Many investors tend to overweight domestic equities, a phenomenon known as home bias. Mexican investors may be inadvertently neglecting the breadth of global equity markets by focusing primarily on local options. The significant representation of the U.S. equity market means that some investors risk overlooking a significant portion of the global equity market and the potential diversification benefits from incorporating U.S. equity exposures.

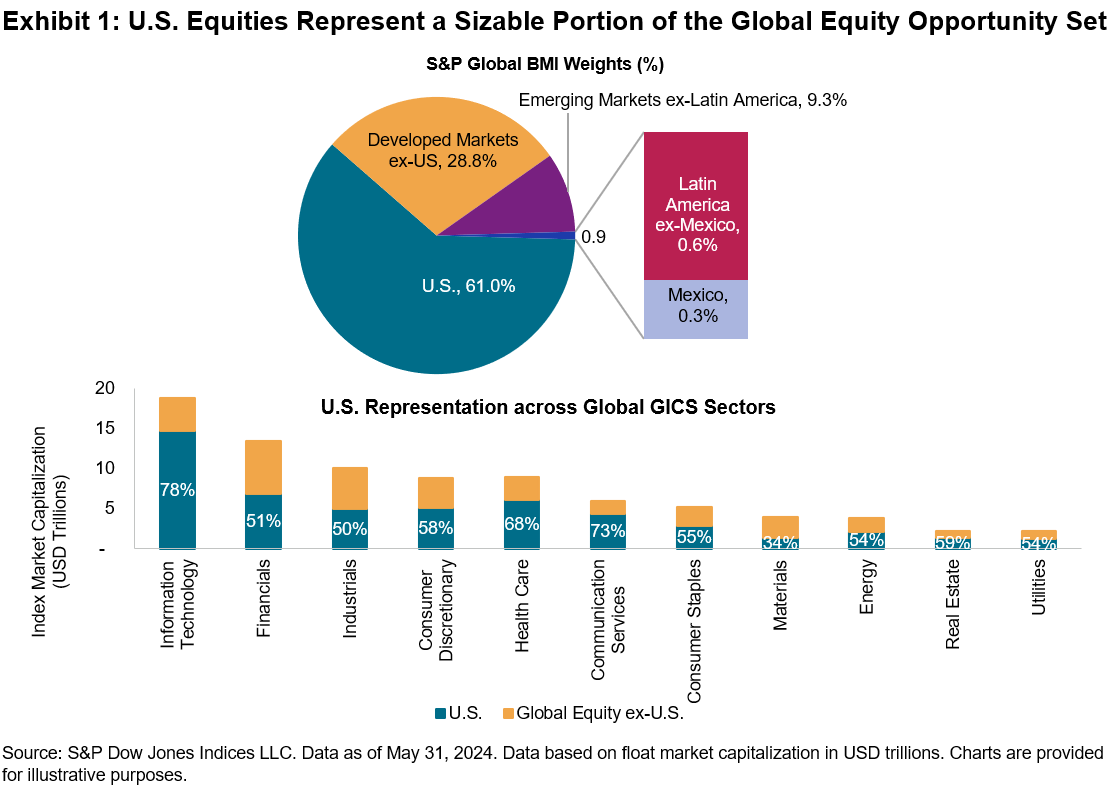

The global relevance of the U.S. equity market can be illustrated by its size: U.S.-domiciled companies represent around 60% of the global equity market capitalization, as represented by the S&P Global BMI. This representation is far higher than the weight of Latin America (0.9%) and Mexico (0.3%). As a result, the consideration of U.S. equities can help investors gain a clearer understanding of global equity performance and support the expression of strategic and tactical views. This is also relevant at a sector level: U.S. companies account for most of the global equity opportunity set in 10 out of 11 global GICS® sectors.

