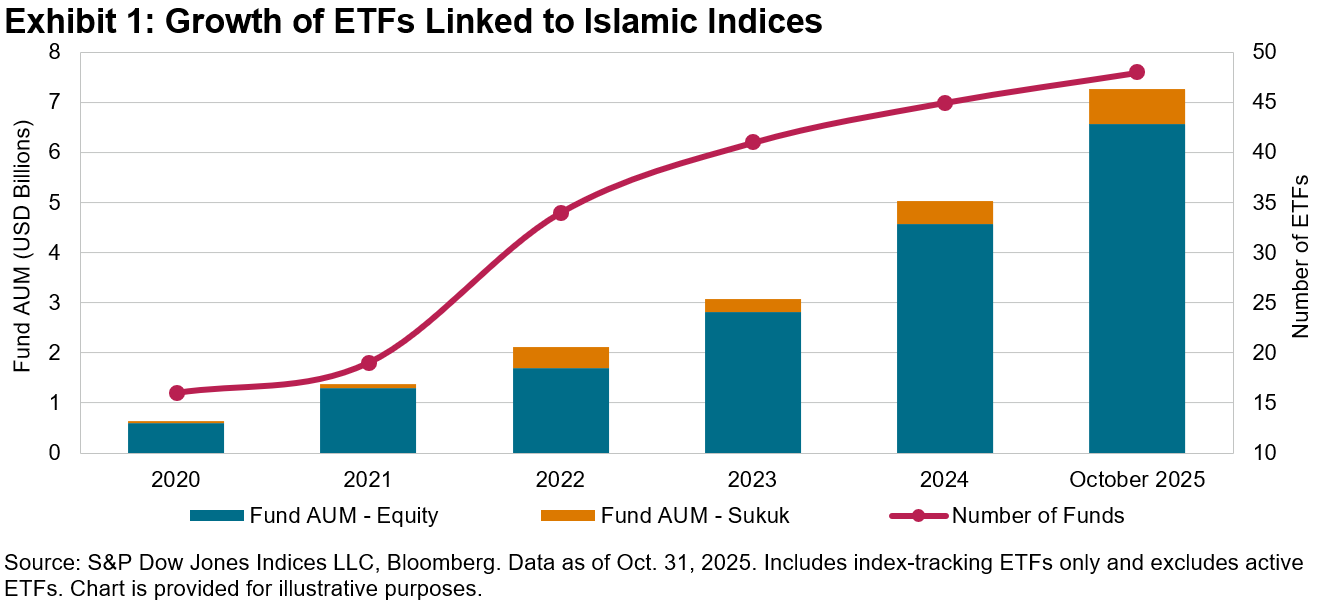

The Islamic asset management industry has been experiencing growth in index-based investing, and these trends have accelerated in 2025. As of October 2025, assets under management (AUM) in exchange-traded funds (ETFs) linked to Islamic indices reached USD 7.3 billion, a 44% YTD increase (see Exhibit 1)—outpacing the 30% growth observed in the global ETF market.1

While Islamic ETFs are traditionally more associated with equities, sukuk is becoming a significant segment, now comprising 9% of total AUM following two new ETF listings this year. Beyond sukuk, there is an expanding range of offerings that include sector, factor, sustainability, active and option-based strategies, offering innovative options for diversification and participation in the various components of the Islamic finance universe.

