The recent advent of artificial intelligence (AI) is transforming daily life from streamlining routine tasks to augmenting productivity and facilitating data-driven decisions. Within indexing, it is a natural progression to explore how these technologies can enhance index construction within a human-validated and governed framework. Integrating machine learning, a subset of AI, systematically enables the analysis of vast datasets, the identification of complex relationships and the generation of forward-looking insights. Applied in this way, AI offers an adaptive evolution of traditional factor investing, further reshaping the alpha-beta continuum.

In this blog, we will introduce the S&P 3AI Indices by reviewing the methodology, performance and positioning of this new index series.

3AI and the 3AI Alpha Scores

3AI is a London-based quantitative research technology firm specializing in machine learning and stock alpha forecasting. Founded in 2018, 3AI develops machine-learning-driven forecasting systems deployed in live investment and research environments.

Alpha forecasts are produced through a fully systematic process governed by strict temporal and methodological constraints, with human oversight focused on model validation, risk controls and research governance. The output of this process is the 3AI Alpha Score, representing a 12-month expected excess return forecast.

These 3AI Alpha Scores are produced through a network of interconnected AI systems operating across bottom-up and top-down dimensions, drawing on more than 300 structured data inputs. Bottom-up models analyze company-level fundamentals, factors, analyst expectations, market behavior and technical indicators, while top-down models reflect sectoral and business-cycle effects. S&P Dow Jones Indices has collaborated with 3AI to incorporate these 3AI Alpha Scores into its indices.

Methodology

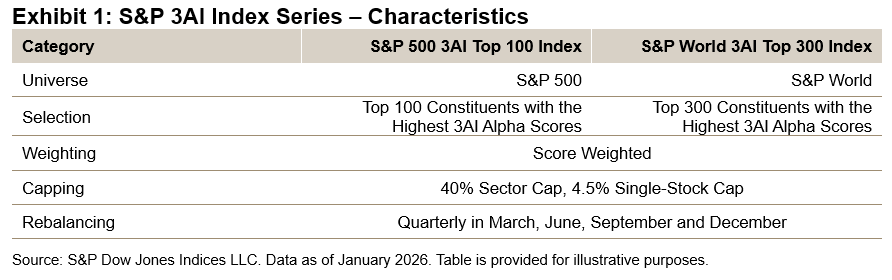

Two of the first indices launched using these scores are the S&P 500® 3AI Top 100 Index and S&P World 3AI Top 300 Index. Each index selects the highest-scoring companies in its universe, hence tracking those with the strongest 12-month alpha forecasts. Constituents are weighted proportionally to their 3AI Alpha Scores, and the indices are rebalanced quarterly. See the index methodology for more details.

