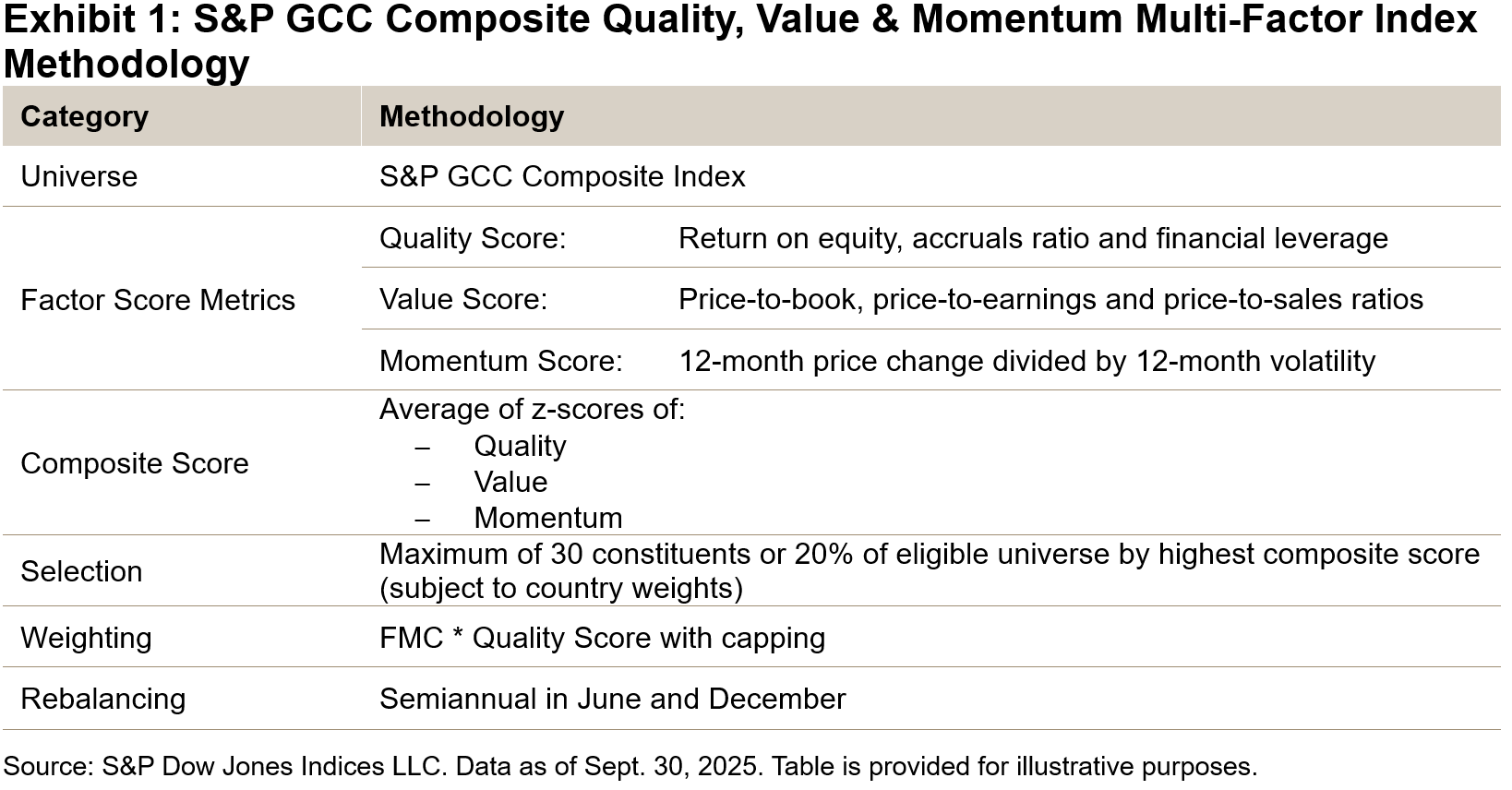

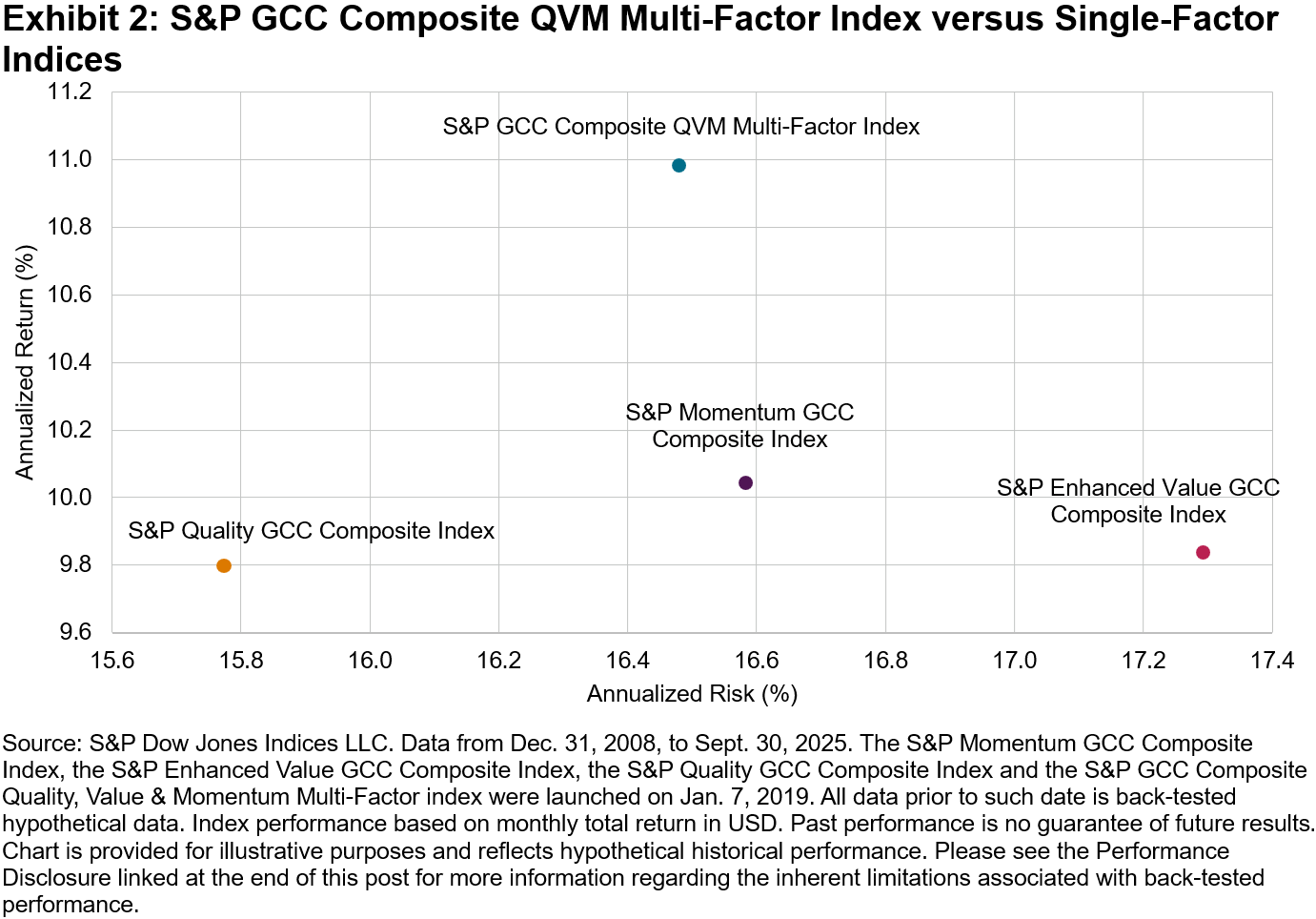

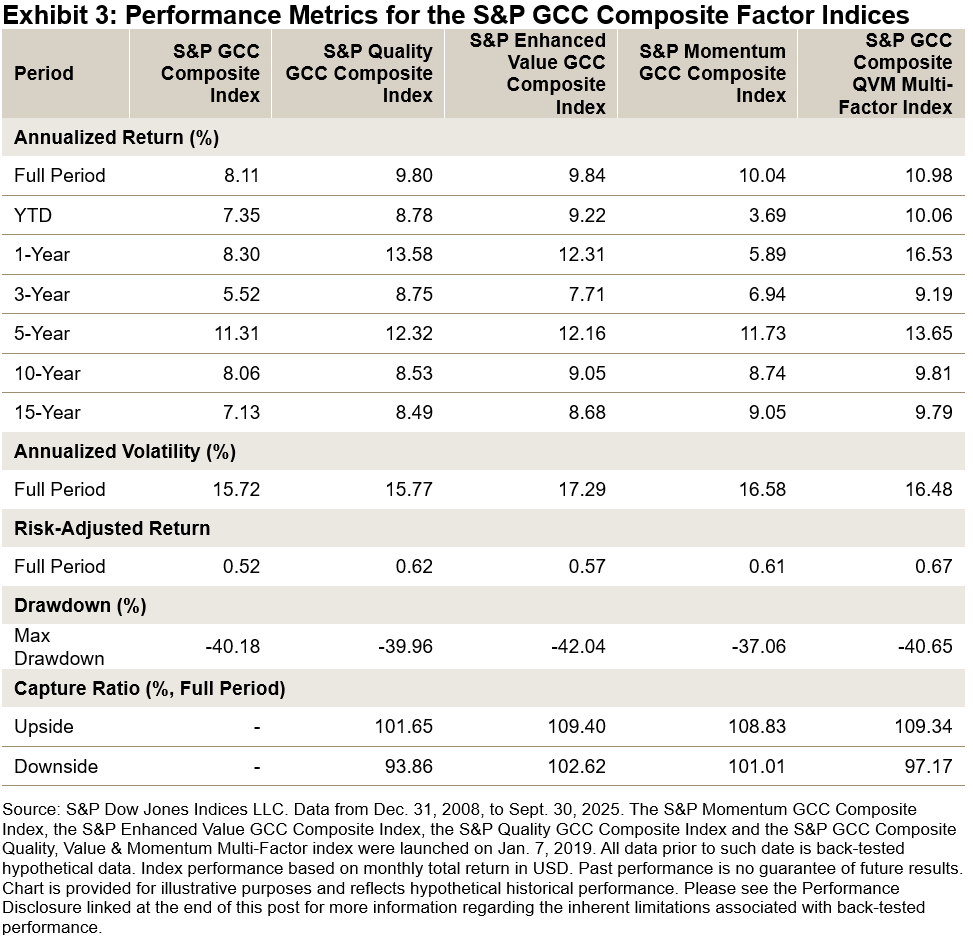

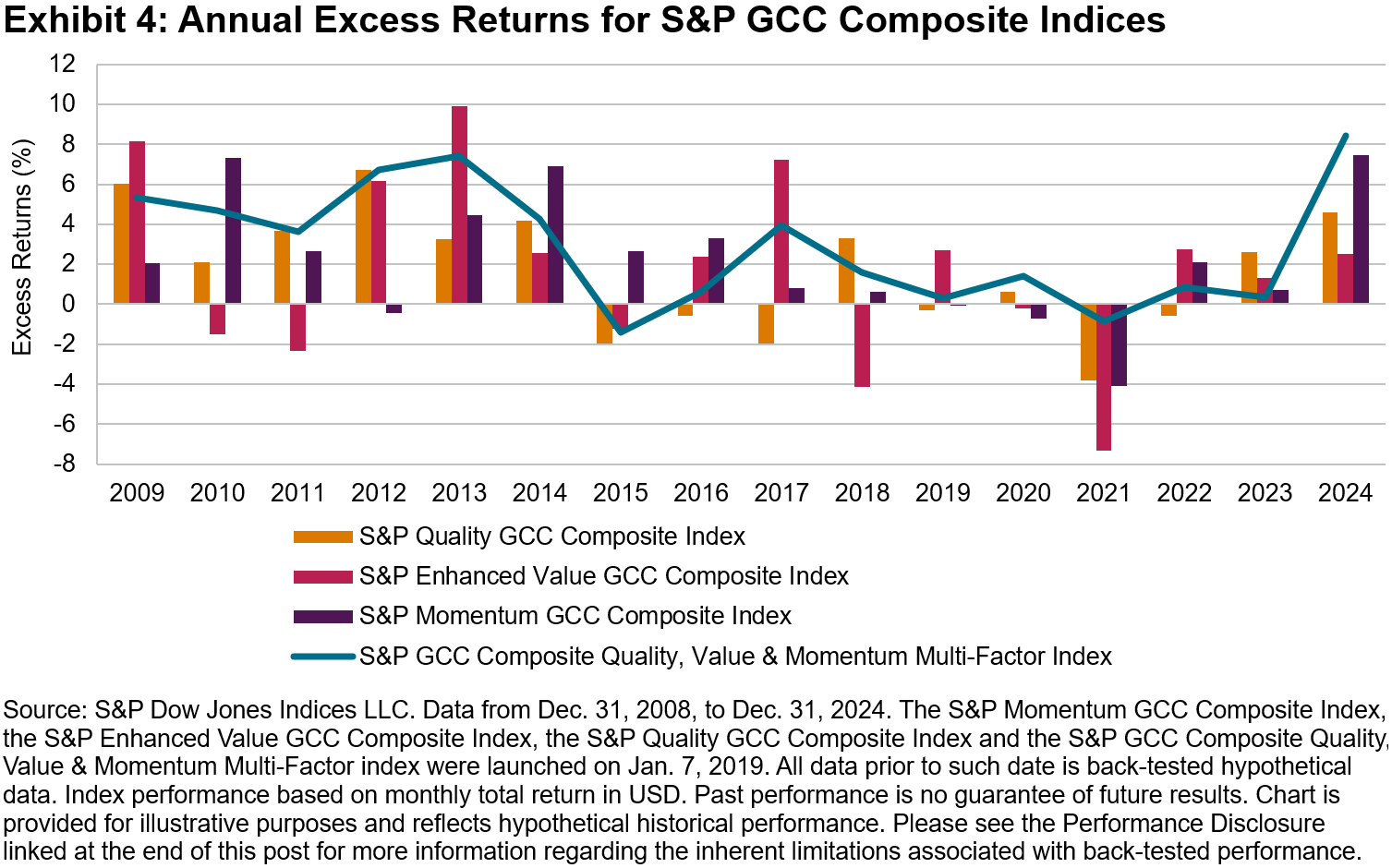

Direct indexing separately managed accounts (SMAs) are gaining traction, especially among financial advisors serving affluent and high-net-worth clients. In their recent whitepaper, Cerulli Associates projects a five-year compound annual growth rate (CAGR) of 16% for direct indexing SMA assets—the highest among all investment vehicles considered.1 In this blog, we unpack what is driving the growth of direct indexing SMAs and examine how advisors who use these solutions evaluate SMAs and their underlying indices.

Why Advisors Utilize Direct Indexing SMAs

Direct indexing SMAs are investment vehicles designed to allow users to track customized versions of well-known indices by owning the securities directly. This direct ownership creates opportunities for tax-loss harvesting, tilting for particular themes and accommodating specific client needs in other ways.

The wide range of potential applications of direct indexing SMAs may help advisors better serve their affluent and high-net-worth clients. Direct indexing SMAs traditionally require higher investment minimums compared to other investment vehicles but enable more optionality than mutual funds or ETFs.

