The S&P 500® surged to a third all-time closing high on Oct. 28, 2025, up 18% YTD. But the ride for U.S. equity investors has not always been a smooth one, with the index recouping sharp losses from earlier in the month on renewed tariff-related concerns and regional bank losses, coupled with AI bubble1 jitters looming in the background.

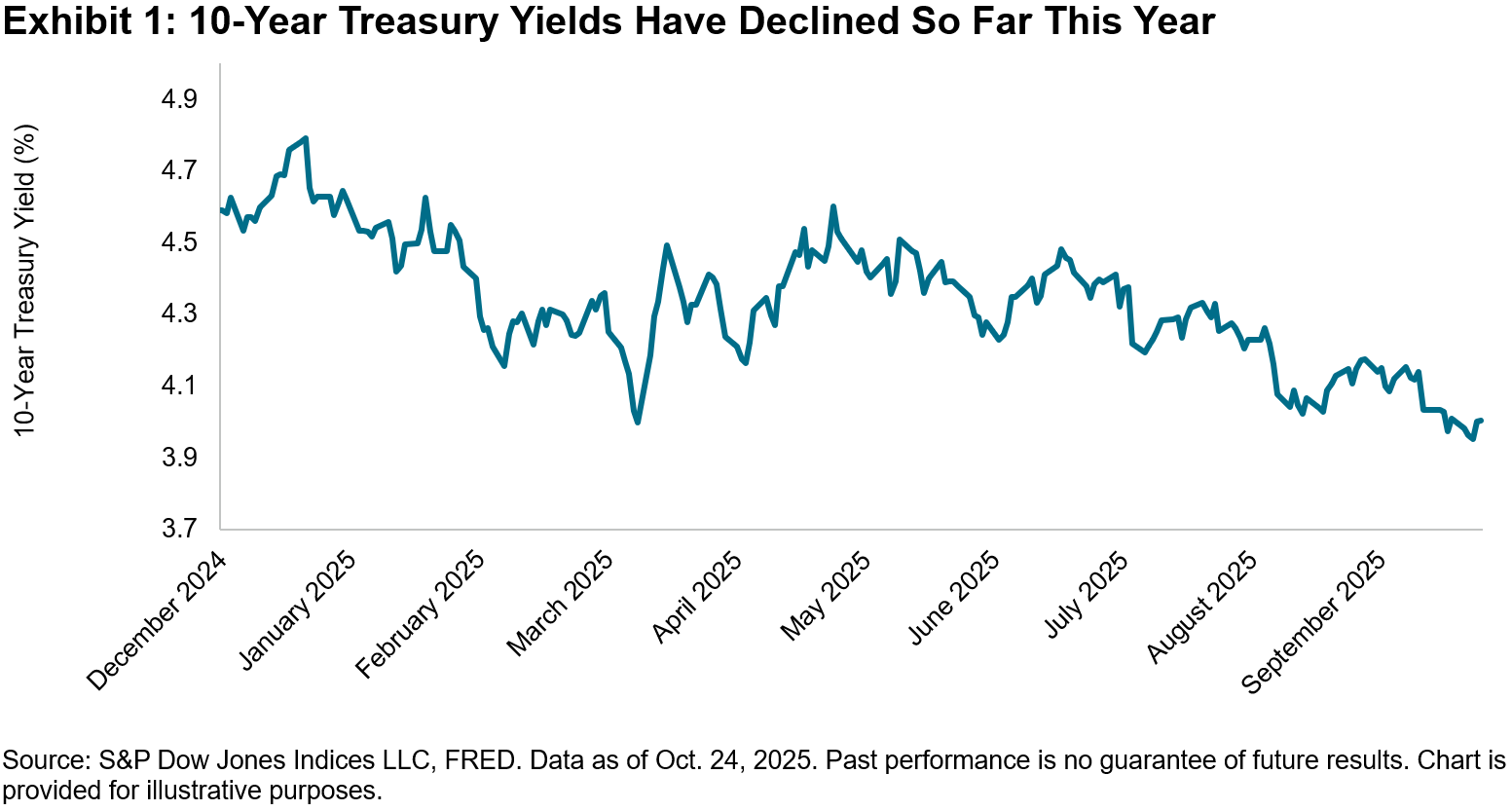

Turning to the fixed income markets, the closely watched 10-year U.S. Treasury yield has declined so far this year, falling below the 4% handle, thanks to optimism surrounding potential upcoming Fed rate cuts and expectations of an end to quantitative tightening, better-than-expected inflation results and increased safe-haven demand amid corporate credit concerns and a government shutdown.