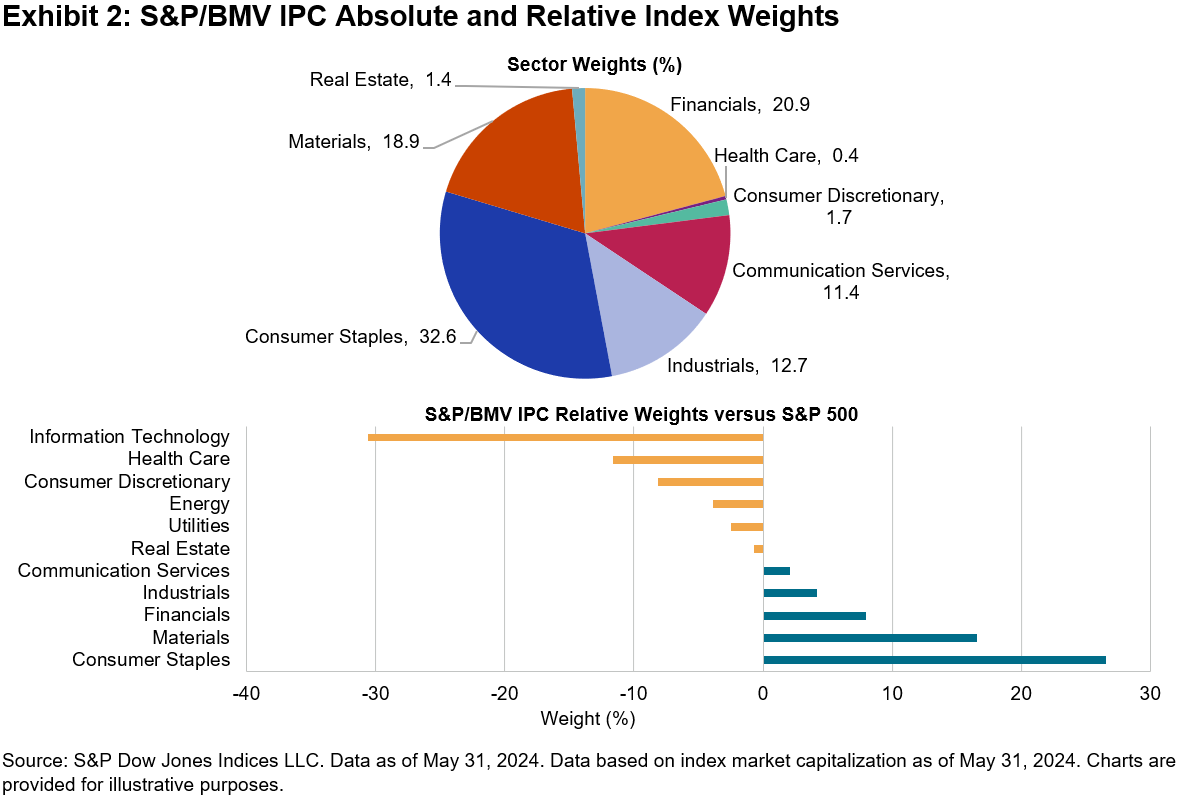

To further illustrate the relevance of U.S. equity exposure, we compare the distinct sectoral compositions of the S&P/BMV IPC and the S&P 500®. The S&P/BMV IPC tracks the performance of the largest and most liquid Mexican stocks. Exhibit 2 shows that, as of May 2024, the index had significant weightings in Consumer Staples, Financials and Materials. Conversely, the S&P 500 had higher exposure to Information Technology, Health Care, Consumer Discretionary, Energy and Utilities. Incorporating U.S. equities could therefore help Mexican investors to diversify domestic sector biases.