What Matters Most to Advisors Considering Direct Indexing SMAs

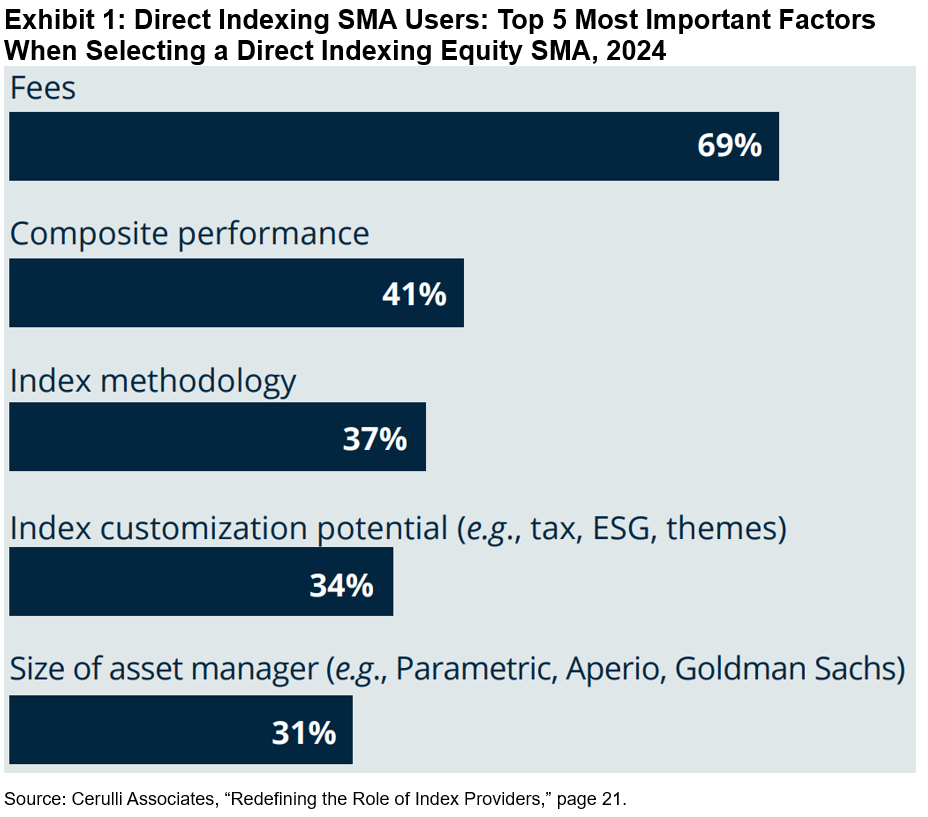

When selecting a direct indexing equity SMA, financial advisors commonly focus on fees (69%), performance (41%), index methodology (37%) and index customization potential (34%), as shown in Exhibit 1.2

These priorities reflect direct indexing SMA users’ focus on cost efficiency, outcomes and the flexibility to shape portfolios around client-specific objectives.

Key Considerations for Evaluating the Underlying Index

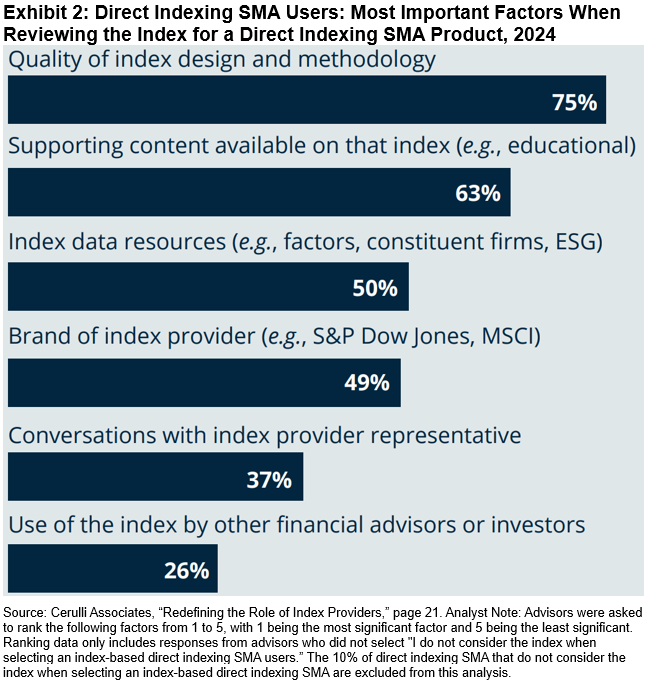

In their review of a direct indexing SMA’s underlying benchmark, financial advisors commonly focus on quality of index design and methodology (75%), supporting content available on that index (63%), index data resources (50%), brand of the index provider (49%) and conversations with an index provider representative (37%), as shown in Exhibit 2.

Index providers with strong brand equity can be an important resource by supplying the above index information to advisors for client conversations. According to Cerulli, most financial advisors using direct indexing SMAs report using index performance data (90%), index design and methodology information (83%), and performance attribution analyses (82%)2—all of which are readily available and accessible from leading index providers.

Index providers “collaborate with us on index design; we use their data and [they] help raise awareness and education for direct indexing,” an executive at an asset manager told Cerulli.3

Cerulli reports that 31% of direct indexing SMA advisors actively engage with index providers, while 35% expect they will engage more in the future.2 This growing trend underscores the potential for index providers to act as a key resource to advisors using direct indexing SMAs as they seek to improve their practices’ functions.

Opportunities for Direct Indexing SMA Users

The survey results suggest that direct indexing SMA users value index providers that can deliver both flexibility and education. Advisors in this segment may need resources that help explain to clients how and why a customized index may align with their objectives.

By providing accessible supporting content, robust data resources and opportunities for direct engagement, index providers offer resources that help these advisors differentiate their practices as direct indexing adoption continues to grow.

To learn more about how financial advisors are using direct indexing SMAs and working with index providers, explore the full Cerulli whitepaper, “Redefining the Role of Index Providers.”

1 The Cerulli Associates whitepaper “Redefining the Role of Index Providers” was sponsored by S&P Dow Jones Indices. Please see page 4.

2 Please see page 21 of Cerulli Associates’ “Redefining the Role of Index Providers.”

3 Please see page 5 of Cerulli Associates’ “Redefining the Role of Index Providers.”

The posts on this blog are opinions, not advice. Please read our Disclaimers.