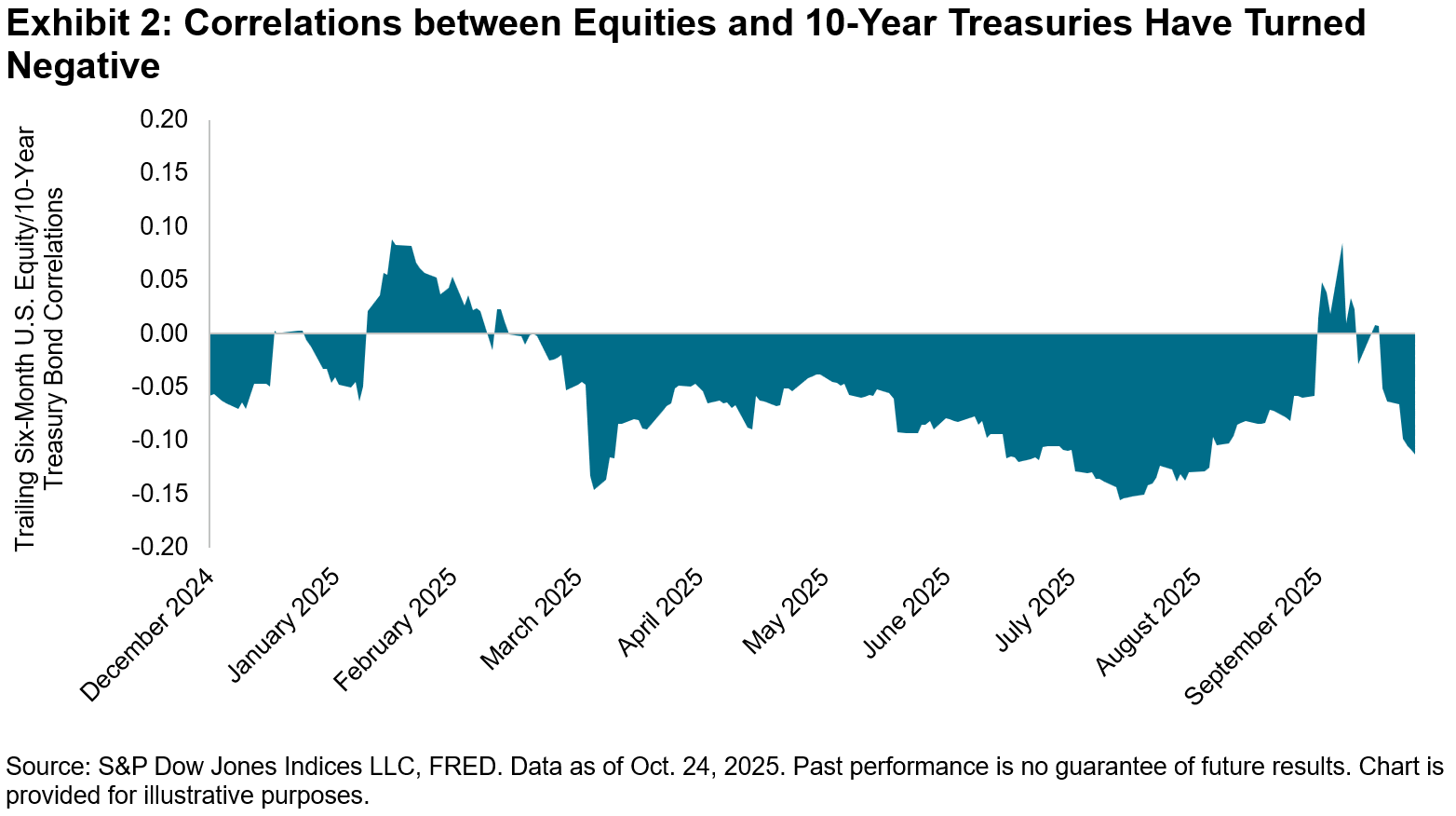

So how can market participants think about diversification and risk reduction in this shifting market environment? We began by analyzing the interaction of equities versus bonds, calculating the historical six-month correlations of the returns of the S&P 500 versus the S&P U.S. Treasury Bond Current 10-Year Index. After having witnessed negative correlations since the early April market tumult, when equities plummeted and market participants sought the refuge of Treasuries, correlations briefly turned positive but recently reversed again into negative territory, showing diversification potential across the two asset classes.

