Looking back at 2025, some key themes emerged and drove many market conversations. Many different themes—including the rise of artificial intelligence (AI), tariffs, risk of inflation and a focus on defense—set against a backdrop of broader macroeconomic, geopolitical and technological changes created a period of increased market uncertainty across industries. Volatility, as measured by VIX®, remained high for most of the year,1 reflecting ongoing investor concern. The S&P 500® experienced notable swings in 2025, approaching bear-market levels in April amid concerns over tariffs before rallying to record highs by June as enthusiasm for AI fueled the market.

But volatility was not the entire story. High readings for both VIX and the Cboe S&P 500 Dispersion Index (DSPX) emphasized that broad macroeconomic trends influenced market direction in 2025 and resulted in a wide variation in performance across industries.

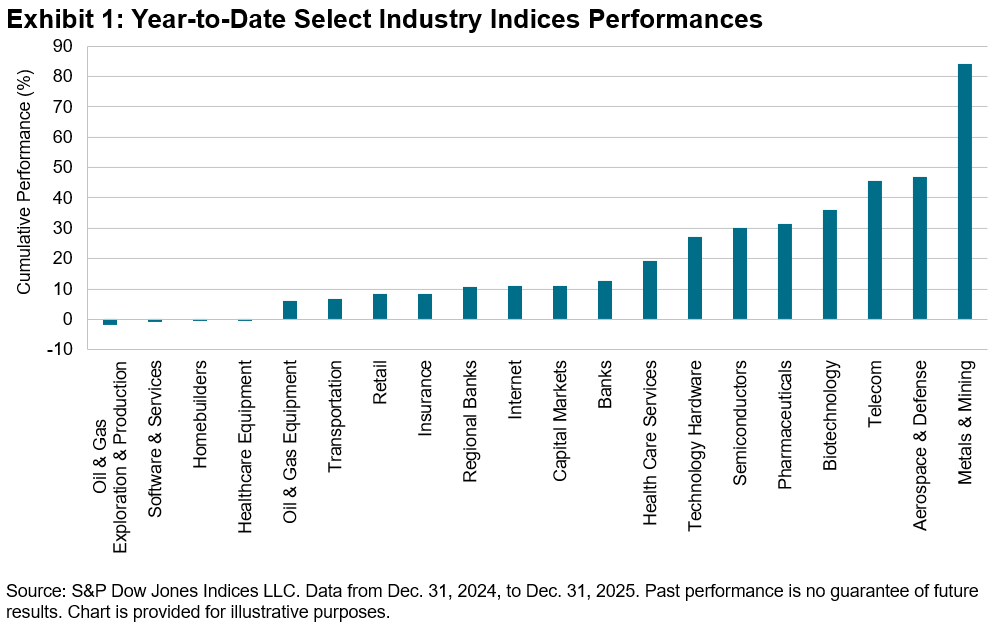

So, who were the leaders and laggards across the U.S. equity landscape in 2025? In a year when headlines focused on big themes, the S&P Select Industry Indices offered a valuable way to look beyond the broad market and highlight the key factors driving this year’s most significant moves, as shown in Exhibit 1.

