The Middle East is a rapidly evolving region and one of its key growth areas has been factor indexing. The increasing adoption of these strategies has been driven by a desire for risk reduction, enhanced returns and cost efficiencies. This trend is evident not only in the adoption of single-factor styles but also in multi-factor approaches that combine single factors with low correlations for greater diversification.

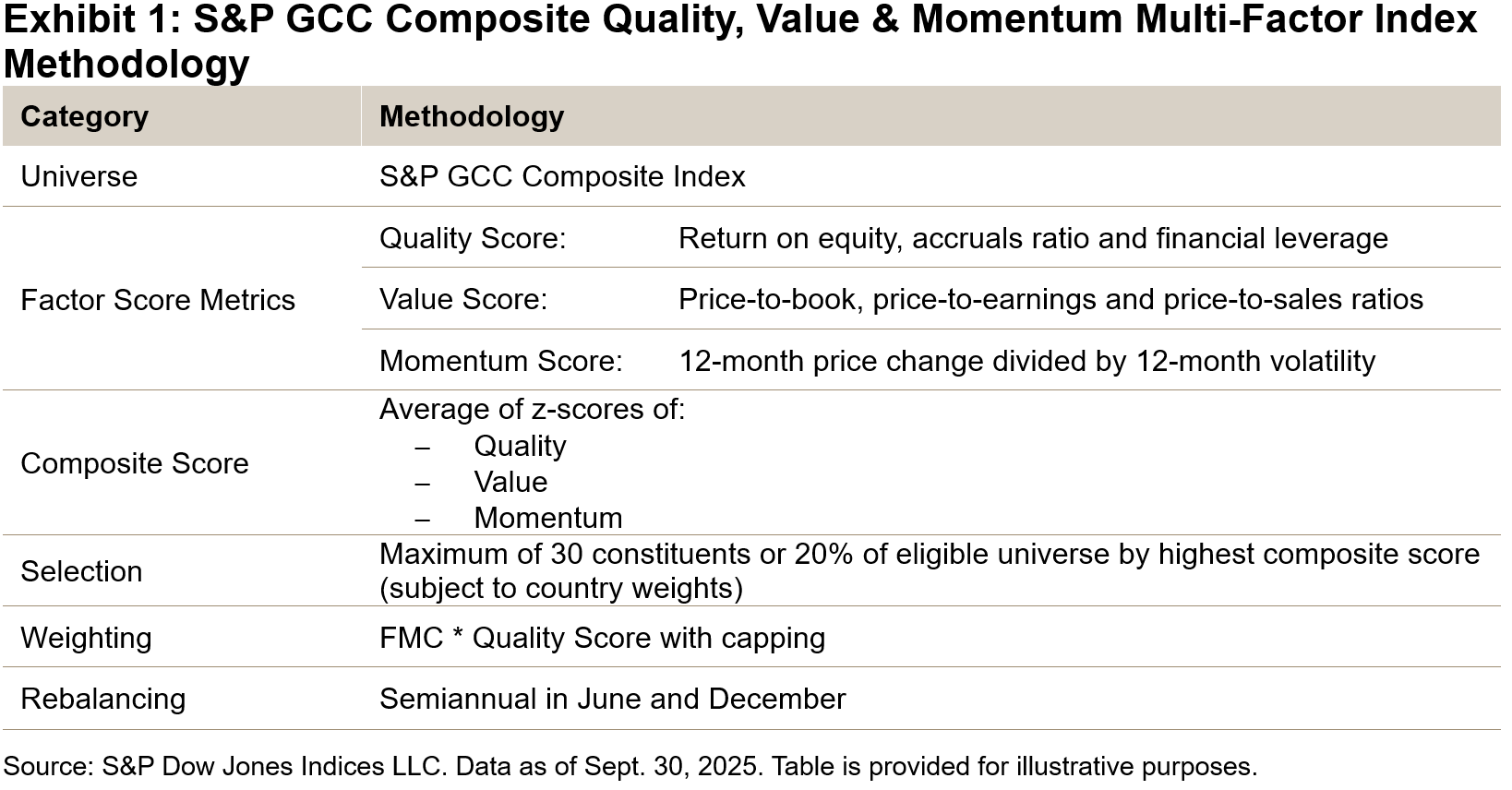

The S&P GCC Composite Quality, Value & Momentum (QVM) Multi-Factor Index tracks companies within the GCC area—comprising Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates (UAE)—that exhibit the highest combined scores in quality, value and momentum. Utilizing a bottom-up approach, the index averages each constituent’s individual factor scores to produce a combined multi-factor score, identifying constituents that score highly, on average, across each factor.