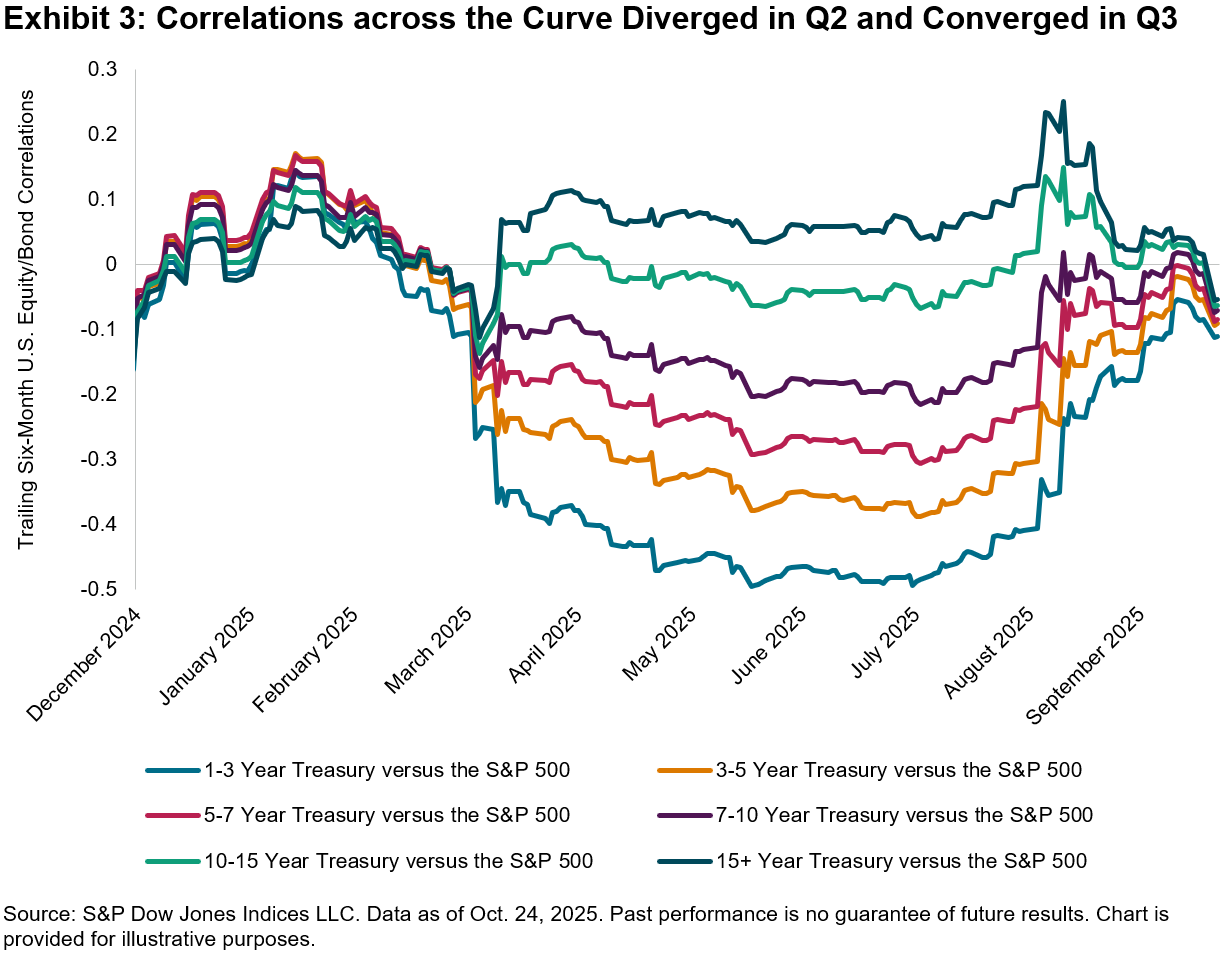

However, for a more nuanced perspective of the relationship between equities and fixed income, analyzing bonds across various durations or interest rate sensitivities may be helpful. Next, we calculated correlations of S&P 500 performance across the entire Treasuries curve, from 1-3 year to 15+ year maturities, using our suite of iBoxx $ Treasuries indices.