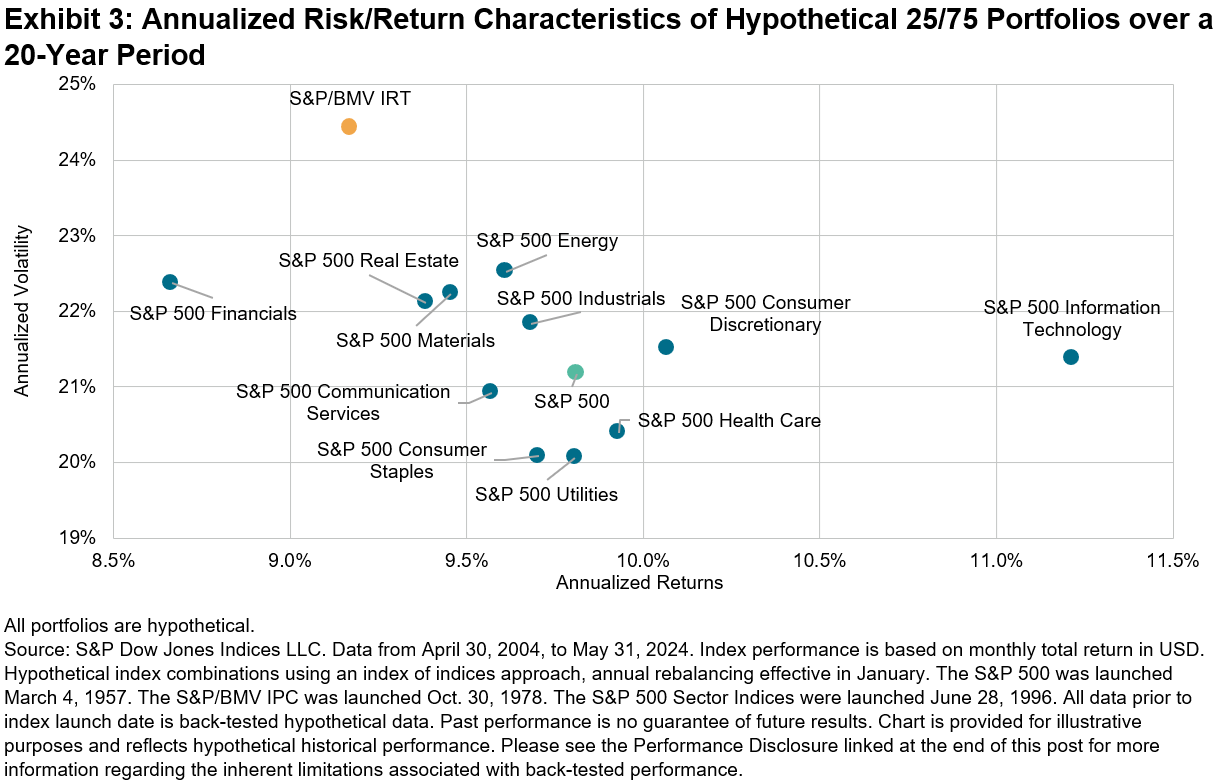

The performance of U.S. equities has historically presented potential diversification benefits to Mexican investors. We demonstrate this by building hypothetical portfolios that blend the S&P 500 and its GICS sector indices with the S&P/BMV IRT, allocating 25% to U.S. equities and 75% to local equities, rebalanced annually. Exhibit 3 indicates that this hypothetical approach yielded higher performance and lower volatility, historically, thereby improving the hypothetical portfolios’ long-term risk-adjusted returns.