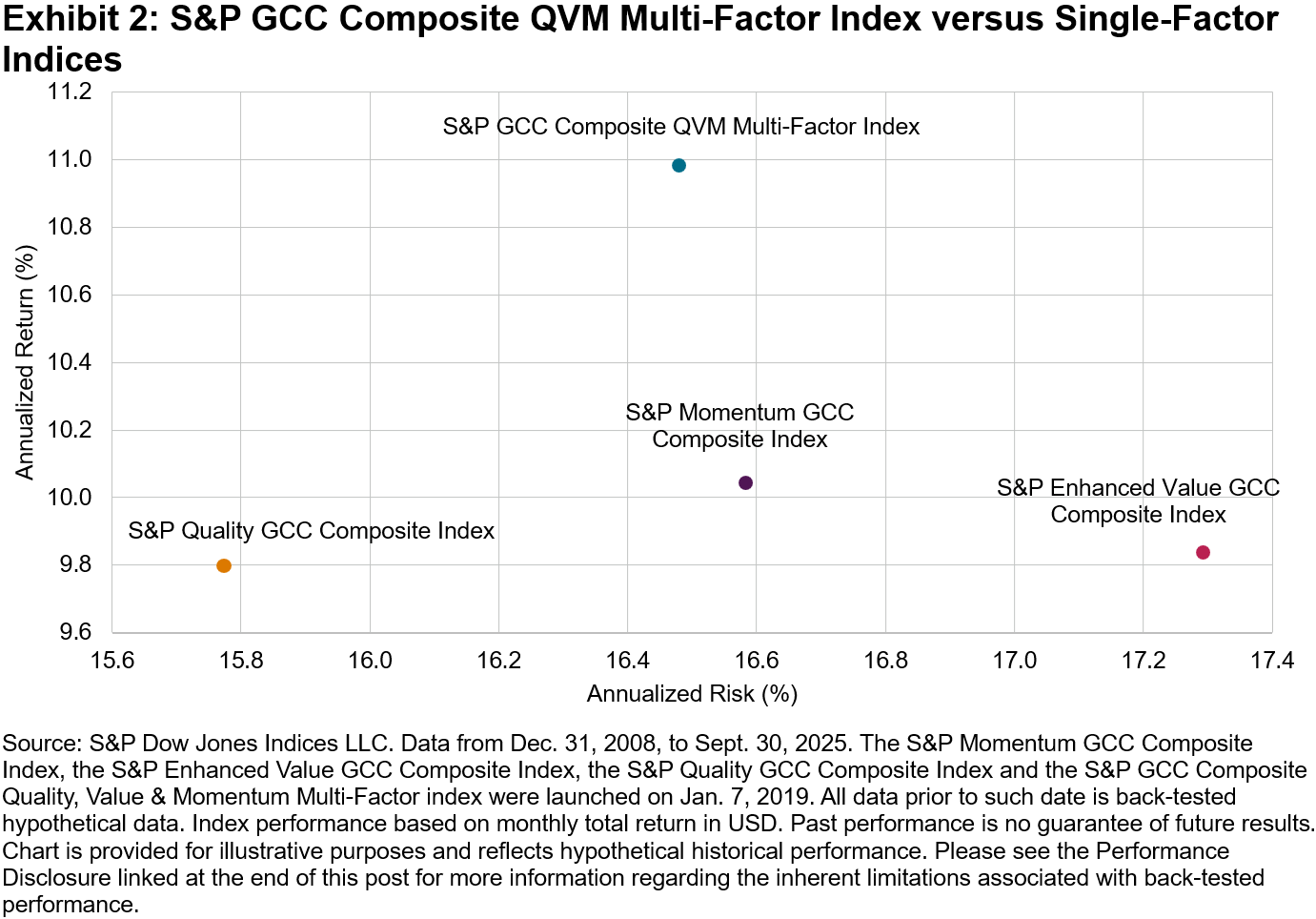

Higher Risk-Adjusted Returns Relative to Single-Factor Indices

The combination of quality, value and momentum has the potential to be complementary, as each factor may react differently to various phases of the business cycle. Quality tends to be more defensive, value is generally pro-cyclical, while momentum often outperforms during sustained market trends. By harnessing these factors in tandem, there is a possibility for improved risk-adjusted returns compared to relying on any single factor alone.