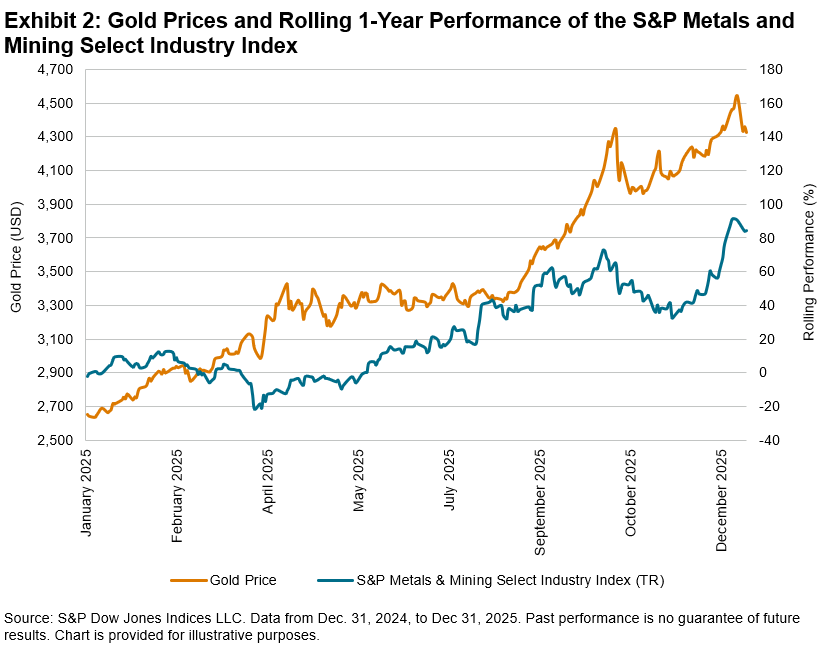

To start, the Metals & Mining industry had a golden year, experiencing an 84.2% increase in 2025. Rare earth elements drive the modern world, with technological advancements boosting demand across various sectors, from AI to defense. Amid rising geopolitical tensions, the U.S. government took measures to bolster domestic supply chains for strategic metals, further supporting the industry’s strong performance. To top it off, gold prices hit record highs in October, as shown in Exhibit 2, fueled by safe-haven demand amid ongoing geopolitical concerns, economic uncertainty and a weaker U.S. dollar.

Aerospace & Defense ranked as the second-highest growth sector among the S&P Select Industries, posting a significant 46.8% increase, largely driven by rising geopolitical tensions worldwide.

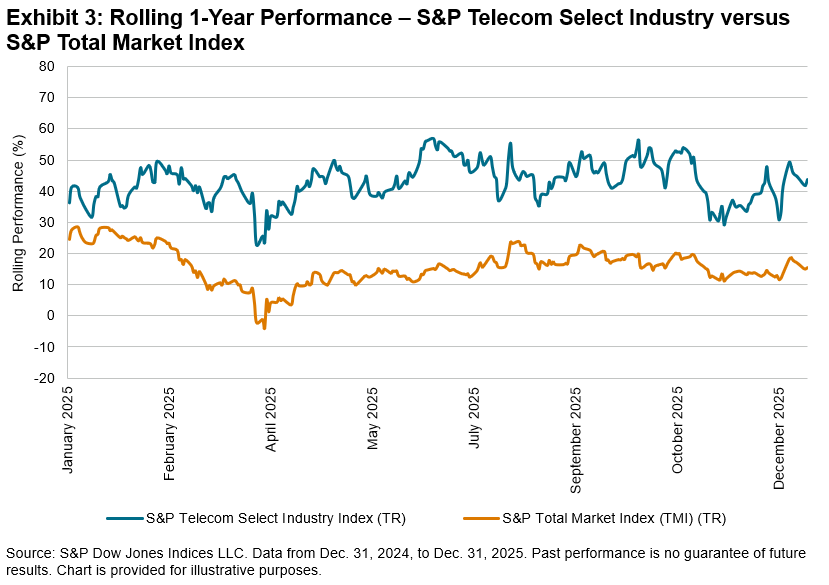

AI-related industries, including Semiconductors and Technology Hardware, also ranked among the top performers in 2025, increasing by 30.1% and 27.3%, respectively. Telecom, another industry closely tied to AI, also delivered strong results, with a 45.5% gain, outperforming the S&P Total Market Index as shown in Exhibit 3.

This standout performance in Telecom was fueled by strategic mergers, ongoing technological advancements and increasing demand for digital infrastructure.2 Defense-linked telecom companies contributed significantly as well. Ondas Holdings, for example, achieved an extraordinary YTD total increase of 1,022.0%,3 based on market optimism about its military and security technologies.

