On Oct. 1, 2024, a new presidential administration took office in Mexico amid a series of constitutional reforms and a new political landscape. Political change can create uncertainty, so it is useful to analyze past periods to identify trends and gain insights on the effects of similar events.

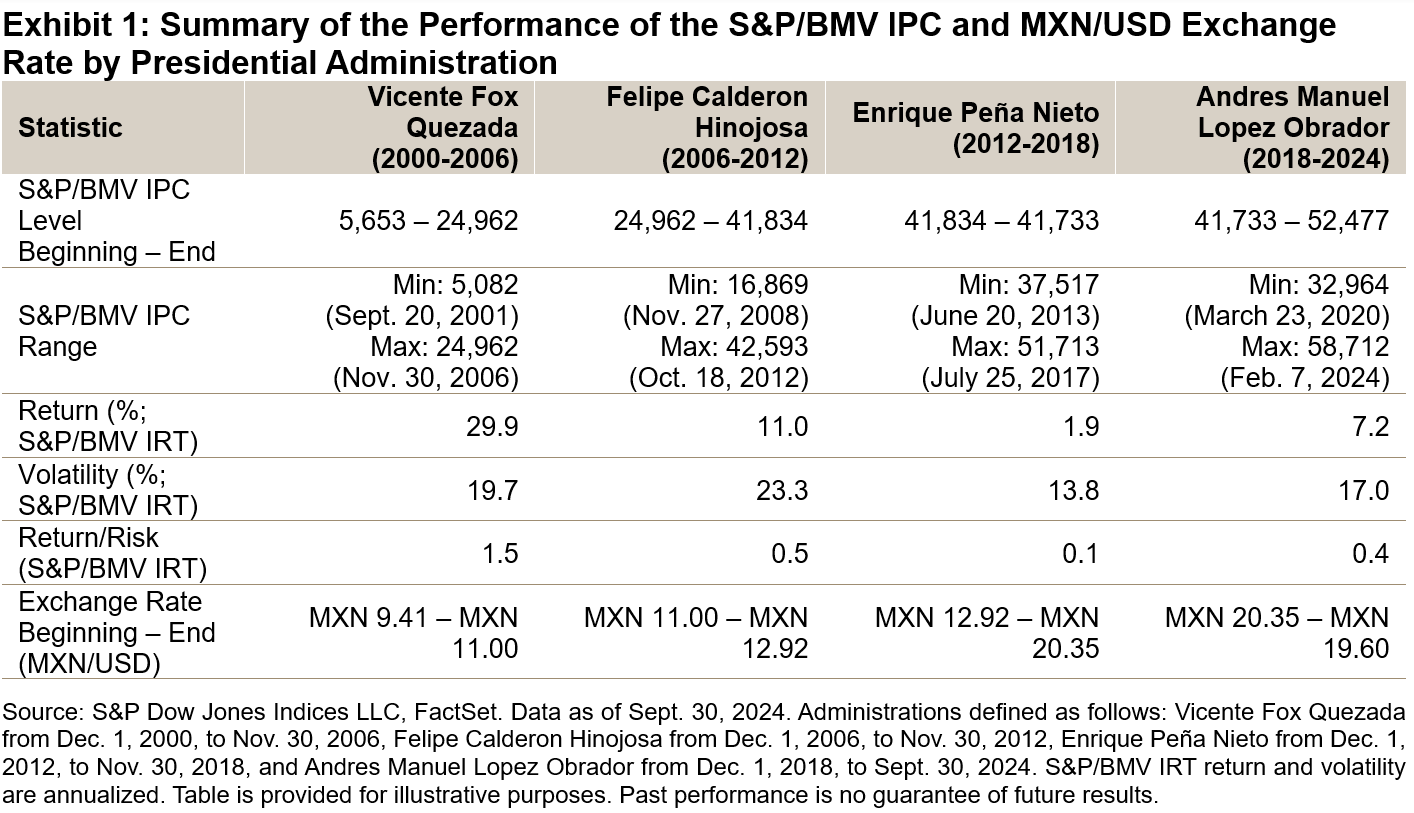

How did the S&P/BMV IPC and the MXN/USD exchange rate perform during the outgoing administration and how did this compare to other periods? Exhibit 1 shows a summary of the performance of the S&P/BMV IPC and the MXN/USD exchange rate since 2000.