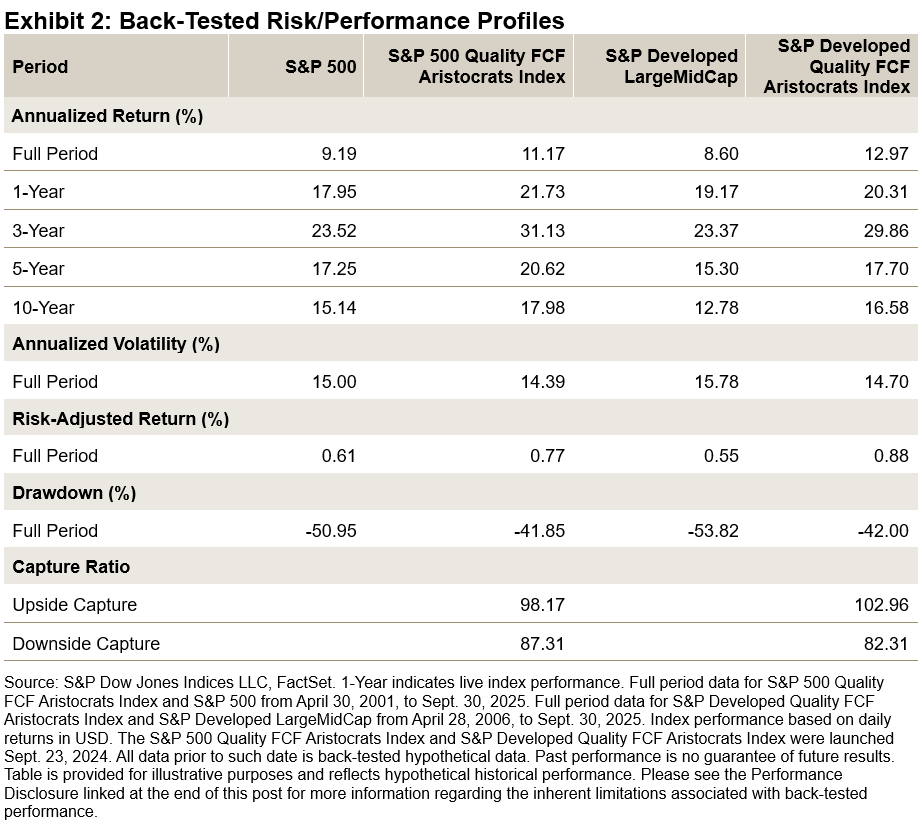

Exhibit 2 illustrates this point, showing that the annualized return per unit of risk was higher for the multi-factor index compared to the single-factor indices over the long term (2008-2025).