Performance of Global Islamic Equity and Sukuk Indices

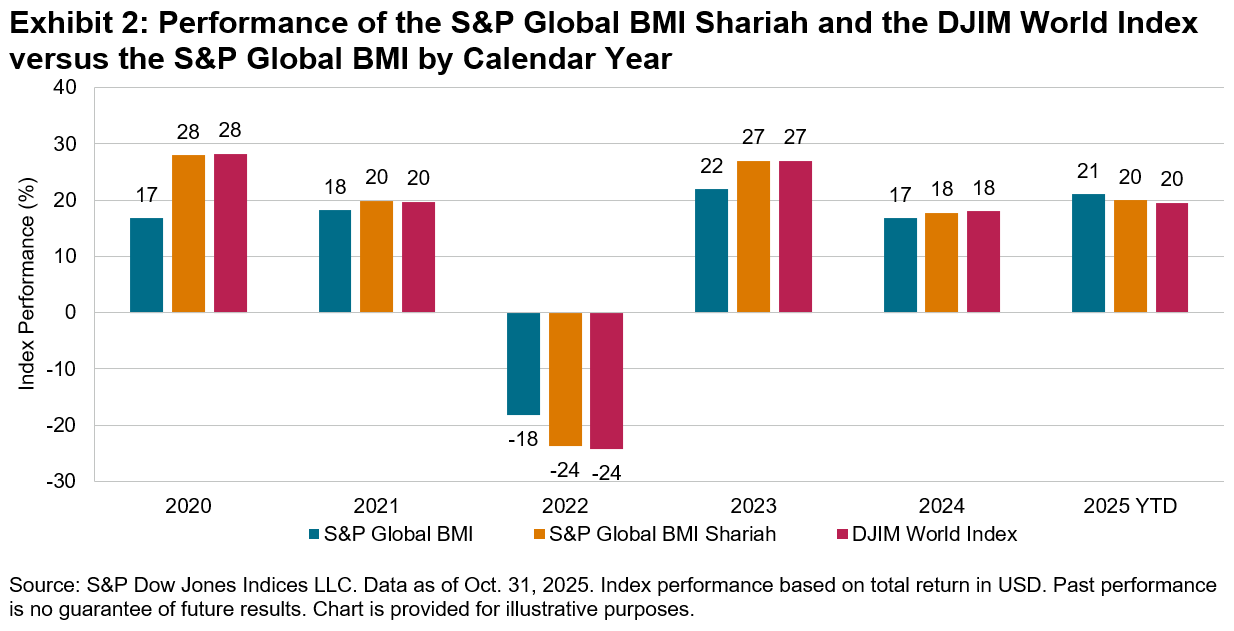

Global equities have demonstrated strong performance this year, bolstered by global monetary easing and AI-driven enthusiasm. By the end of October 2025, the S&P Global BMI stood with a 21.0% increase YTD.2 However, Shariah-compliant global equities slightly underperformed their conventional counterparts overall, with the S&P Global BMI Shariah and Dow Jones Islamic Market (DJIM) World Index recording gains of 20.0% and 19.5%, respectively. If this trend continues, it will mark the first instance of annual underperformance for our global Islamic equity indices since 2022 (see Exhibit 2).