The S&P/BMV IPC has delivered varied but positive returns in the past four administrations. We can observe that the annualized performance of the S&P/BMV IRT increased significantly in the past administration, going from 1.9% to 7.2%, though still below what we saw in the 2000s. In terms of volatility, the past six years saw a slight increase compared to the previous period; however, if we look at the return/risk ratio, the additional risk was offset by higher returns.

The exchange rate closed with a marginal appreciation when compared to its 2018 level, although just before the 2024 elections, it had appreciated by over 16%. In any case, this is noteworthy as this was the first administration in which the Mexican peso did not depreciate.

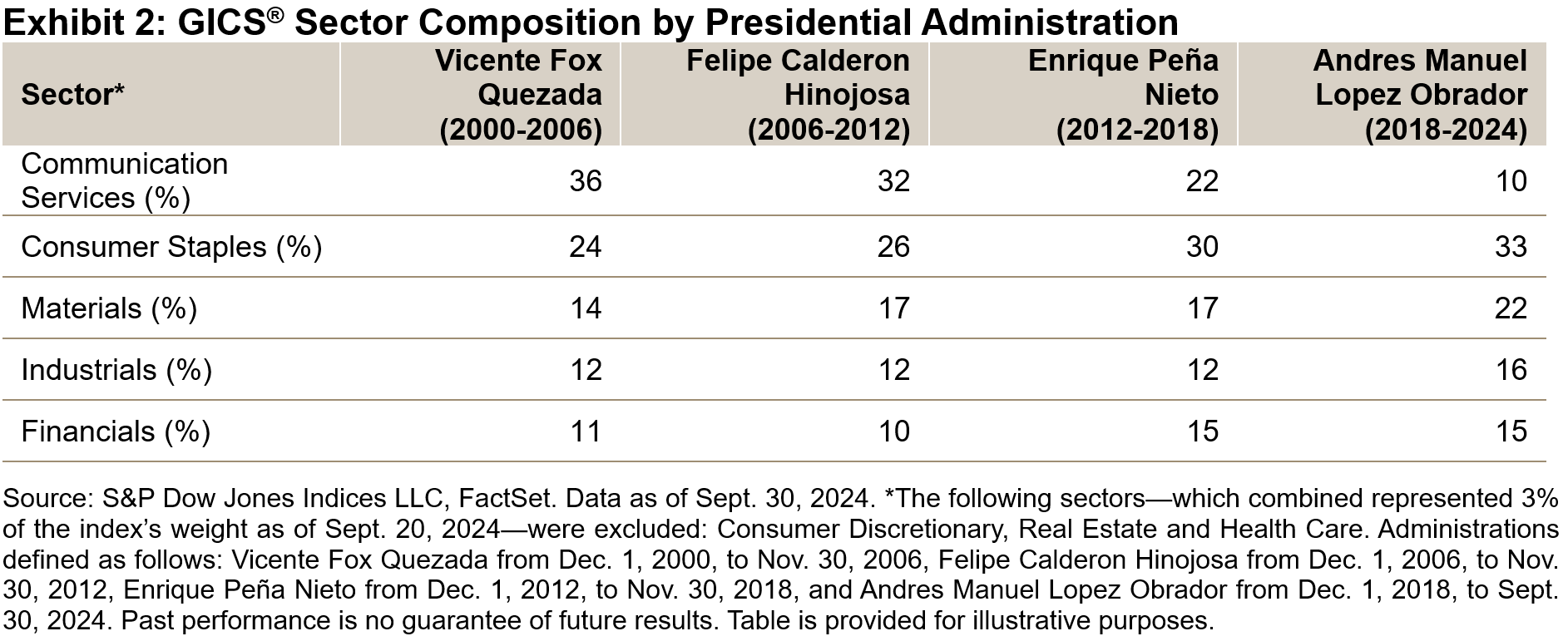

From a sector perspective, there have been notable changes in the largest sectors these past six years. Communication Services continued to shrink in share, from a high of 37% in 2006 to 10% in 2024. In the period from 2018-2024, Materials and Industrials gained 6% and 4%, respectively, while Financials decreased by 3% and Consumer Staples remained flat at 33%.

