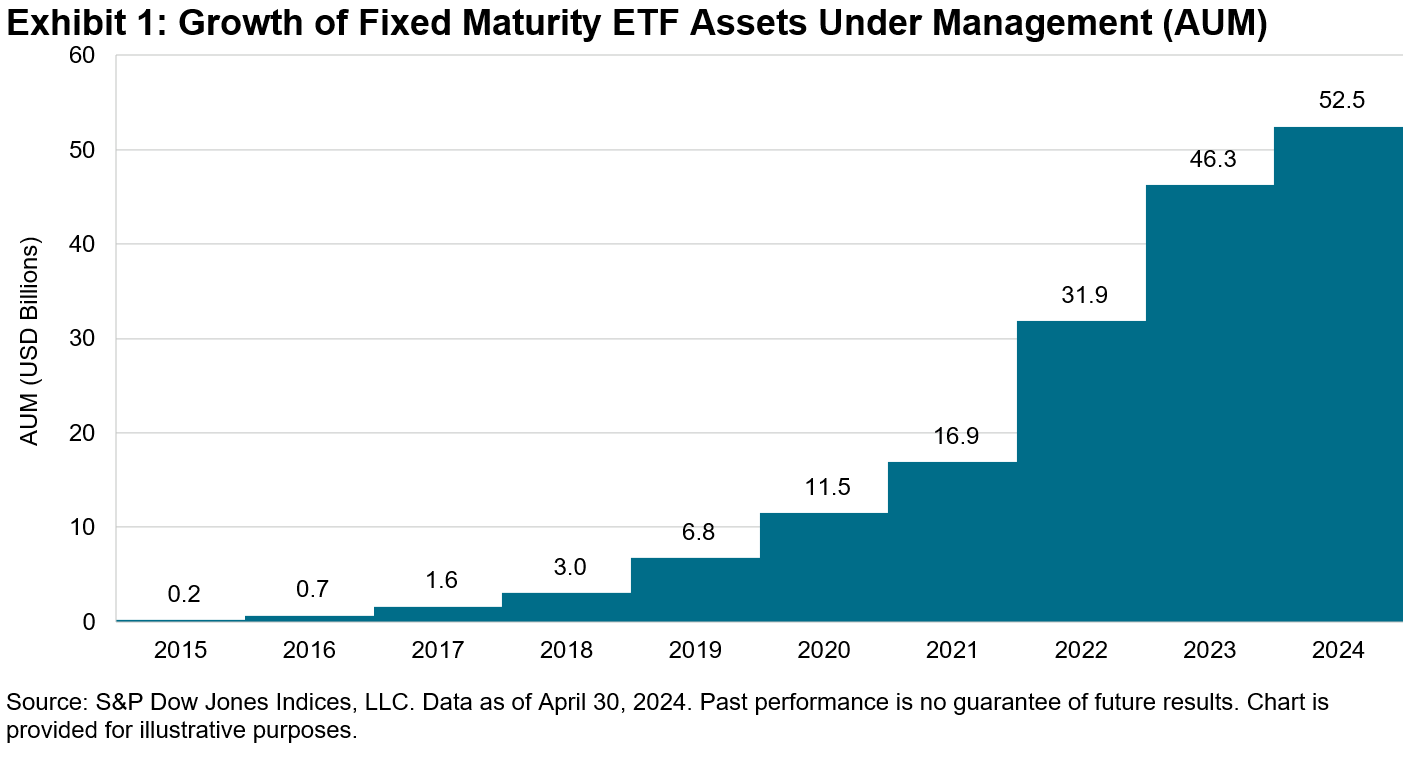

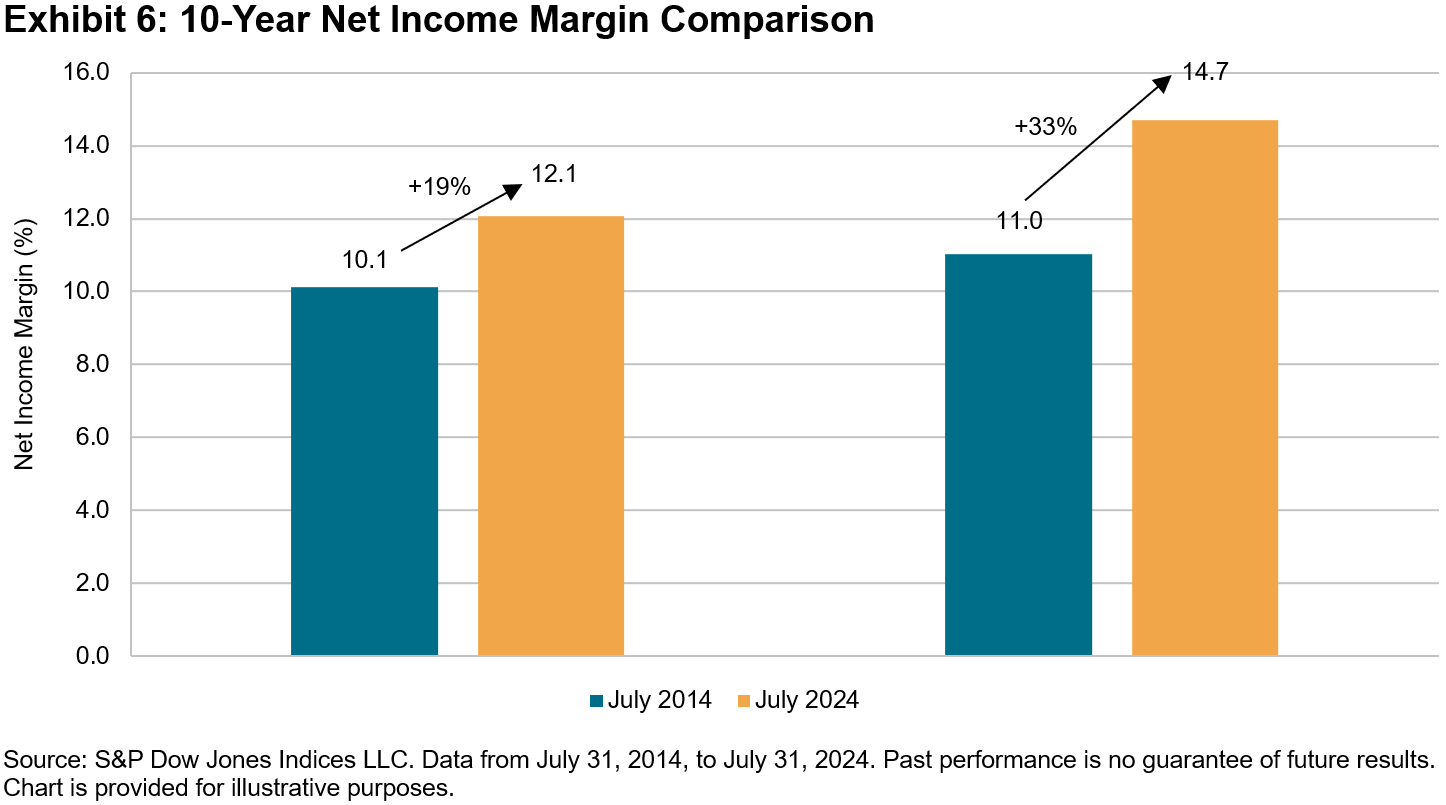

As fixed income index solutions continue to evolve, one notable innovation has been that of fixed maturity indices. Fixed maturity indices have existed in the U.S. for over 10 years, where growth and adoption have increased over that time. The market is newer in Europe, where adoption has taken shape over the last 12 months. As this market expands across geographies and exposures, we take a closer look at the construct and the utilization of the fixed maturity index.

What is a fixed maturity index? How is it different from a typical broad-based fixed income index?

A fixed maturity index is an index that holds bonds that expire within the same maturity year or period. For example, the iBoxx® USD Corporates 2029 Index holds only investment grade bonds that mature in the year 2029. It draws on the same broad-based, diversified investment grade corporate universe that represents the beta of the market, but filters for a specified year of maturity. In 2029, the final year of the index, maturing bond proceeds are invested into money market instruments rather than investment grade bonds at rebalance; by the end of the expiration year, the index will have converted to an index of money market instruments and subsequently expire. In this way, one might refer to a fixed maturity index as having a maturity year (in this case, 2029), drawing a contrast to the typical construct of a fixed income index (which is perpetual in nature), as maturing proceeds are typically reinvested into the underlying securities and the original asset class exposure is constantly maintained.

Why is it interesting that a fixed income index “matures”?

The maturing nature of a fixed maturity index draws similarities to the profile of an individual bond, which has a maturity year where one may expect a return of principal. A scheduled maturity that is known in advance may be useful in financial planning where the timing of cash flow needs is certain. In the case of a fixed maturity index, one has certainty on a “maturity” year, but the exposure is not just one bond, it is an index of bonds. So, a fixed maturity index provides investors with a maturity date while still allowing diversification benefits of a broad-based fixed income benchmark. Fixed maturity indices are typically established with multiple maturity years, e.g. iBoxx USD Corporates Fixed Maturity Indices span the years 2027-2035.

How are fixed maturity indices utilized? What is a bond ladder?