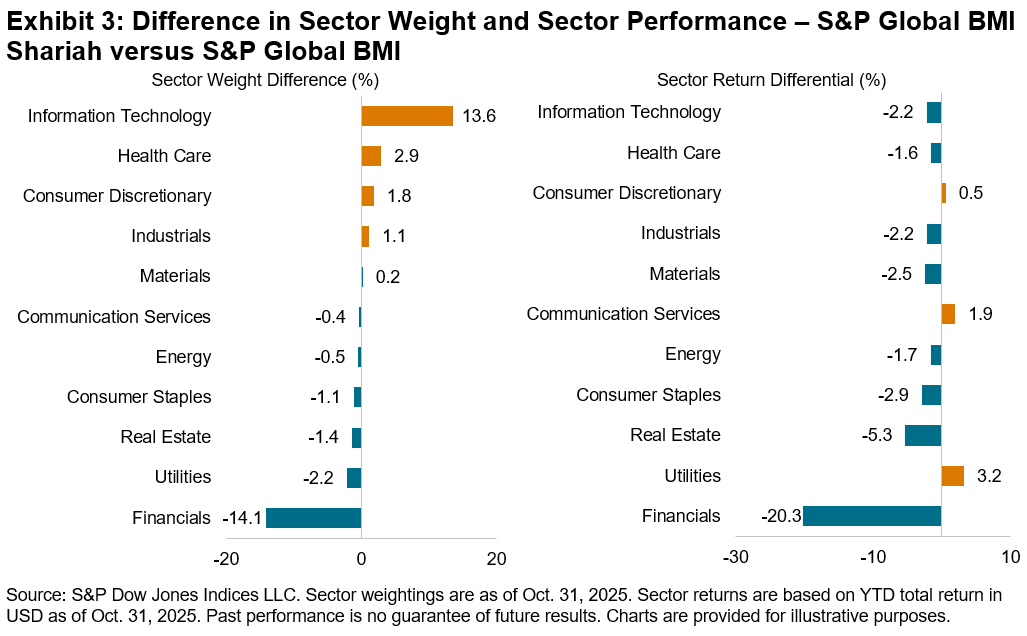

The relative performance of Islamic indices can be effectively analyzed through the lens of sectors. As of Oct. 31, 2025, Information Technology accounted for 40.4% of the S&P Global BMI Shariah, compared to 26.8% in the S&P Global BMI. This sector was instrumental in driving the Shariah index’s performance, contributing to 54.5% of the total return and posting an excess return of 3.1% relative to the conventional benchmark YTD. Conversely, Financials had a negative impact, resulting in an excess return of -3.5%. This is partly due to its lower weight: only 2.5% in the S&P Global BMI Shariah versus 16.5% in the S&P Global BMI. However, Shariah-compliant Financials companies also underperformed their non-compliant counterparts significantly: the S&P Global BMI Shariah Financials sector underperformed the S&P Global BMI Financials sector by 20.3% (see Exhibit 3).

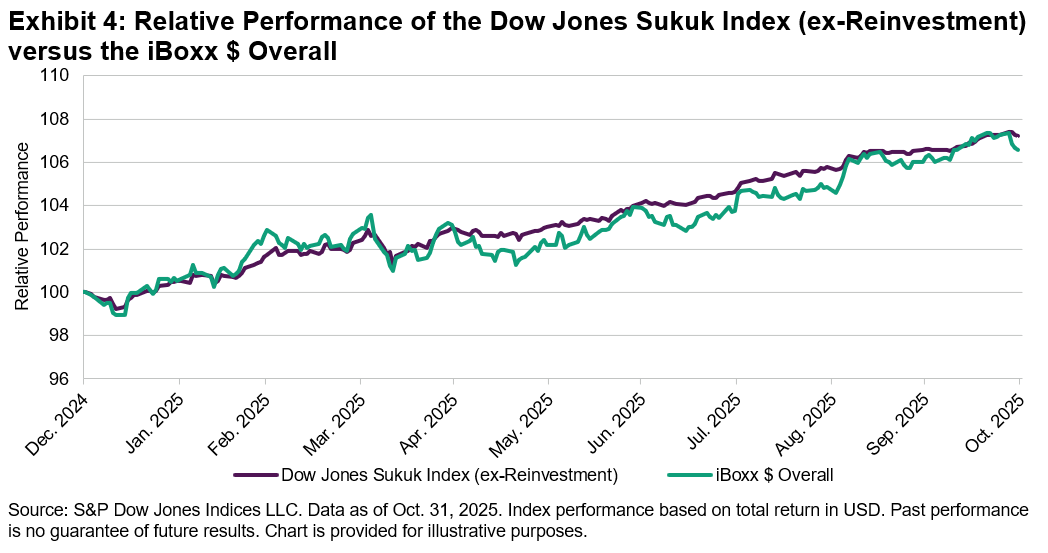

Global bonds also performed well, aided by easing inflation and declining interest rates. As of the end of October 2025, USD-denominated investment grade bonds, as represented by the iBoxx $ Overall, gained 6.6% YTD. In comparison, the Dow Jones Sukuk Index (ex-Reinvestment), which tracks USD-denominated investment grade sukuk, outperformed at 7.2% YTD, driven in part by compression in credit spreads.