We observed that from April to September, there was a wide divergence across correlations, with longer-term Treasuries providing less diversification compared to short-term Treasuries, which had consistently lower correlations versus equities. Although these correlations have since converged, the diversification benefits of equities versus bonds can vary depending on which part of the curve Treasuries are situated in.

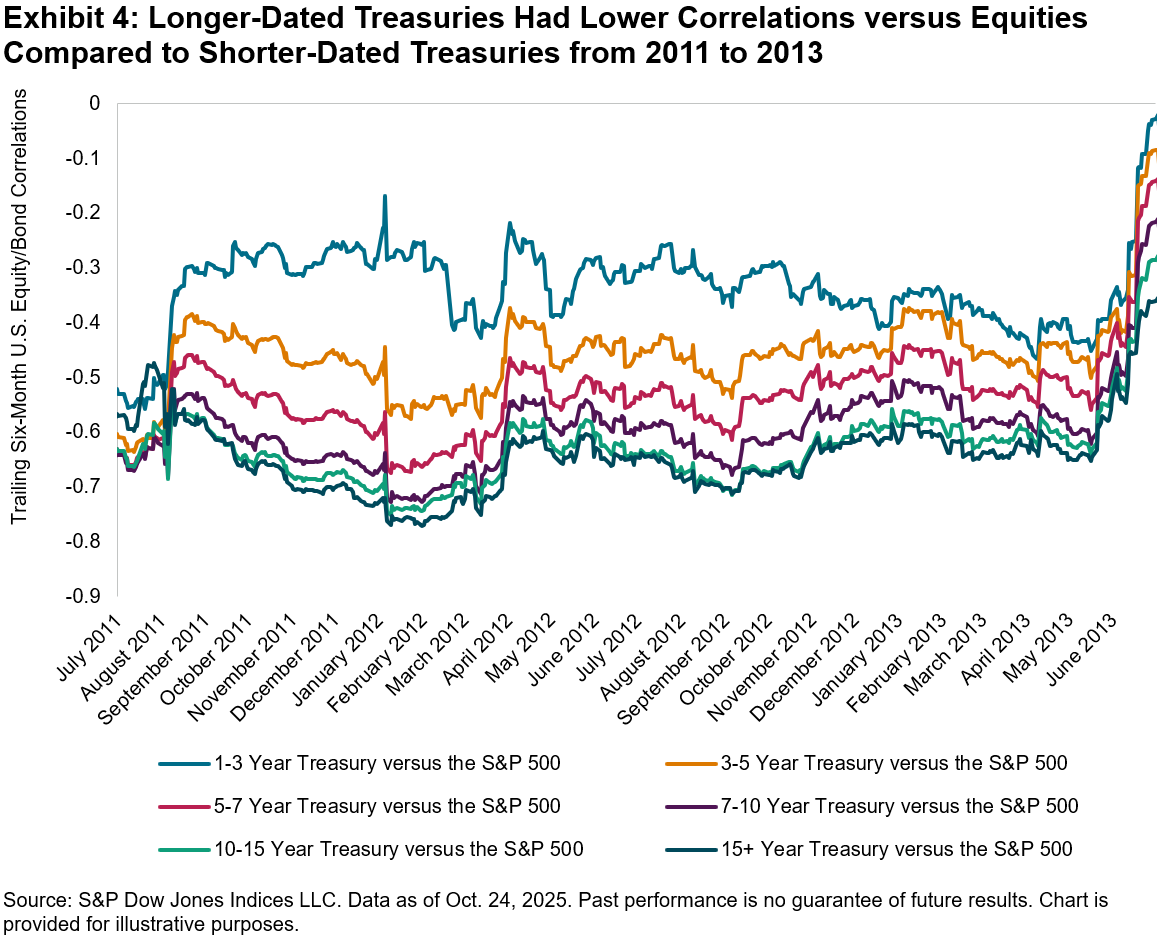

Another example of when correlations between equities and bonds varied across the Treasuries curve was from August 2011 to May 2013, characterized by momentous events like the European debt crisis, when market participants sought safe havens like Treasuries, and the Fed’s “Operation Twist,” which involved selling shorter-dated Treasury debt and buying longer-dated debt. During this period, however, shorter-dated Treasuries provided acted as less of a diversifier, with higher relative correlations to equities compared to longer-duration bonds.

