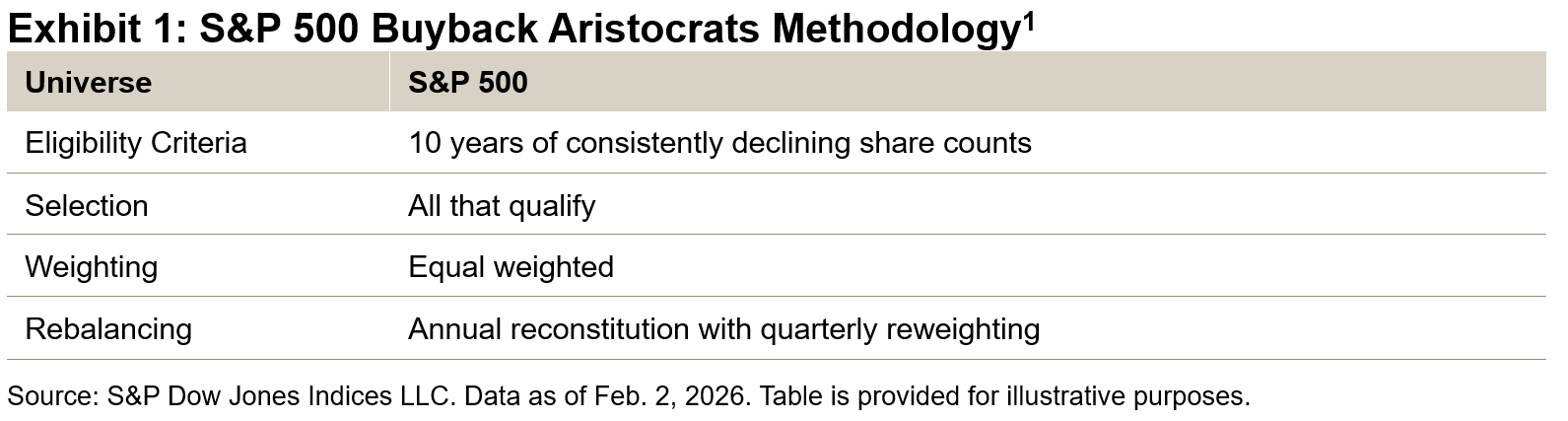

The latest addition to the S&P Aristocrats Index Series, the S&P 500® Buyback Aristocrats Index represents a new generation of buyback indices. This index tracks companies that have consistently reduced their common shares outstanding for at least 10 consecutive years—a rare achievement that signals disciplined capital management, financial strength and a steadfast commitment to shareholder interests.

Just as the S&P 500 Dividend Aristocrats® identifies companies with a proven history of growing dividend payments, the S&P 500 Buyback Aristocrats Index recognizes firms that demonstrate sustained dedication to share repurchases, with a particular emphasis on net share count reduction. This parallel underscores a core principle: quality is not defined by isolated actions, but by persistent behavior over time. By focusing on long-term buyback consistency, this index showcases companies focused on creating lasting value with a proven track record of enhancing shareholder returns.

