Launched in 2007, the S&P Global Clean Energy Index has been a headline benchmark for measuring clean energy-related companies’ performance over the past 16 years. In April 2021, we launched the S&P Global Clean Energy Select Index to measure the 30 largest companies in global clean energy businesses listed on developed market exchanges.

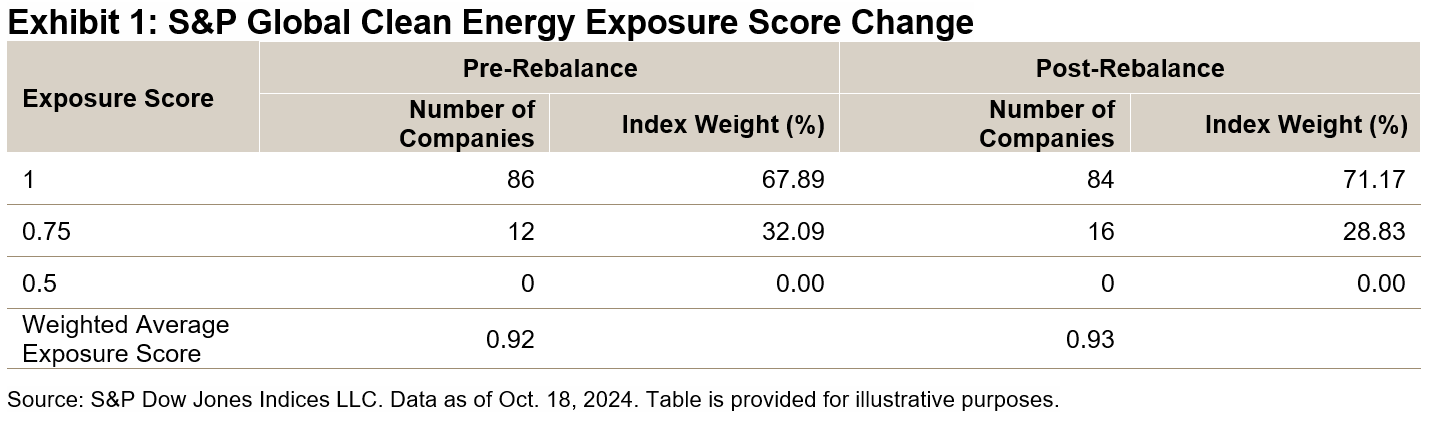

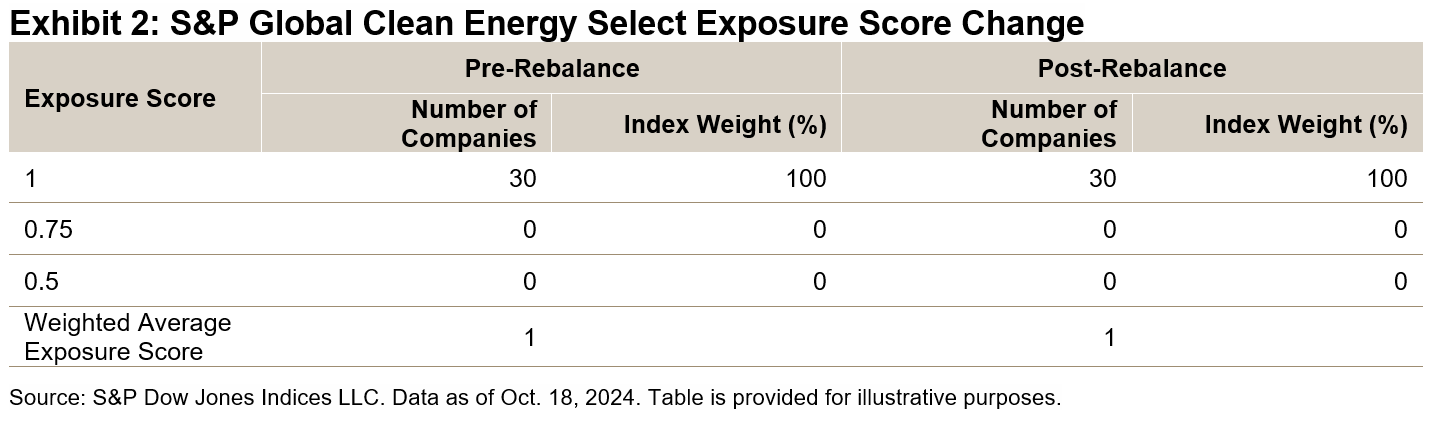

Both indices had their semiannual rebalances on Oct. 18, 2024. The index methodology categorizes companies into four exposure score buckets ranging from 0 to 1, with a 0.25 increment, to measure their clean energy business purity. Exhibits 1 and 2 show the change in exposure before and after the October rebalance for both indices. For the S&P Global Clean Energy Index, the weighted average exposure score of the index increased slightly from 0.92 to 0.93. The S&P Global Clean Energy Select Index consists of 30 companies with an exposure score of 1 listed in the developed market exchanges (see Exhibit 2).