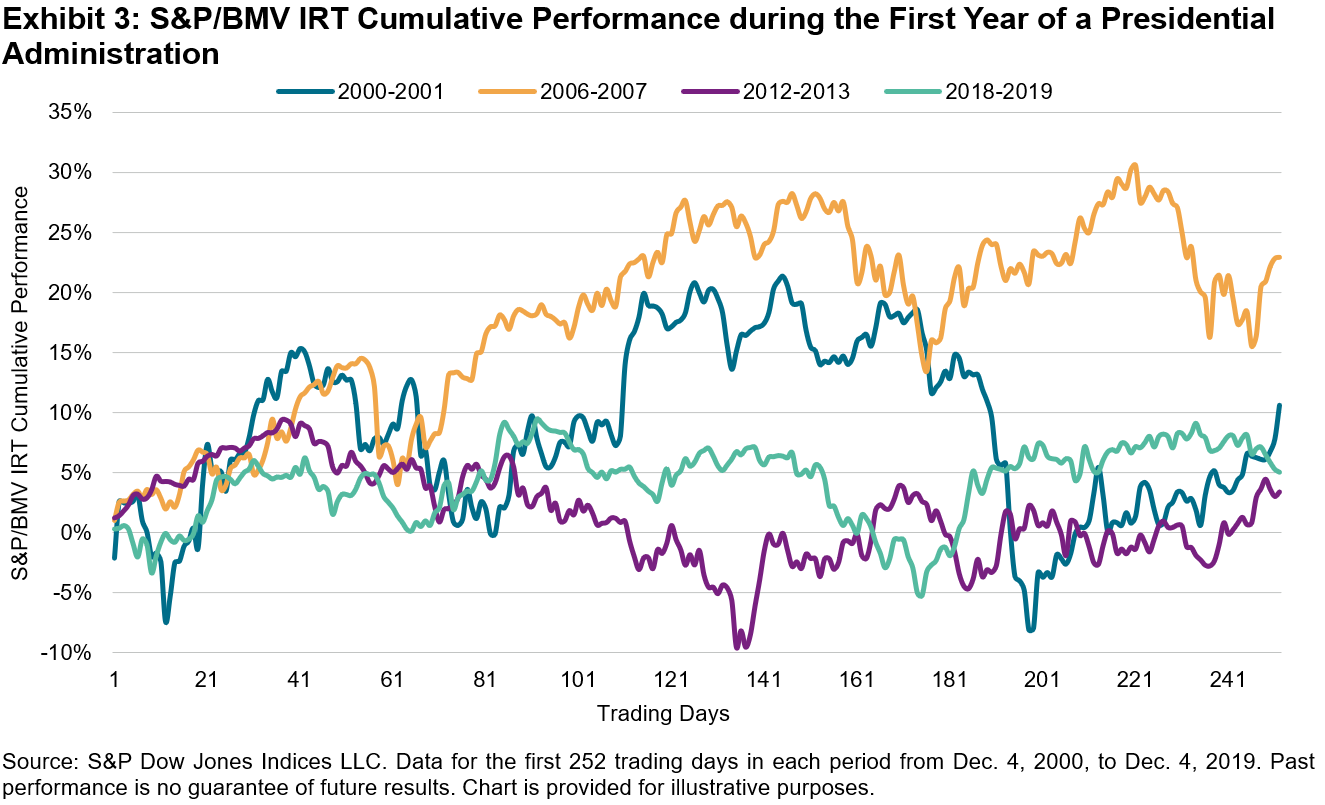

The first year of a new administration in Mexico tends to be eventful, as there are often major changes in policy. In addition, this can be exacerbated by external events, such as a global financial downturn or the U.S. presidential elections.

In Exhibit 3 we see the cumulative performance of the S&P/BMV IRT during the first year of each administration since 2000. Though each administration faced its own challenges, one thing they all have in common is that the S&P/BMV IRT ended their first year with positive returns.

