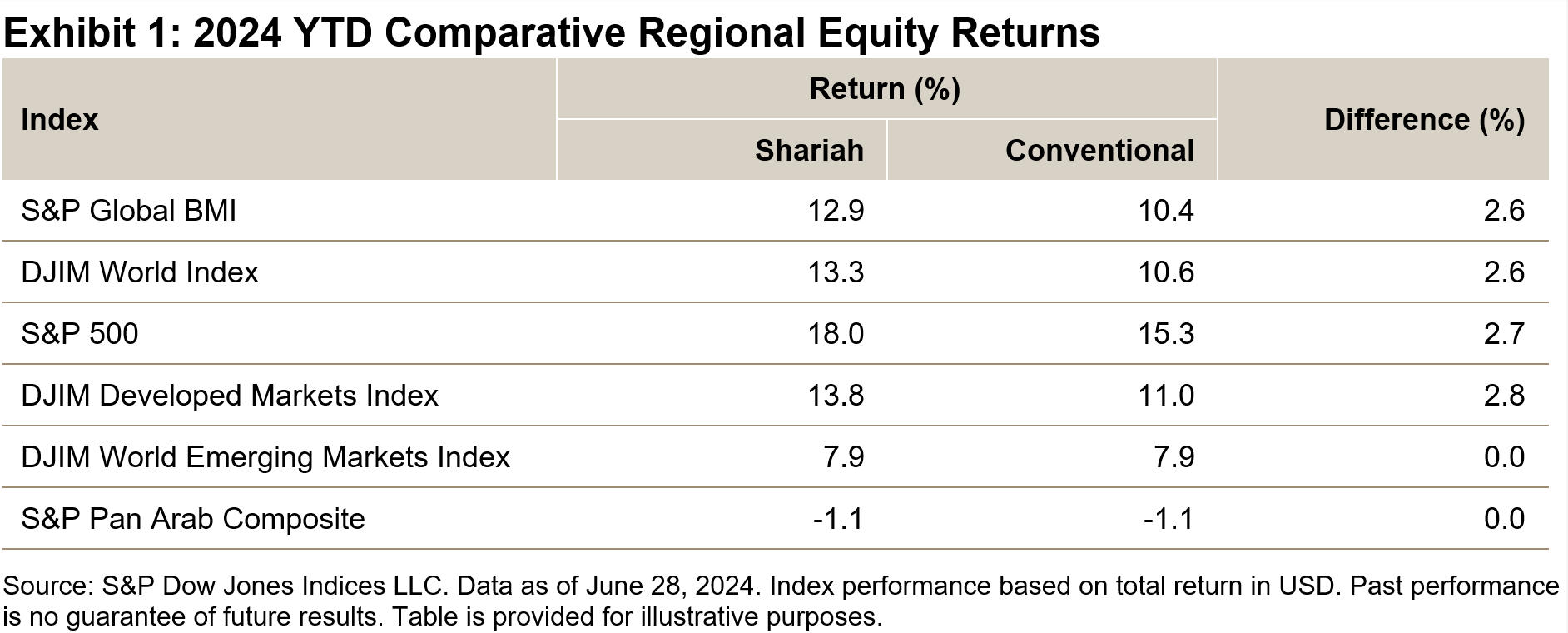

Global equities extended their upward trend into Q2 2024 on the back of sustained economic growth and moderating inflation. The S&P Global BMI posted a healthy 10.4% return in the first half of the year, led by the U.S where the S&P 500® had an impressive run with a 15.3% gain and new record highs. Shariah-compliant global benchmarks beat their conventional counterparts, with the S&P Global BMI Shariah and Dow Jones Islamic Market (DJIM) World Index both generating excess returns of 2.6% in H1 2024. Emerging markets started catching up with developed markets in the second quarter, narrowing their YTD return differentials to 3% in conventional benchmarks and 6% in Shariah-compliant benchmarks (see Exhibit 1).

