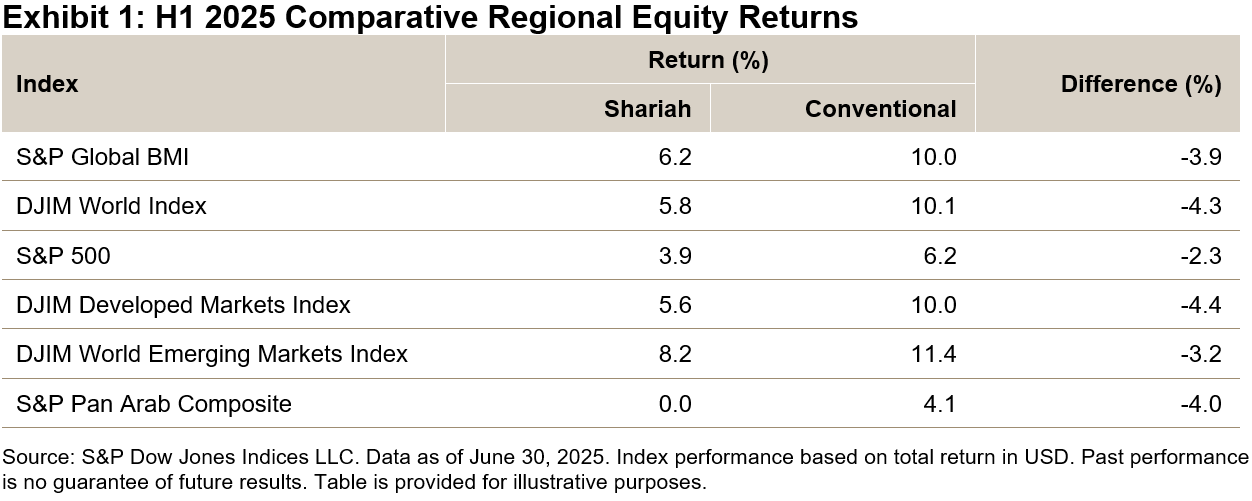

In the first half of 2025, global equities faced significant volatility, primarily driven by developments related to U.S. tariffs. Steep declines between February and April were followed by a swift recovery, and the S&P Global BMI ultimately finished with a solid 10.0% return. U.S. equities underperformed, breaking their streak of extended outperformance, as the S&P 500® rose by only 6.2% in U.S. dollar terms (and rose significantly less or declined in most other major currency terms due to notable depreciation of the U.S. dollar). Meanwhile, influenced in part by declining oil prices, MENA equities are on track to record a third consecutive year of underperformance, with the S&P Pan Arab Composite posting a modest YTD return of 4.1% by the year’s midpoint.

A trend reversal was also observed in the relative performance of Shariah-compliant benchmarks, which underperformed their conventional counterparts across the board. The S&P Global BMI Shariah and Dow Jones Islamic Market (DJIM) World Index trailed their conventional equivalents in H1 by 3.9% and 4.3%, respectively (see Exhibit 1). This shift follows a cumulative outperformance of over 14% in the previous five years.