A Differentiated Buyback Strategy

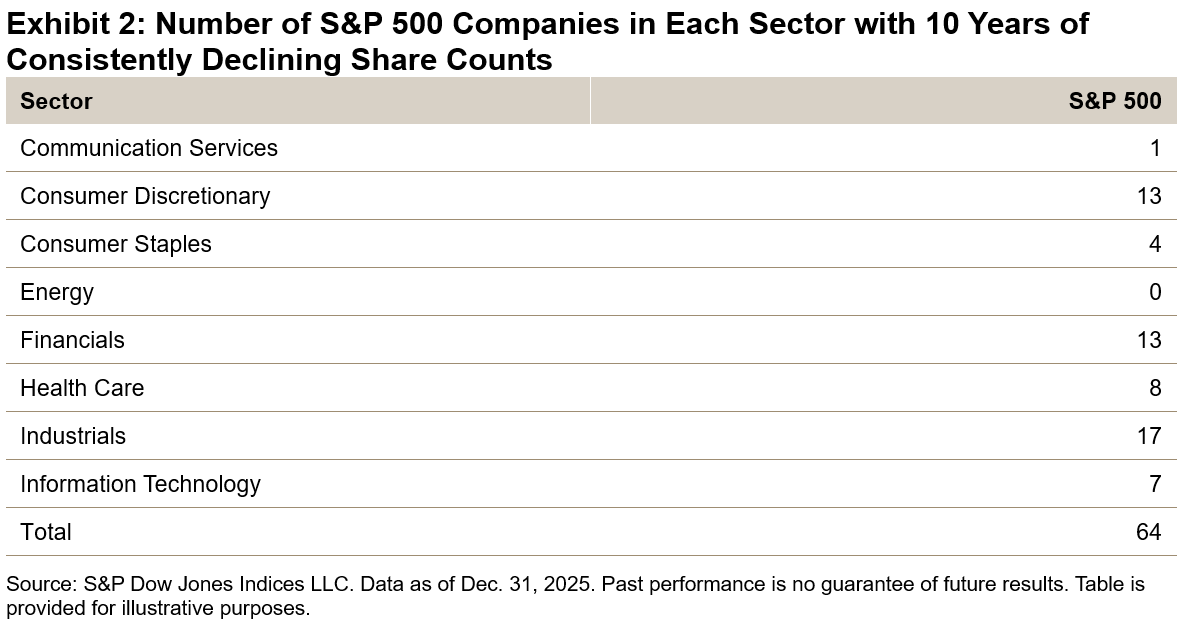

As of Dec. 31, 2025, the S&P 500 Buyback Aristocrats Index comprises 64 companies. Unlike traditional buyback strategies that rely on a single point-in-time assessment, this index emphasizes consistency across market cycles. This distinction is significant, as companies that regularly execute net buybacks tend to exhibit higher quality and more resilient earning power. Spreading buyback activity over multiple periods also helps address a common criticism of repurchases—that they are often poorly timed—thus resulting in a more balanced and reliable approach to capital return.

Long-Term Outperformance

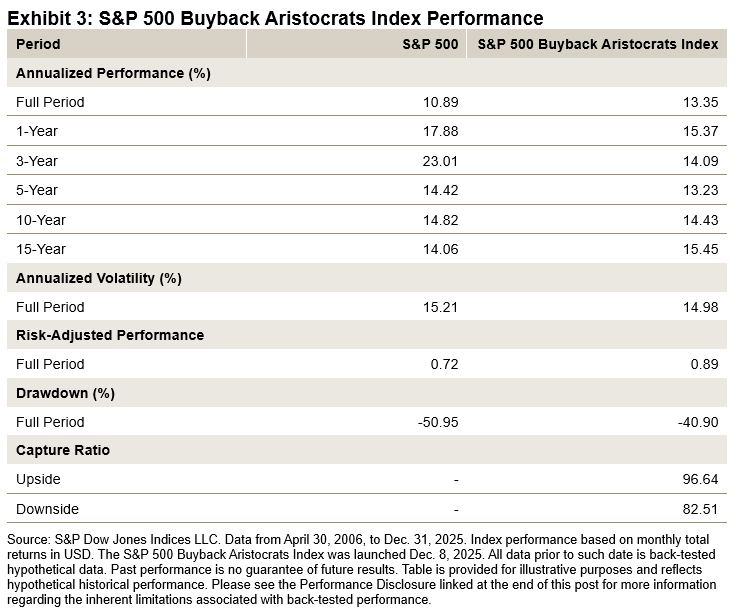

Back-tested data shows that the S&P 500 Buyback Aristocrats Index has outpaced the S&P 500 by 2.46% on an annualized basis since June 30, 2000. This long-term outperformance makes sense: as companies reduce their shares outstanding, each remaining share represents a larger claim on future earnings. Moreover, a sustained decrease in shares outstanding often signals a company’s ability to consistently generate strong cash flow and management’s ongoing commitment to returning capital to shareholders.