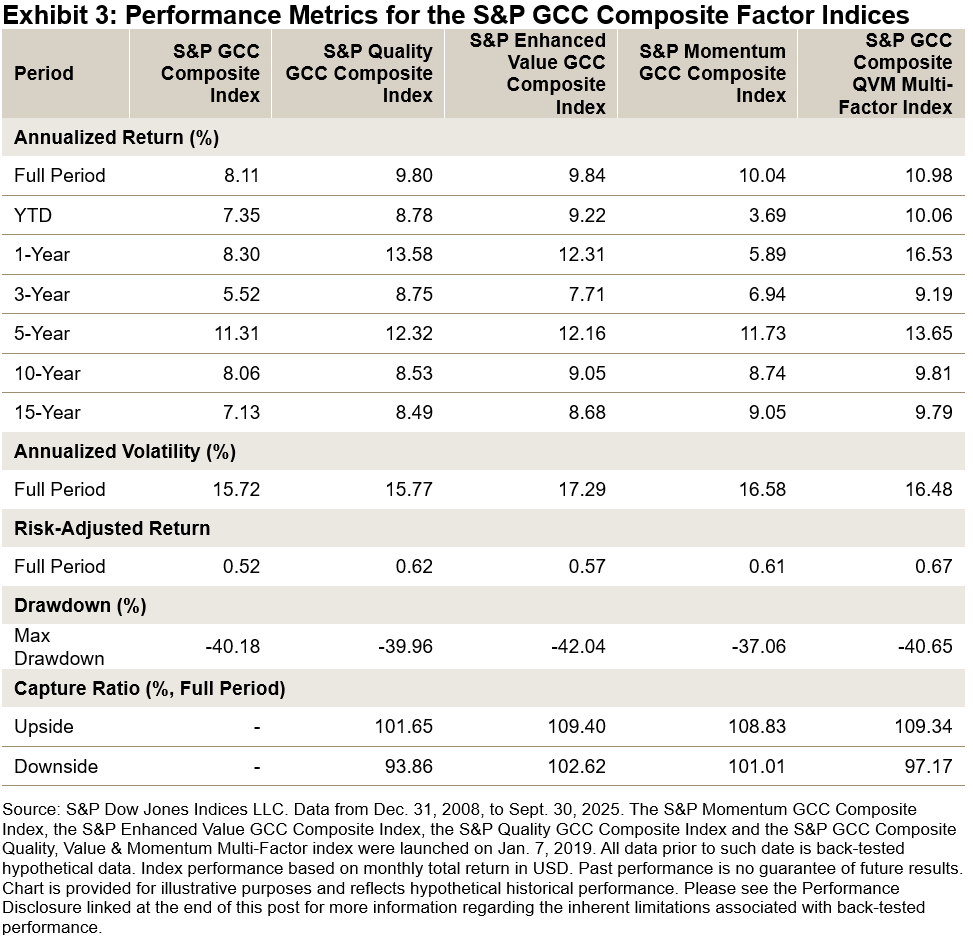

Strong Long-Term Outperformance

The S&P GCC Composite QVM Multi-Factor Index outperformed each of the individual single-factor indices and its benchmark universe on both an absolute and risk-adjusted basis over the full back-tested period. In the shorter term, the index outperformed over one-, three- and five-year periods. A review of its capture ratios reveals that the index outperformed in upward-trending markets while maintaining moderate defensive qualities during downturns.