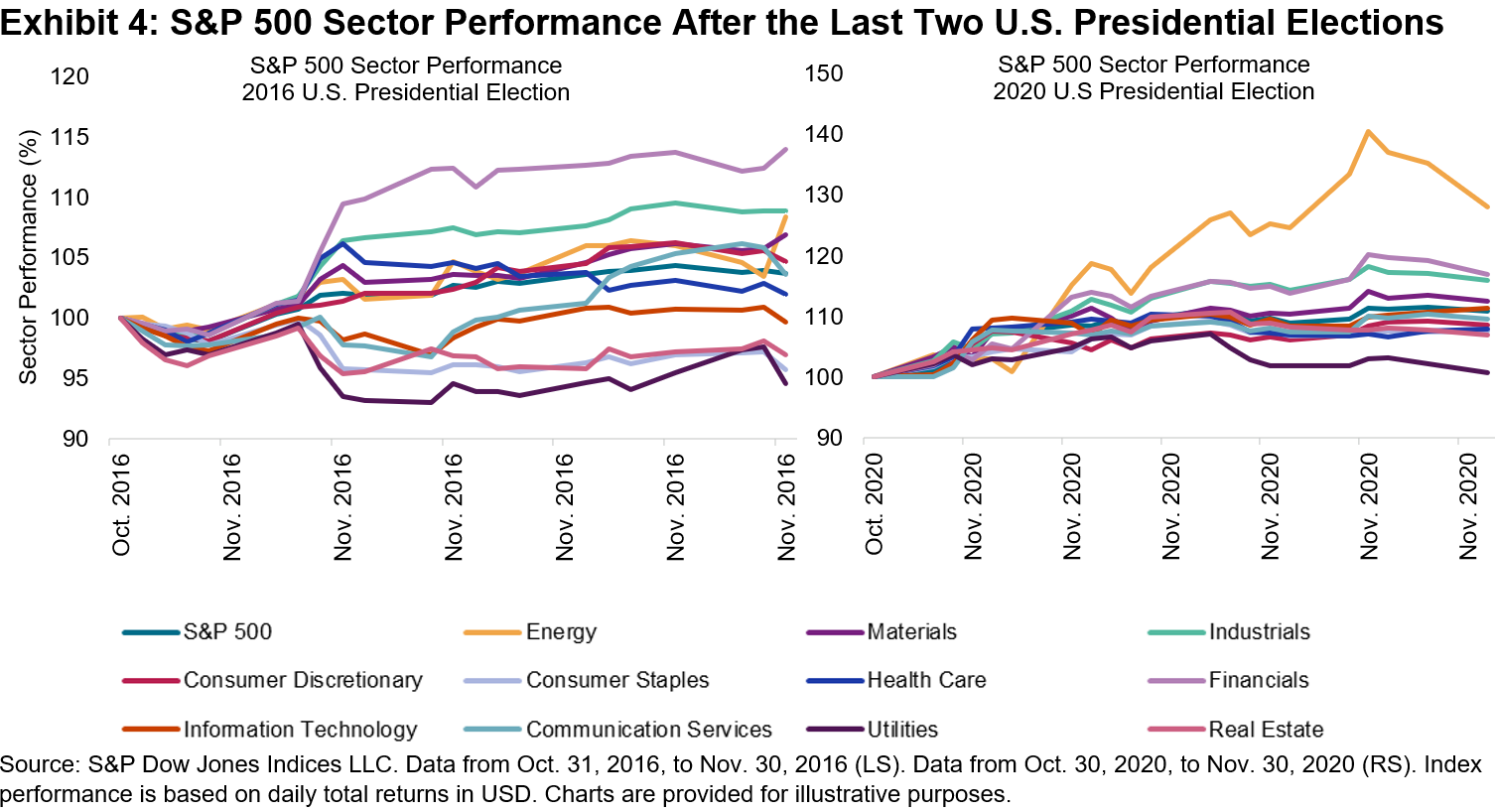

Beyond the strategic relevance of U.S. equities, the historical performance of U.S. sectors around U.S. Presidential elections has presented the idea of U.S. sectors having tactical relevance. Historically in election years, sector performance spreads have widened in November, as Exhibit 4 illustrates. While the S&P 500’s overall performance remained relatively stable in recent elections, sectoral fluctuations contributed to nearly half of the index’s monthly dispersion—a measure to determine the spread of stock returns within the index, highlighting the importance of sectors to express views.

The U.S. equity market represents a sizable portion of the global equity opportunity set. Incorporating U.S. equities not only potentially offers Mexican investors a way to alleviate domestic sectors biases, it has historically enhanced risk-adjusted returns. Additionally, U.S. sectors serve as the basis for market strategies and positioning, and our sector indices offer a measure for investors seeking to express both tactical and core portfolio views.

The posts on this blog are opinions, not advice. Please read our Disclaimers.