MENA equities diverged from the global trend and remained sluggish. The S&P Pan Arab Composite posted a 1.1% loss in H1, led by Saudi Arabia (-1.5%), UAE (-3.5%) and Qatar (-2.4%). Egyptian equities stabilized after the loan extension by the International Monetary Fund, with the S&P Egypt BMI remaining almost flat in U.S. dollar terms in Q2.

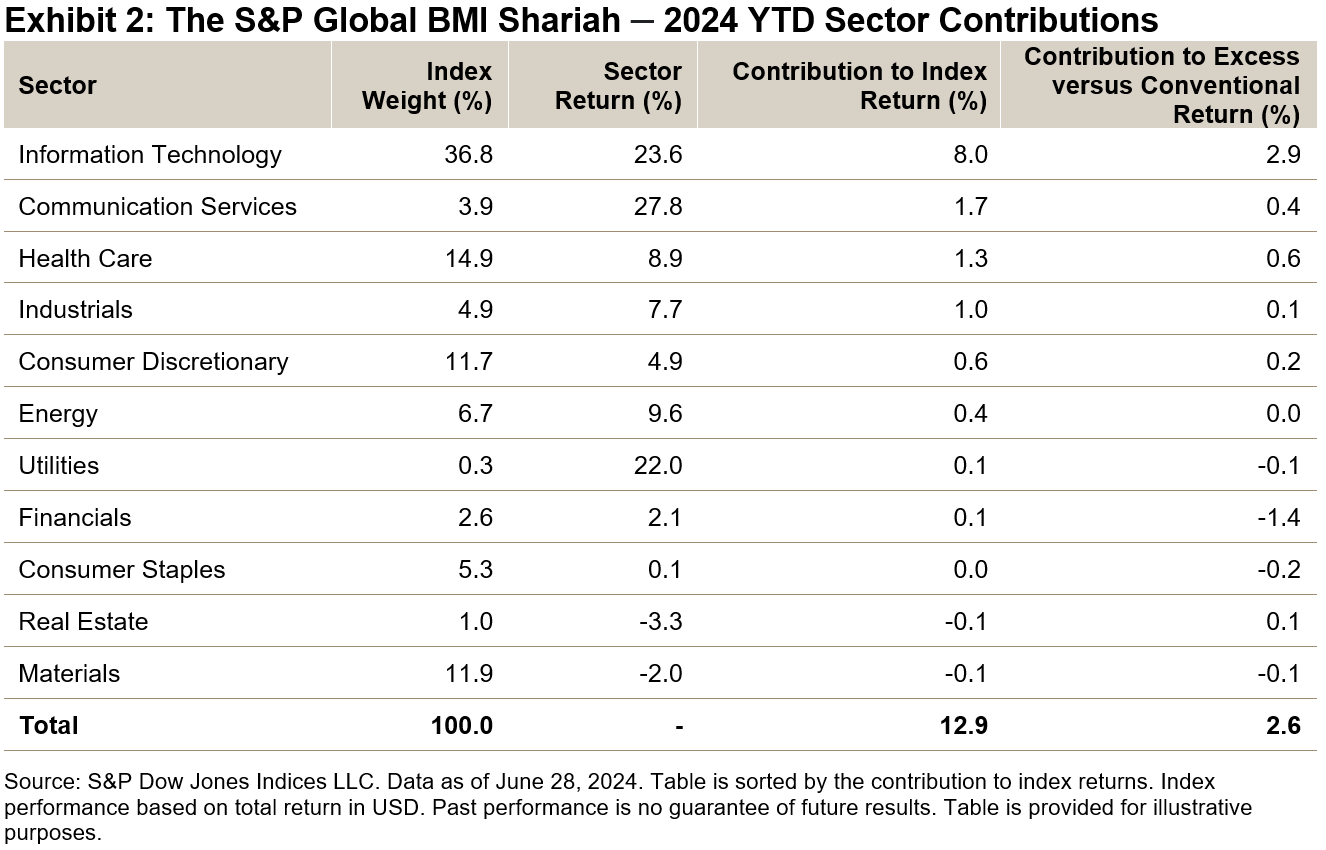

Drivers of Shariah Index Performance in H1 2024

The first six months of 2024 were characterized by the outperformance of large-cap Information Technology and Communication Services companies. Information Technology, which accounts for 36.8% in the S&P Global BMI Shariah versus 24.2% in the S&P Global BMI, contributed 62% of the Shariah index’s return and generated an excess return of 2.9% against the conventional benchmark. On the other hand, Financials brought the heaviest negative effect to the relative performance with an excess return of -1.4%, due to its