Diversification across the Economic Cycle

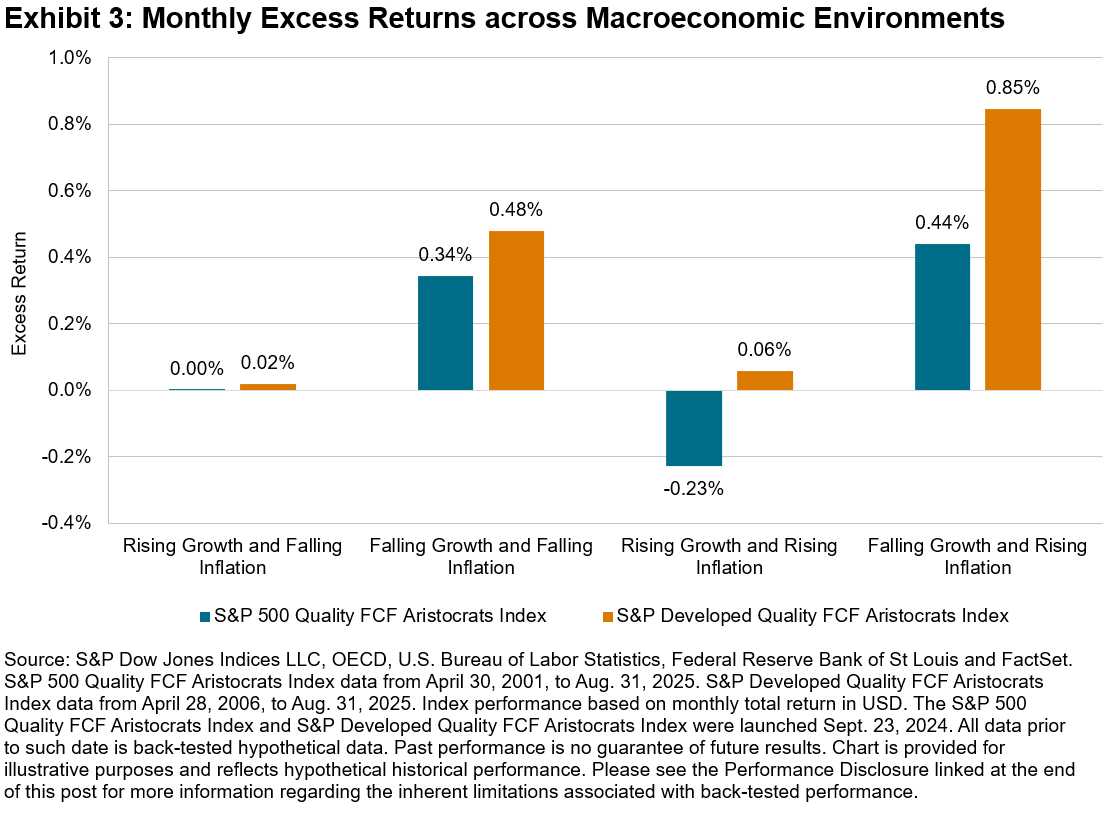

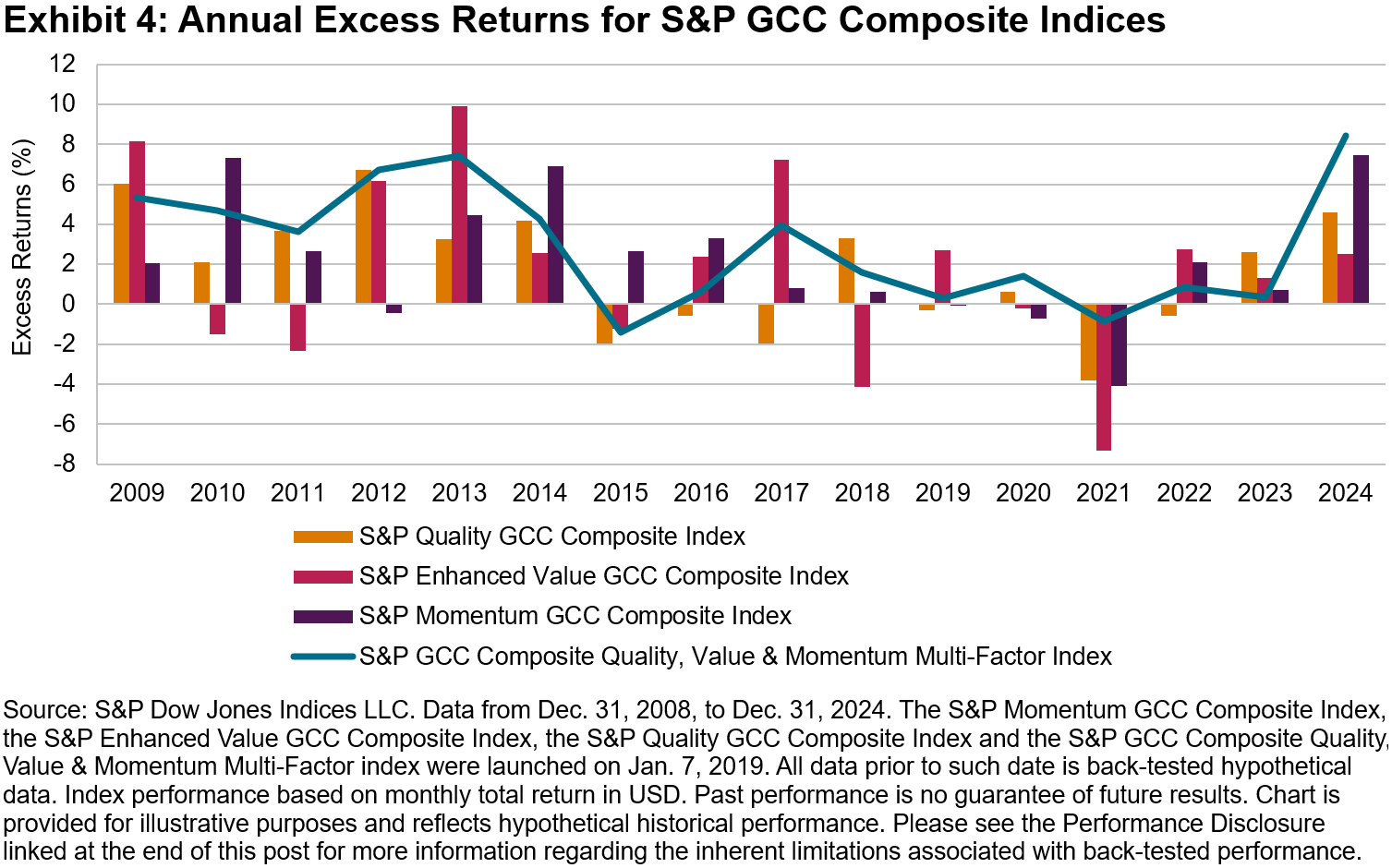

Most factors exhibit outperformance over the long run; however, none work all the time. Individual factor styles react in unique ways to the different phases of the economic cycles, outperforming at various stages. This is illustrated in Exhibit 4, which charts individual factor performance for each year between 2009 and 2024.