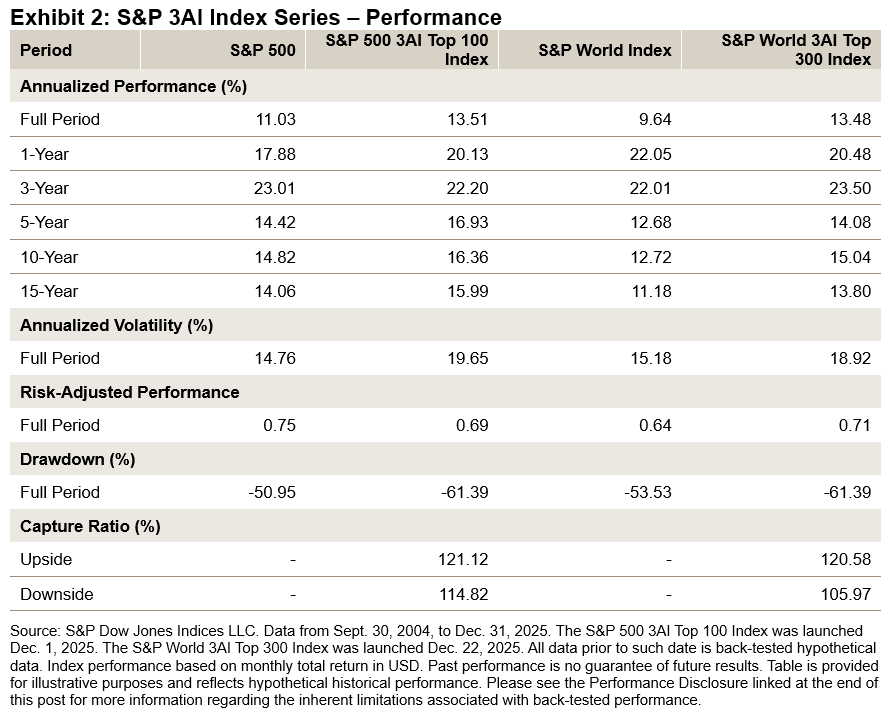

Performance Characteristics

Since the index was launched in late 2025, any performance data prior to that date is considered back-tested. It is important to note that the development of a machine-learning forecasting process involves three distinct phases: model training, out-of-sample testing and, lastly, live implementation. During model training, only point-in-time data is utilized, ensuring that observed alpha is genuinely out-of-sample or live and is not influenced by the realized performance of the index or any related strategy. Once live, the model benefits from an expanding data and learning window.

Over the back-tested period studied from Sept. 30, 2004, to Dec. 31, 2025, the S&P 500 3AI Top 100 Index achieved approximately 2.5% annualized outperformance versus the S&P 500, while the S&P World 3AI Top 300 Index outperformed the S&P World Index by about 3.8% annualized.

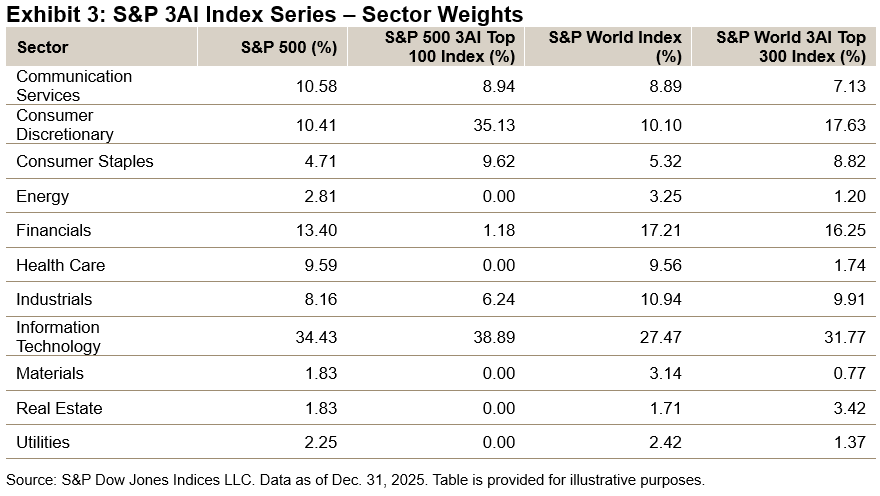

Sector Weights

As of Dec. 31, 2025, both indices exhibited notable overweights in Consumer Discretionary—approximately 25% above the benchmark for the S&P 500 3AI Top 100 Index—and in Consumer Staples, which was nearly double its benchmark weight. For both indices, Information Technology also showed an overweight relative to their benchmarks. In Financials, the S&P 500 3AI Top 100 Index was materially underweight, but the S&P World 3AI Top 300 Index was broadly in-line with its benchmark. This highlights a two-sided dynamic within the sector: U.S. Financials were de-emphasized, while Financials companies from other developed markets were overweighted. Health Care had a significant underweight in both indices, having been largely excluded.

Conclusion

The S&P 3AI Indices represent our first AI-enhanced indices that use predictive modeling to drive stock selection. While the underlying scores are derived from machine-learning models, the indices bring the benefits of transparency and robust human-led governance. We are excited to introduce these innovative benchmarks and are exploring the expansion of this series of indices. Stay tuned for further analysis and publications that will provide additional information on the machine-learning processes and offer detailed attribution of historical index performance.

The use of “3AI” in the name of the S&P 3AI indices is a reference to the machine learning technology firm, 3AI, which provides the 3AI Alpha Intelligence scores that are used by S&P Dow Jones Indices in the construction of these indices. These scores represent 12-month excess return forecasts, generated through the application of machine learning techniques across global equities, by analyzing company data and business-cycle sensitivities.

The Content may have been created with the assistance of an artificial intelligence (AI) tool. While the AI tool may provide suggestions and insights, the final Content was composed, reviewed, edited, and approved by a human(s) at S&P Dow Jones Indices. As such, S&P DJI claims full copyright ownership of this AI-assisted Content, in accordance with applicable laws and regulations.

The posts on this blog are opinions, not advice. Please read our Disclaimers.