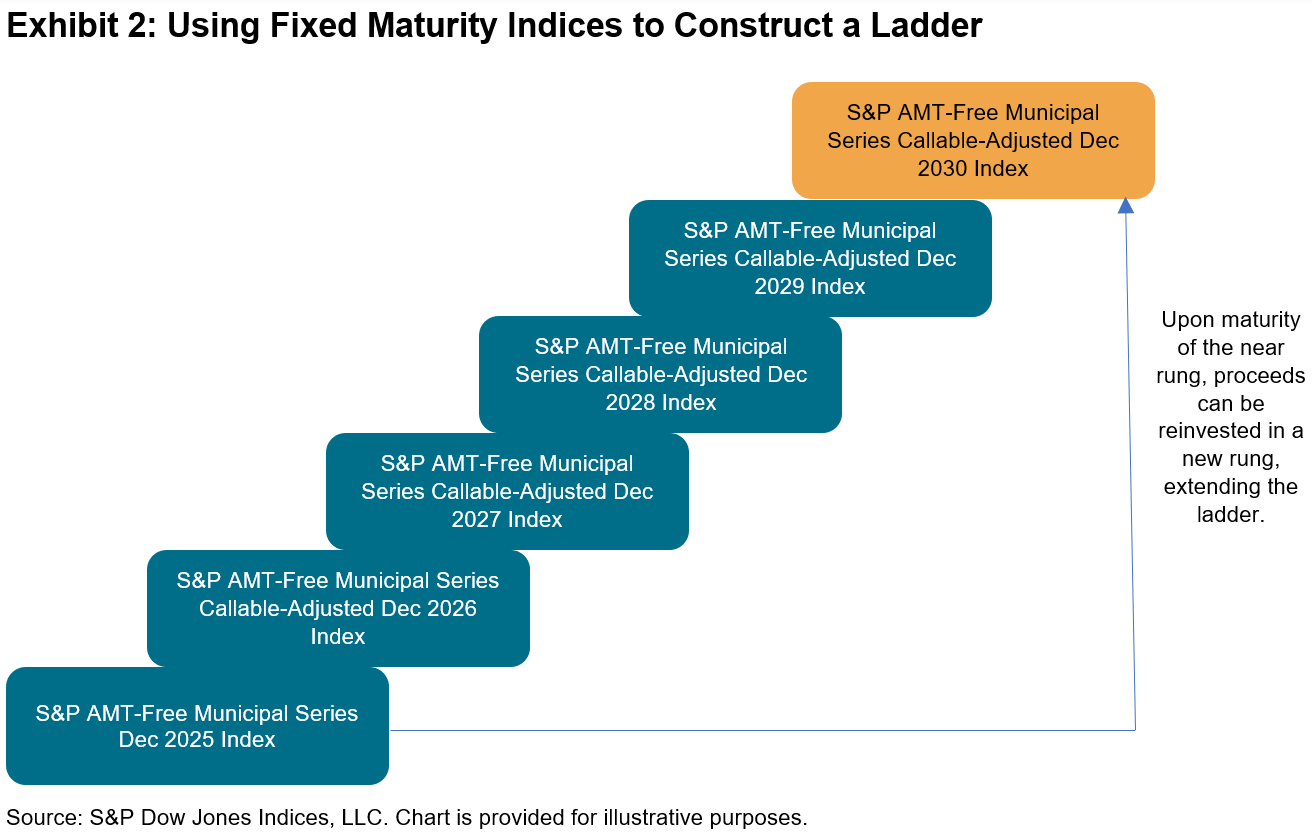

Bond laddering is a commonly used framework that has always existed in the investment community for individual bonds, and it now may utilize fixed maturity indices in a similar application. A bond ladder is constructed by choosing maturity years that match the needs of the investor. As a rung on the ladder matures, the proceeds may be extended to a further rung of the ladder. The resulting “ladder” of bonds is a construct that is meant to provide current income in the form of coupons while smoothing out interest rate fluctuations, as the staggered maturity dates track different yields.

Bond versus Bond Index

Bond ladder rungs were originally designed using single fixed income securities. By constructing a ladder using fixed maturity indices relative to individual securities, there could be potential diversification benefits and potentially minimized transaction costs as individual bonds may be difficult to access. This contrast has contributed to the growing popularity of fixed maturity indices and has resulted in index solutions being developed across all segments of fixed income, including investment grade credit, high yield credit, municipal bonds and sovereigns. For example, S&P DJI has carried a U.S. Municipal Bond Fixed Maturity Suite for over a decade and was one of the early adopters of this index construct as practitioners began utilizing indices to construct bond ladders. Our suite, the S&P AMT-Free Municipal Bond Index Series, first launched 15 years ago, includes indices with consecutive maturity years from 2024 to 2030. The recent expansion in Europe has spanned corporate credit and sovereigns, for all of which S&P DJI has index capabilities.

Conclusion

Conclusion