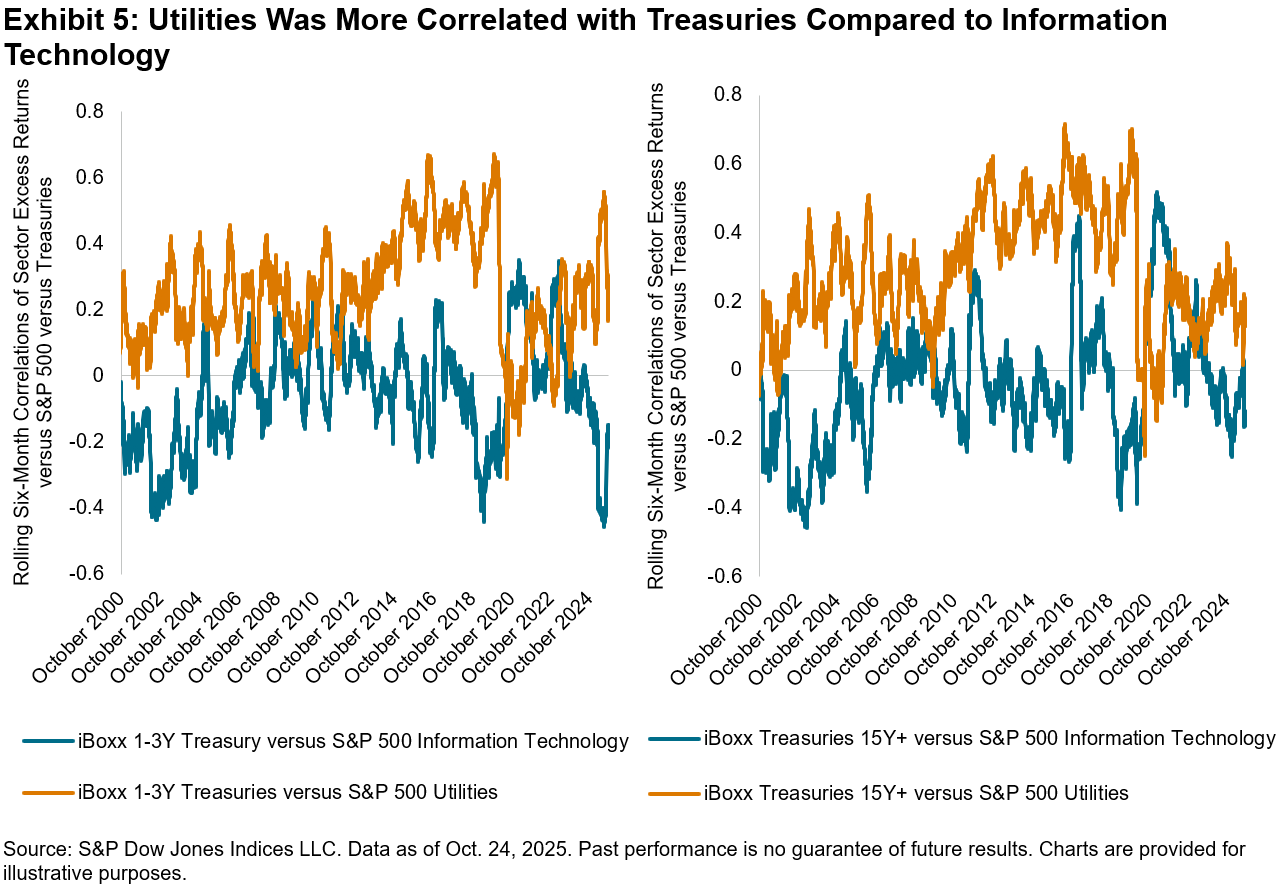

For an even more granular perspective across equities, we can compare the correlations of Treasuries across durations versus individual sectors. Sampling classically cyclical Information Technology and traditionally defensive Utilities, Exhibit 5 displays the historical six-month correlations of the excess returns of S&P 500 Information Technology and S&P 500 Utilities versus the iBoxx $ Treasuries 1-3 Year and iBoxx $ Treasuries 15 Years+. Unsurprisingly, Utilities generally exhibited a stronger correlation with short and longer-duration bonds compared to Information Technology, which, given the tech-heavy nature of the large-cap equity market, may indicate that the diversification ballast offered by bonds may be particularly germane in the current market regime.

Understanding equity movements versus bonds, both across the duration spectrum and across sectors, may be especially relevant as we anticipate the Fed’s upcoming rate decision and Big Tech earnings this week, and as the beginning of Q4 approaches.

The posts on this blog are opinions, not advice. Please read our Disclaimers.