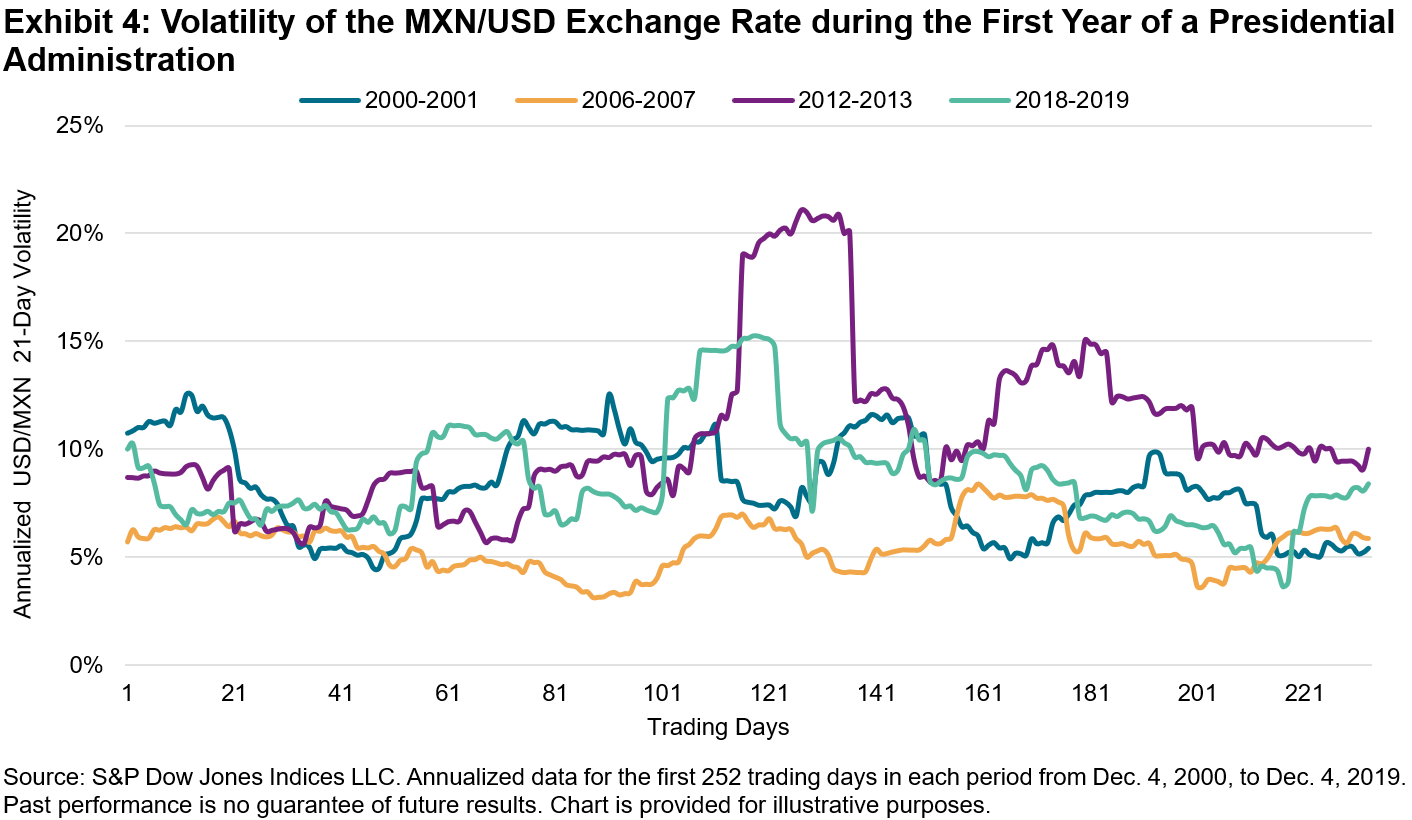

Exhibit 4 illustrates the exchange rate volatility during the first year of each administration. While many factors influence exchange rates it is interesting that the level of MXN/USD volatility ended each administration’s first year roughly where it started, despite some short-term bouts of volatility during the year. The most volatile first year of an administration was seen in the period from 2012-2013, where annualized 21-day volatility reached 21%.

In conclusion, an administration’s effect on the equity market and the exchange rate in Mexico is better observed from a long-term perspective, as high levels of volatility, which tend to be short-lived, can create uncertainty but not necessarily mark a trend. Insights gained from these analyses could help market participants make informed decisions in the face of change.

The posts on this blog are opinions, not advice. Please read our Disclaimers.