reduced weightings (2.6% in the S&P Global BMI Shariah versus 15.7% in the S&P Global BMI) as well as the underperformance of Shariah-compliant Financials companies against non-compliant ones (see Exhibit 2).

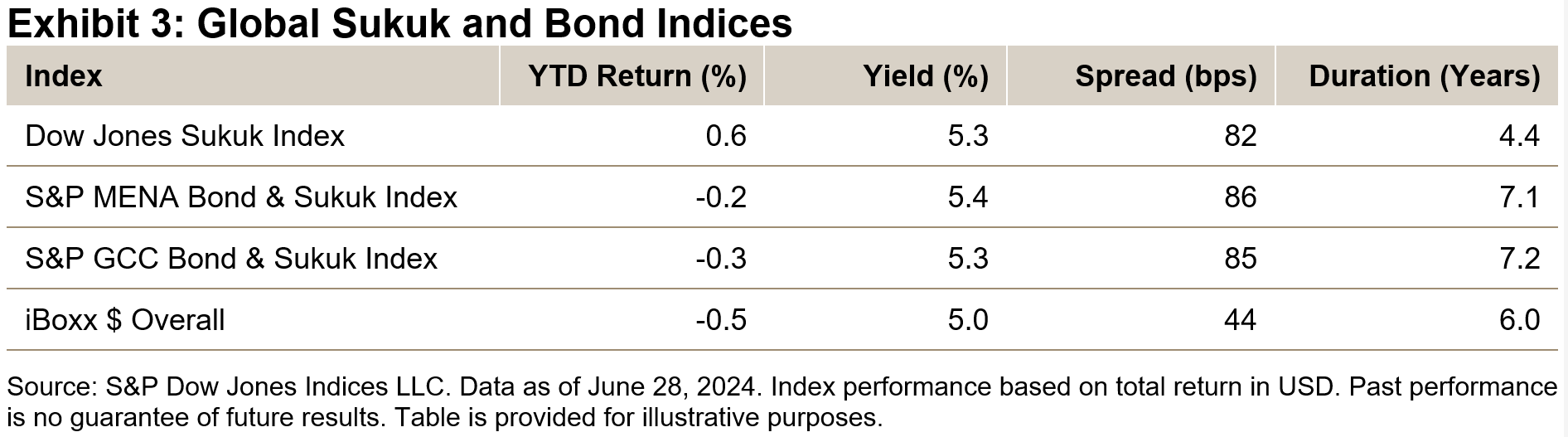

Global Sukuk Gained Modestly in H1 2024

With adjusted market expectations for the U.S. Fed to reduce interest rates in 2024, U.S. dollar-denominated investment-grade bonds remained under pressure globally, resulting in a 0.5% loss in the iBoxx USD Overall in H1. In comparison, the Dow Jones Sukuk Index, which comprises U.S. dollar-denominated investment-grade sukuk, gained 0.6%, largely due to relatively lower duration. The sukuk benchmark had a yield of 5.3% and a spread of 82 bps over the U.S. Treasury bonds as of the end of June 2024.

This article was first published in IFN Volume 21 Issue 29 dated July 17, 2024.

The posts on this blog are opinions, not advice. Please read our Disclaimers.