Drivers of Shariah Index Performance in H1 2025

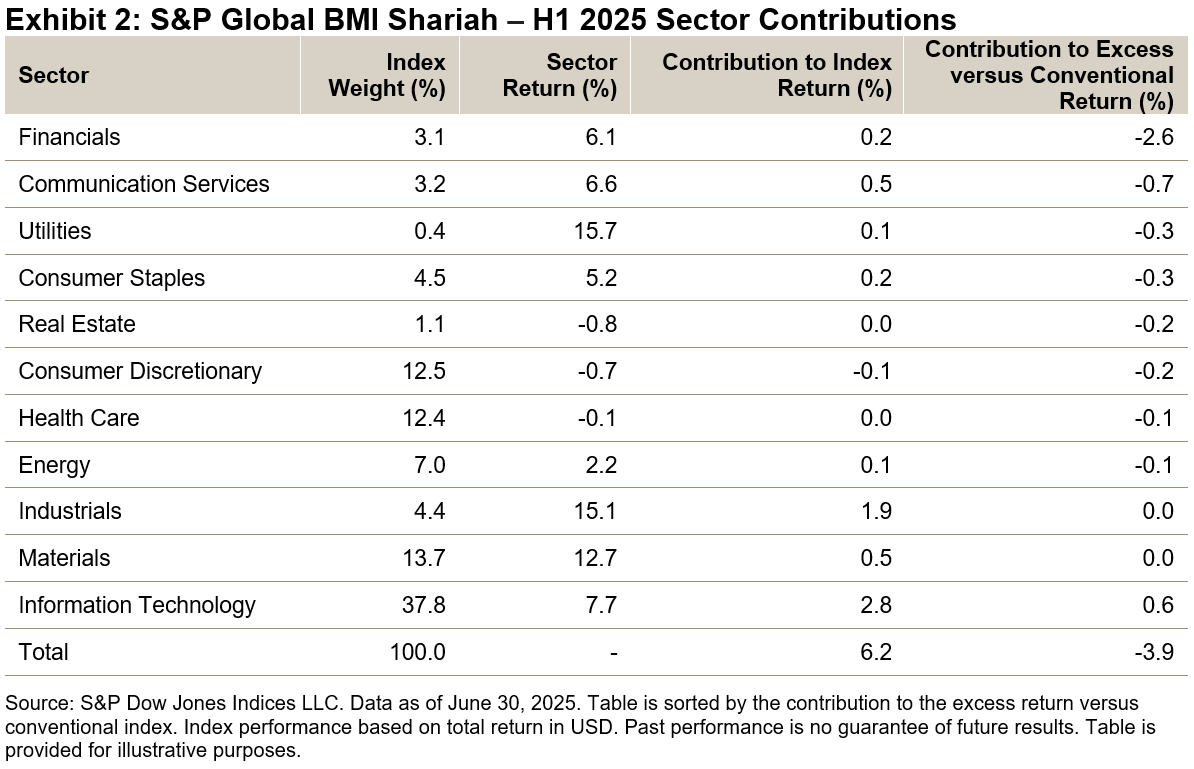

The underperformance of Shariah benchmarks is analyzed through a sector lens in Exhibit 2. Financials contributed the largest negative excess return of -2.6%, primarily due to the outperformance of non-Shariah-compliant financial companies—such as conventional banks, brokerage firms and asset managers—relative to their Shariah-compliant counterparts. Meanwhile, telecommunications companies, which typically hold lower weightings in Shariah benchmarks due to their higher levels of indebtedness, outperformed during the market turbulence, contributing to the negative excess return by the Communication Services sector.

Global Sukuk Rallied

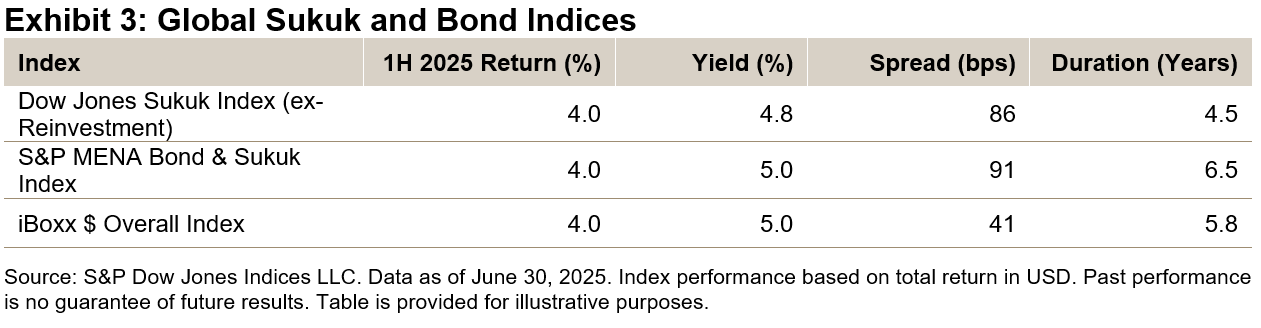

Global fixed income markets had a strong run in H1, bolstered by moderating inflation and expectations of further rate cuts. U.S. dollar-denominated investment grade bonds and sukuk, as measured by the iBoxx $ Overall Index and Dow Jones Sukuk Index (ex-Reinvestment), both delivered solid returns of 4.0%. With improving global liquidity conditions, the issuance of foreign-currency-denominated sukuk is expected to continue growing, thereby supporting high financing needs in core Islamic economies in 2025.1

This article was first published in IFN Volume 22 Issue 28 dated July 16, 2025.

1 See “Islamic Finance 2025-2026: Resilient Growth Amid Upcoming Headwinds”, S&P Ratings, April 2025.

The posts on this blog are opinions, not advice. Please read our Disclaimers.