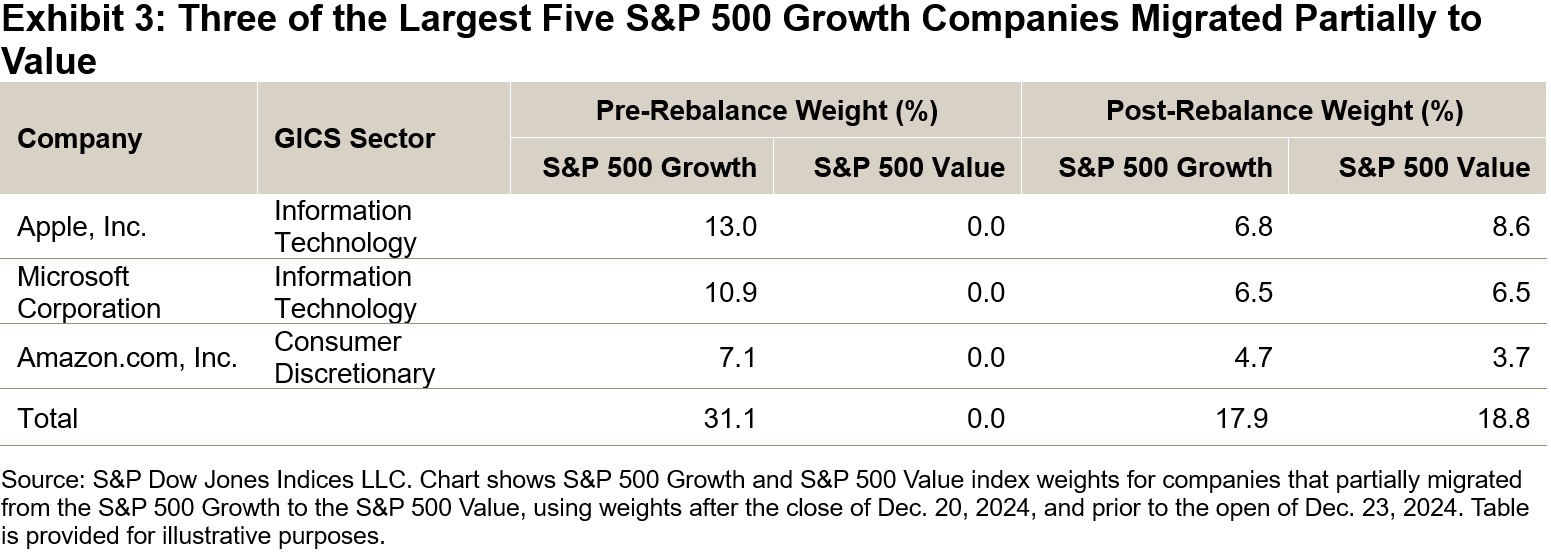

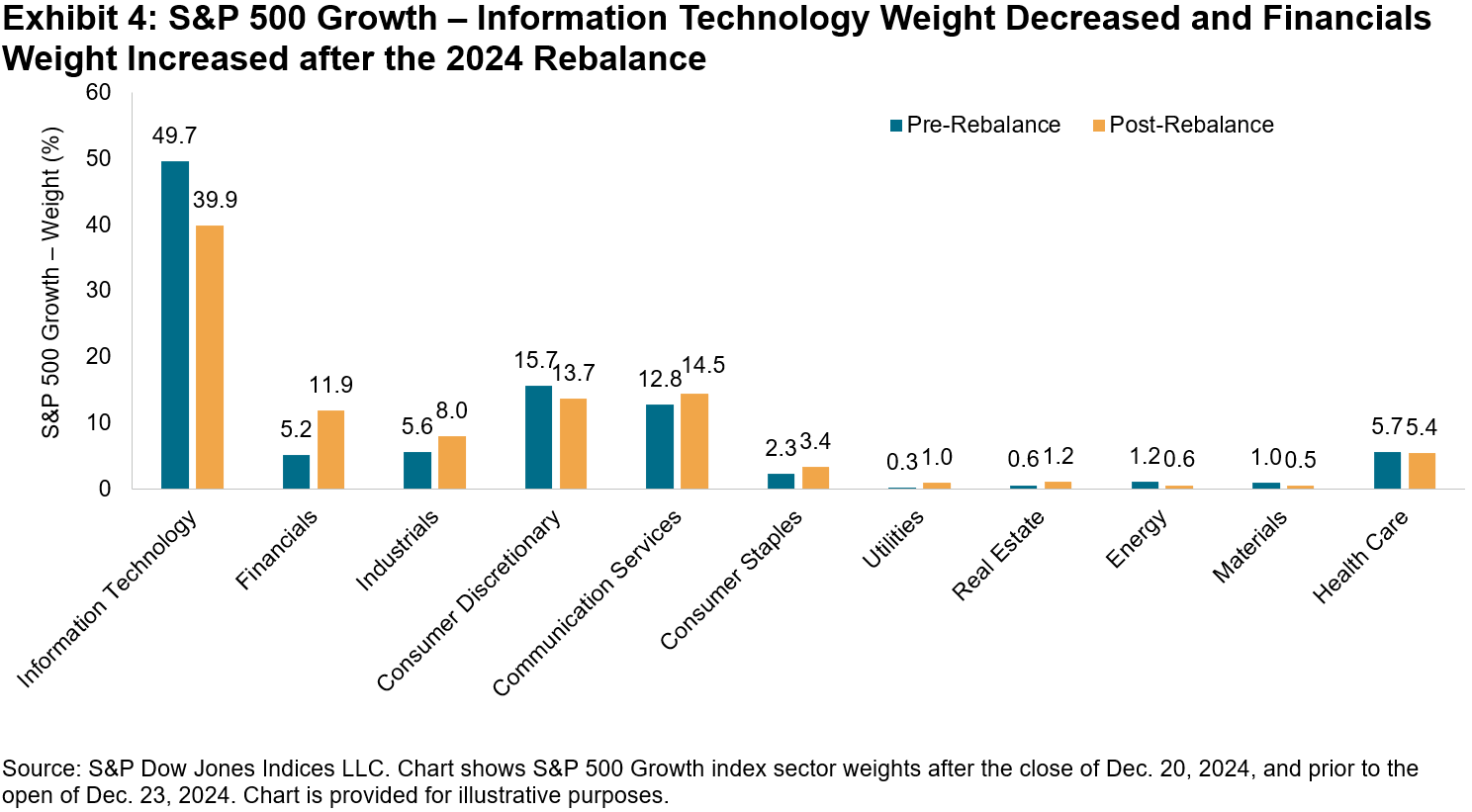

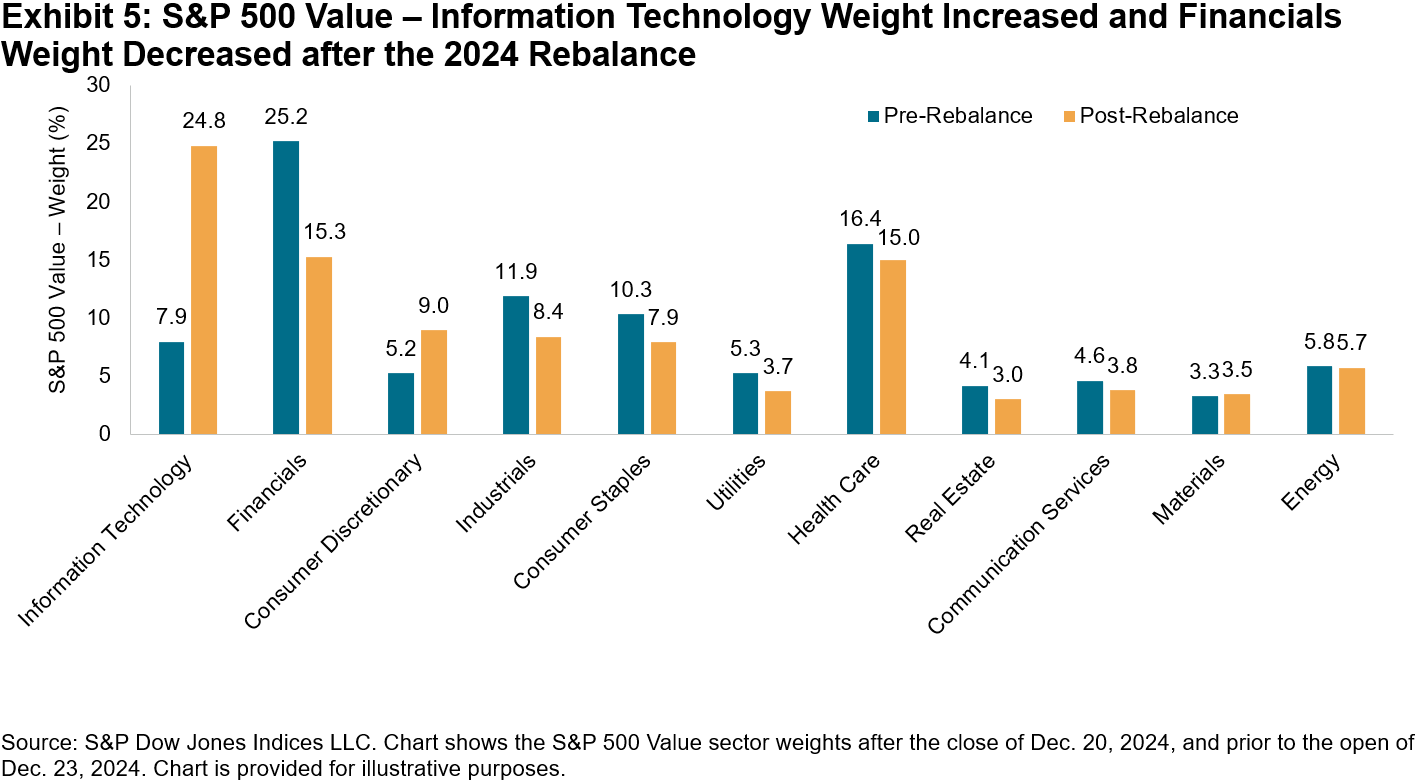

Notably, three of the five largest S&P 500 Growth companies pre-rebalancing—Apple, Microsoft and Amazon (representing 31.3% of the S&P 500 Growth’s weight)—moved to the blended basket. These companies migrated due to a decline in their Growth Score: Apple ranked lower in sales growth and earnings growth relative to the underlying index (the broader basket), while Amazon and Microsoft experienced declines in earnings growth and sales growth relative to the growth basket. Only Microsoft ranked lower in momentum relative to the broader basket.

Notably, three of the five largest S&P 500 Growth companies pre-rebalancing—Apple, Microsoft and Amazon (representing 31.3% of the S&P 500 Growth’s weight)—moved to the blended basket. These companies migrated due to a decline in their Growth Score: Apple ranked lower in sales growth and earnings growth relative to the underlying index (the broader basket), while Amazon and Microsoft experienced declines in earnings growth and sales growth relative to the growth basket. Only Microsoft ranked lower in momentum relative to the broader basket.