Defensiveness over the Business Cycle

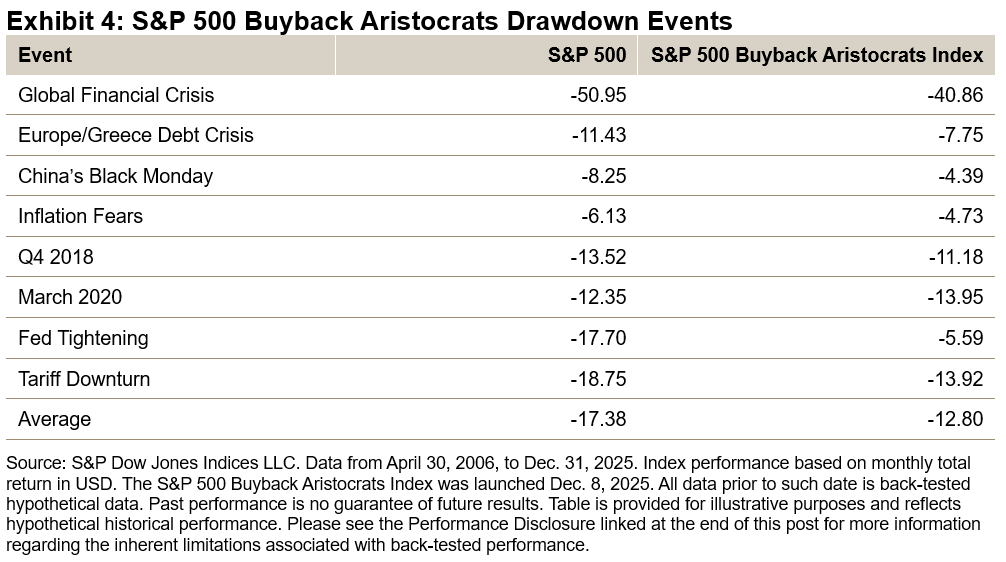

The defensive characteristics of the S&P 500 Buyback Aristocrats Index are particularly evident during periods of market stress. The index exhibited a lower downside capture than the S&P 500 and as shown in Exhibit 4, has demonstrated resilience during select drawdown events.

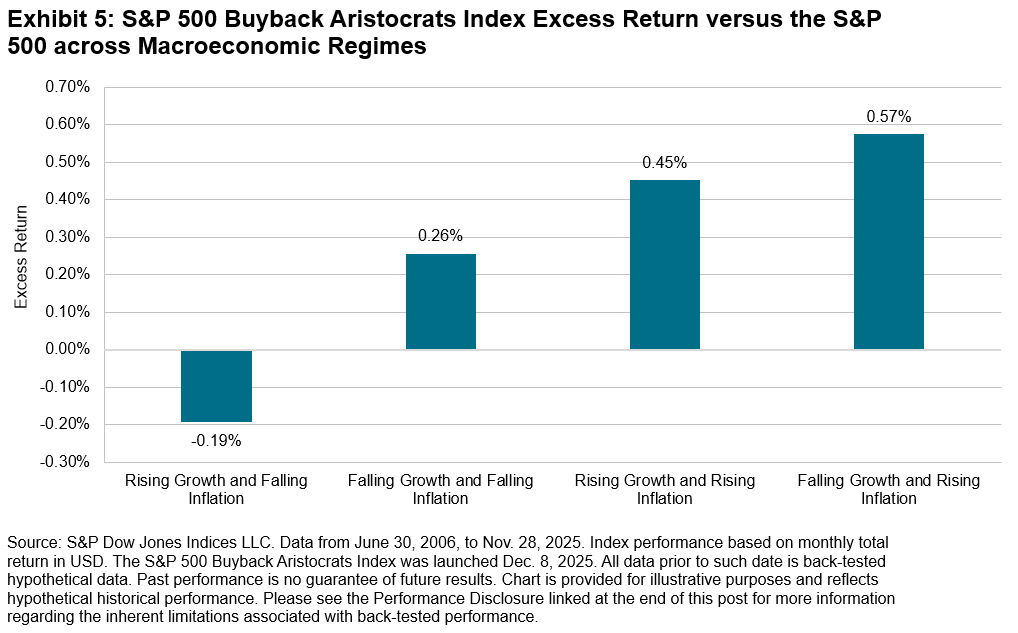

Like many factor-based strategies, performance relative to the benchmark may vary across macroeconomic regimes. Notably, across its back-tested history, the S&P 500 Buyback Aristocrats Index has outperformed during periods of rising inflation, as well as in environments characterized by slowing growth and declining inflation—conditions often associated with the later stages of the business cycle.

Conclusion

The S&P 500 Buyback Aristocrats Index stands out among buyback strategies by requiring constituents to demonstrate a reduction in shares outstanding for at least 10 consecutive years. This stringent requirement has historically driven outperformance and defensive qualities relative to its benchmark throughout its back-tested history.

1 For the full methodology, please refer to the S&P 500 Buyback Aristocrats Index Methodology.

The posts on this blog are opinions, not advice. Please read our Disclaimers.