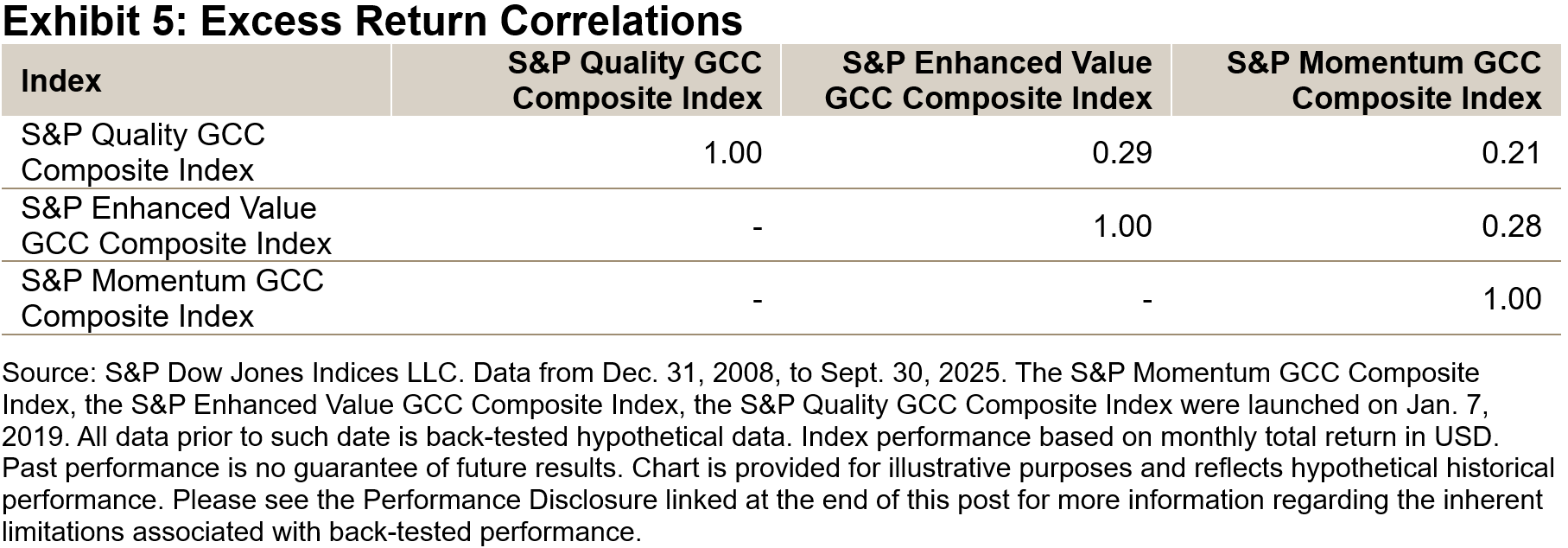

Low Excess Return Correlations

Some market participants may utilize single factors tactically, while others prefer multi-factor approaches that eliminate the need for precise timing. Exhibit 5 shows the historical low correlations of excess returns among the S&P GCC Single-Factor Indices. This characteristic is a key reason why combining these factors within the QVM methodology tends to result in a smoothing of risk-reward profiles.

Conclusion

By leveraging a multi-factor approach, there is a potential for diversification within the GCC markets versus the benchmark universe. The different factor characteristics such as the defensiveness of quality and the cyclical benefits of value across market cycles has helped to smooth performance for the S&P GCC Composite QVM Multi-Factor Index, with recent live and longer-term hypothetical back-tested performance showing enhanced risk-adjusted returns. A multi-factor strategy also has the potential to benefit from positive developments in the region. Additionally, those seeking to learn more about Shariah-compliant options may want to explore the S&P GCC Composite QVM Multi-Factor Shariah Index.

The posts on this blog are opinions, not advice. Please read our Disclaimers.