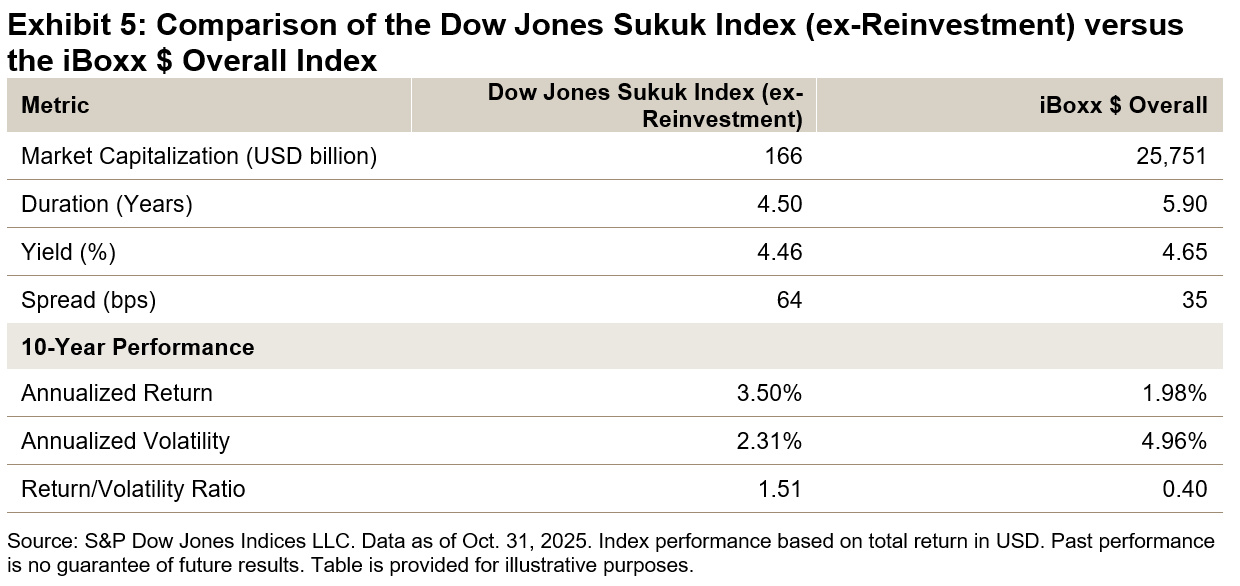

The Dow Jones Sukuk Index (ex-Reinvestment) displayed lower volatility in comparison to conventional bonds. Despite a wider credit spread, it outperformed with less volatility than the iBoxx $ Overall, resulting in higher risk-adjusted performance over the past decade (see Exhibit 5). This can be attributed to sukuk’s relatively shorter duration, but it may also reflect the nature of its investor base: the majority of sukuk investors are long-term, buy-and-hold Islamic institutions, including Islamic banks, insurers and pension funds, which often have regulatory or Shariah compliance requirements to hold sukuk. A relative absence of speculative trading may contribute to lower observed volatility.

Looking Ahead

The global sukuk market continues to expand; it surpassed the USD 1 trillion mark in outstanding issuance this year.3 The USD-denominated sukuk sector has gained prominence due to increasing financing needs of core Islamic finance countries and the growing interest of non-Islamic sovereigns in sukuk as a financing option. The historical performance and risk profile of USD-denominated sukuk also underscores its potential for wider adoption among non-Islamic fixed income market participants. However, the situation regarding Shariah Standard 62 of the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) remains uncertain, with amendments and delays in implementation that warrant close monitoring.4

Currently, most ETFs tracking Islamic indices are within products domiciled in North America and Europe, largely due to the more developed ETF markets in these regions. While this trend may persist and drive the majority of growth in the sector in the foreseeable future, other regions are also beginning to embrace index-based investing. The relevance of index-based investing to MENA-based investors is supported by a growing library of empirical evidence: the recent S&P Indices Versus Active (SPIVA®) Scorecard shows that actively managed MENA and GCC equity funds largely underperformed their relevant benchmarks.5

Amid these developments, indices could continue to play a role as benchmarks for Shariah-compliant investments and as the basis for innovative, transparent solutions to meet the evolving needs within the Islamic finance sector. As the market matures, the integration of index-based strategies changes the landscape for Islamic finance participants and fosters greater accessibility for a diverse range of investors. This evolution may support sustainable growth and help ensure that the Islamic finance sector remains adaptive in a rapidly changing global landscape.

This article was first published in IFN Annual Guide 2026.

1 Source: ETFGI. Data as of Oct. 31, 2025.

2 All returns mentioned in this post are total returns in USD.

3 Tan, Jessica. “Sukuk Market Hits USD 1 Trillion This Summer: What You Should Know.” S&P Dow Jones Indices. Sept. 2, 2025.

4 “Sukuk Issuance Trends Show Resilience.” S&P Global Ratings. July 8, 2025.

5 Ganti, Anu R. et al. “SPIVA® MENA Mid-Year 2025.” S&P Dow Jones Indices. Oct. 28 2025.

The posts on this blog are opinions, not advice. Please read our Disclaimers.