In recent years, the global financial landscape has witnessed a significant shift toward sustainability considerations as investment themes. As market participants seek to understand the relative performance of sustainability-focused indices, it is essential to explore the underlying drivers of ESG dynamics in both developed and emerging markets.

In a previous analysis, we focused on ESG momentum—measured at the company level simply as the year-over-year absolute change in the ESG score—and its impact on the performance of the S&P 500® ESG Index when compared to the S&P 500, representing the U.S. equities market. Similarly, the dynamics operating within the S&P/BMV Total Mexico ESG Index provide a case study for assessing the impact of ESG momentum on the index’s relative performance against its benchmark, the S&P/BMV Total Mexico Index.

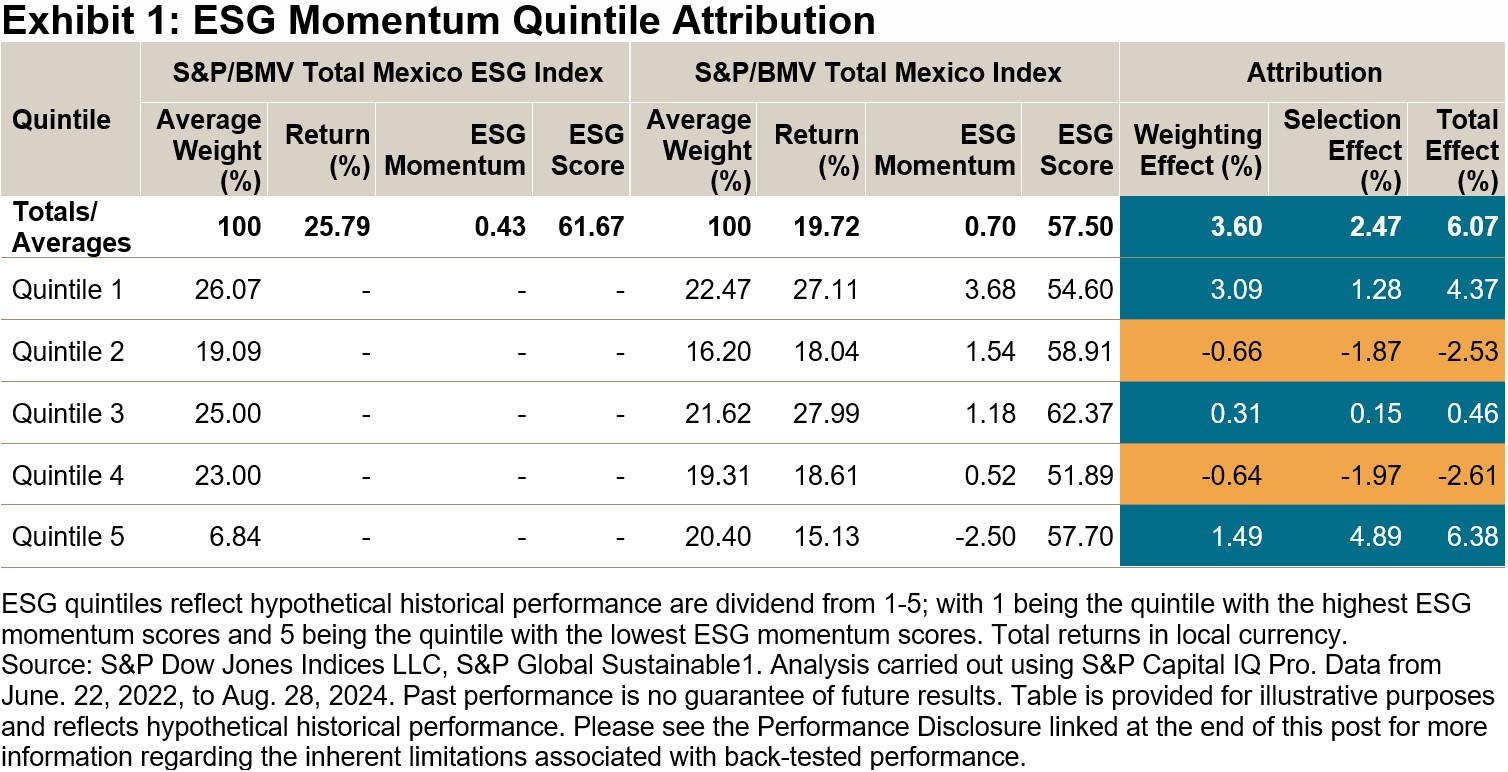

During the time frame studied, from June 22, 2022, to Aug. 28, 2024, the S&P/BMV Total Mexico ESG Index outperformed its benchmark, the S&P/BMV Total Mexico Index, by 6.07%, cumulatively. To examine the effect of ESG momentum on this outperformance, we created hypothetical ESG momentum quintile compositions1 by ranking the S&P/BMV Total Mexico Index’s constituents by their ESG momentum score and assigning each of them to one of the five compositions, from the highest to the lowest ESG momentum-scoring. The hypothetical market-cap-weighted performance of these quintile compositions was then calculated and used to create an ESG momentum attribution analysis, underscoring the importance of ESG momentum exposure in the performance of the S&P/BMV Total Mexico ESG Index.

Exhibit 1 summarizes the results of this analysis, including the average weights of the S&P/BMV Total Mexico ESG Index and the S&P/BMV Total Mexico Index in each ESG momentum quintile (from high to low scoring), the corresponding quintile composition and index returns, as well as a summary of the corresponding weighting and selection effects over the full period.2

Like our observations in the U.S. market,1 the S&P/BMV Total Mexico ESG Index benefitted the most from an underweight in the worst ESG momentum-scoring constituents, i.e., Quintile 5. This quintile underperformed by 4.59% relative to the S&P/BMV Total Mexico Index. On average, the S&P/BMV Total Mexico ESG Index underweighted Quintile 5 by 13.56%, generating 1.49% in excess return from the weighting effect. Combined with a selection effect of 4.89%, it resulted in a 6.38% excess total return for the S&P/BMV Total Mexico ESG Index for this quintile.

However, the S&P/BMV Total Mexico ESG Index also benefitted from overweighting the best ESG momentum-scoring constituents, i.e., Quintile 1, which achieved a cumulative outperformance of 7.39% relative to the S&P/BMV Total Mexico Index, a trend that was not seen in the U.S. market analysis. On average, the S&P/BMV Total Mexico ESG Index overweighted this quintile by 3.60%, generating 3.09% in excess return from the weighting effect. Taken together with the selection effect, the total contribution was 4.37% in excess return for the S&P/BMV Total Mexico ESG Index for this quintile.

These findings highlight that the best ESG momentum-scoring constituents in the S&P/BMV Total Mexico ESG Index not only outperformed the S&P/BMV Total Mexico Index but also demonstrated significant improvements in their ESG scores without sacrificing performance.

1 For more details on this methodology, see Beyhan, Maya, “Charting New Frontiers: The S&P 500 ESG Index’s Outperformance of the S&P 500”, S&P Dow Jones Indices LLC, Sept. 6, 2024.

2 Analysis carried out using S&P Capital IQ Pro.

The posts on this blog are opinions, not advice. Please read our Disclaimers.