In the market allocation breakdown, significant changes in the S&P Global Clean Energy Index following the rebalance include a 6.41% increase in the weight of the U.K. and a 2.13% increase for Brazil, alongside an 8.80% decrease for the U.S. Meanwhile, for the S&P Global Clean Energy Select Index, Portugal’s weight rose by 4.04%, while the weights of South Korea and Brazil experienced declines of 3.11% and 2.92%, respectively.

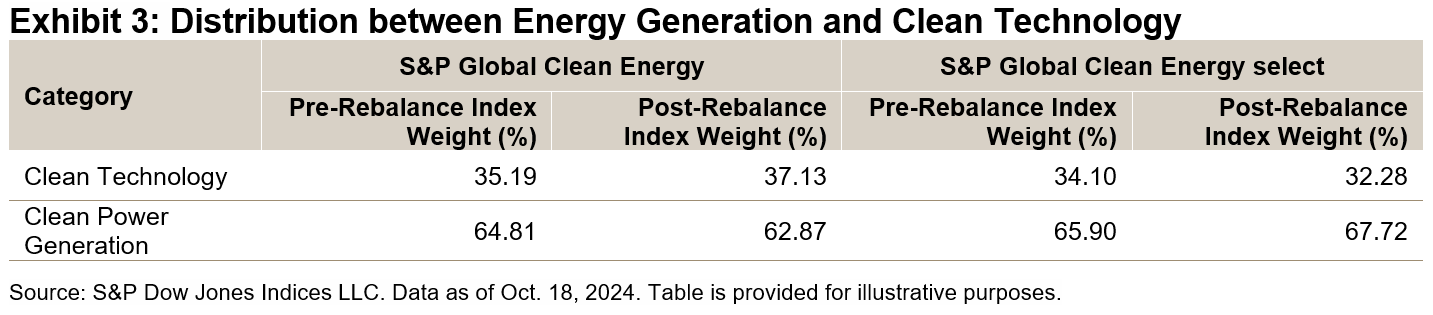

The S&P Global Clean Energy Index and the S&P Global Clean Energy Select Index track both the performance of clean energy technology firms and clean power generation companies (see Exhibit 3). During the recent rebalance, the index weight of clean technology in the S&P Global Clean Energy Index increased, primarily driven by a 1.12% rise in the index weight for the FactSet Revere Business Industry Classifications System (RBICS) subindustry of Wind Energy Equipment Manufacturing. Conversely, the index weight for clean power generation decreased, largely due to a 7.4% weight decrease in the RBICS subindustry of United States Northeast Electric Utilities.

The composition change of the S&P Global Clean Energy Select Index was different, featuring a decrease in clean technology weight alongside an increase in clean power generation weight. Within clean technology, there was a 3.39% drop in the RBICS subindustry of Photovoltaic and Solar Cells and Systems Providers. Meanwhile, clean power generation saw a 3.3% increase in the RBICS subindustry of Europe Mixed Alternative Wholesale Power and a 1.6% rise in the RBICS subindustry of Europe Solar Wholesale Power.

The inclusion or exclusion of constituents within the S&P Global Clean Energy Select Index could be a result of the change on exposure score, or it could be due to the market movements that changed the relative float market capitalization ranking of companies within the S&P Global Clean Energy Index. For exposure score information, please refer to S&P DJI’s Client Resource Center.

S&P Global Clean Energy Index Performance YTD in 2024

Underperforming the S&P Global BMI YTD, the S&P Global Clean Energy Select Index was down 25.78% and the S&P Global Clean Energy Index was down 19.93% in USD total return terms. Dispersion was high among constituents of the S&P Global Clean Energy Index. SolarEdge Technologies (-83.12%), Shoals Technologies (-66.41%) and Hanwha Solutions Corporation (-61.58%) were among the lagging performers, while Suzlon Energy (up 61.24%) and NHPC (up 23.55%) made positive contributions, partially offsetting some of the losses.

We recently published the paper “Navigating the Clean Energy Transition: Market Dynamics and Performance Insights,” which delves into the market dynamics around the clean energy transition. The paper outlines the energy transition process, provides an overview and performance review of the S&P Global Clean Energy Indices, discusses ongoing policy support for the energy transition and presents a quantitative analysis of performance. For those seeking a deeper understanding of these topics, the paper offers valuable perspectives on the current state and future potential of the clean energy transition.

The posts on this blog are opinions, not advice. Please read our Disclaimers.