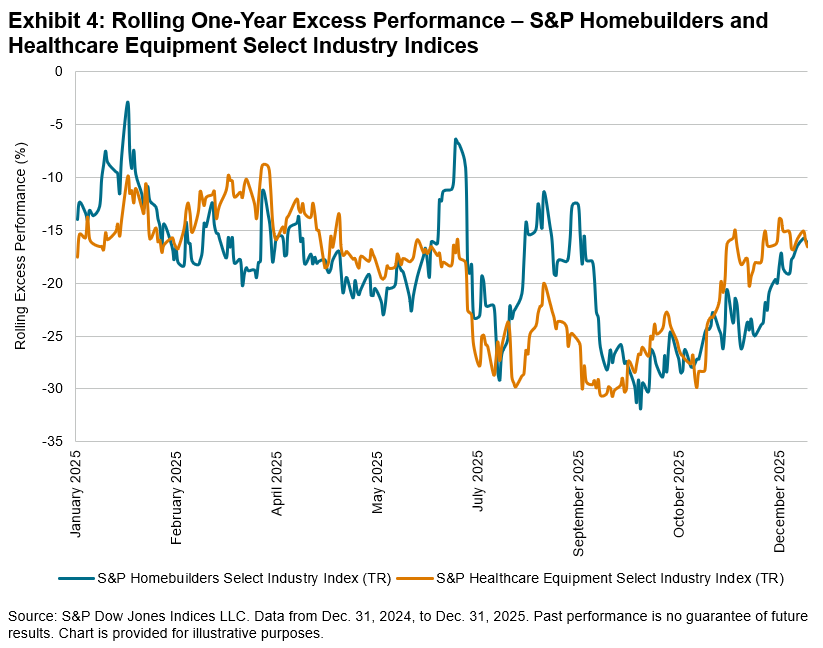

While some industries thrived, others that were more influenced by macroeconomic and political shifts and less influenced by technological trends faced significant challenges. Industries sensitive to tariffs, such as Homebuilders and Healthcare Equipment, struggled, as illustrated in Exhibit 4.

Homebuilders faced a difficult 2025, dropping 0.4% YTD. The industry struggled with declining new home sales, primarily due to affordability issues, higher construction material costs and persistently high interest rates. Looking ahead, tariffs on steel and aluminum are expected to further slow the construction market, possibly leading to more project delays and cancellations into 2026.4

Healthcare Equipment faced similar headwinds, dropping 0.3% YTD. Tariffs on medical devices and products weighed on suppliers, distributors and hospitals, further dampening overall industry sentiment.5

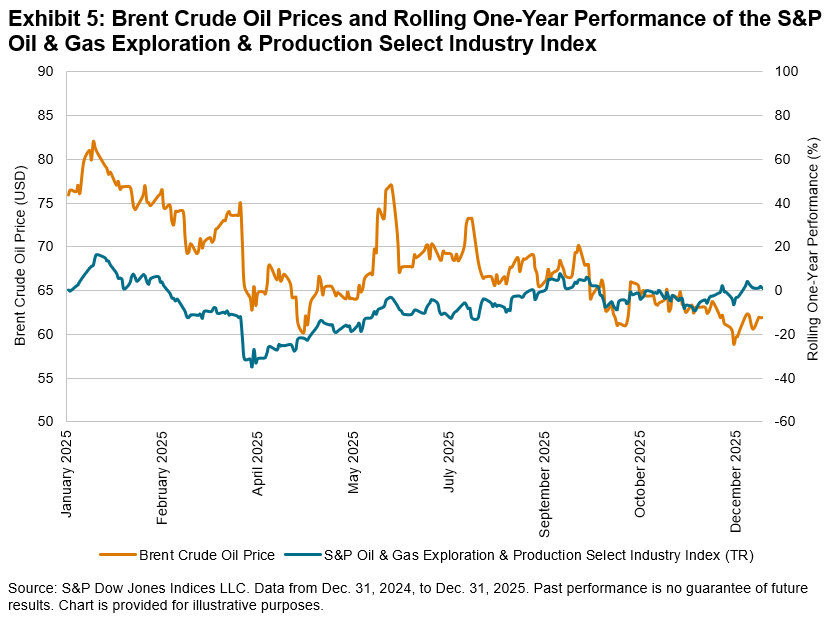

To close out the 2025 Wrapped, Oil & Gas Exploration & Production was the biggest decliner, falling 1.9% for the year. In 2025, crude oil prices overall declined as global supply exceeded demand, reflecting mainly negative performances for the industry, as shown in Exhibit 5.

In 2025, the market moved unevenly; some industries surged while others struggled, shaped by macro forces. The S&P Select Industry Indices offered valuable insights into these shifting trends, highlighting both leaders and laggards across the volatile and dispersed U.S. equity landscape. As market dynamics continue to evolve, with ongoing concerns about a potential AI bubble,6 lingering uncertainty over tariffs and rapidly changing geopolitics in the region, staying attuned to industry-level developments could prove crucial in helping understand the key drivers of the market and the economy in 2026.

1 Vörös, Benedek. “Rallies, Records and Relentless Restlessness: A Tale of Markets in 2025.” S&P Dow Jones Indices. Dec. 16, 2025.

2 S&P Global Ratings. “U.S. Telecom And Cable 2025 Outlook: Convergence, Consolidation, And Disruption.” Jan. 13, 2025.

3 Data as of Dec. 9, 2025.

4 S&P Market Intelligence. “US tariffs: Impact on the US construction industry.” July 21, 2025.

5 S&P Ratings. “The Health Care Credit Beat: Medical Devices And Supplies Tariff Impact Muted–For Now.” Oct. 22, 2025.

6 Ganti, Anu. “Animal Spirits or Anxiety?” S&P Dow Jones Indices. Nov. 13, 2025.

The posts on this blog are opinions, not advice. Please read our Disclaimers.