Rethinking Diversification in a Volatile Market

Recent market volatility has highlighted the risks of relying solely on technology-driven U.S. large-cap stocks for long-term returns. With shifts in global economic cycles and increasing geopolitical tensions, diversification has become even more relevant. Focusing only on U.S. equities may mean missing valuable opportunities abroad, particularly in Europe. The S&P Europe 350® measures leading companies across diverse sectors in 16 developed European markets, which could complement a U.S.-focused approach.

European Equities Outperformance YTD

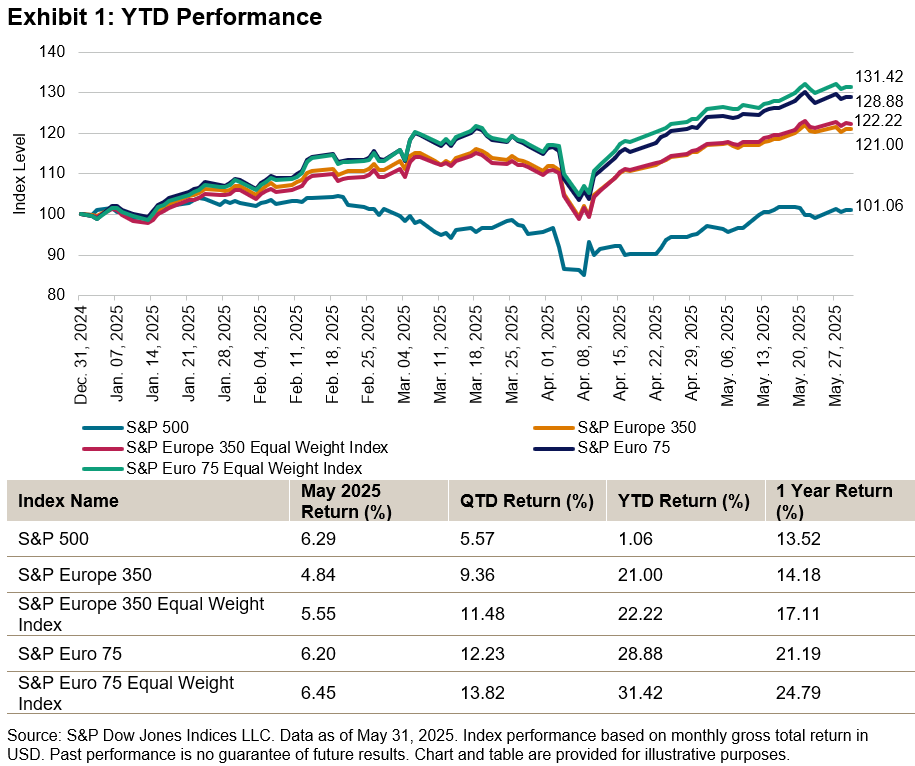

In the first half of 2025, European equities showed significant resilience. As shown in Exhibit 1, the S&P Europe 350 gained 21%, while the S&P 500® remained nearly flat, increasing only 1%. The S&P Euro 75, which targets the eurozone, performed even better, with gains approaching 29%. This outperformance was mostly driven by Europe’s controlled inflation, accommodative monetary policy and increased public investment in infrastructure and defense. Moreover, favorable valuations and strong corporate earnings have further enhanced investor confidence and global capital flows into the region.

Diversification Impact

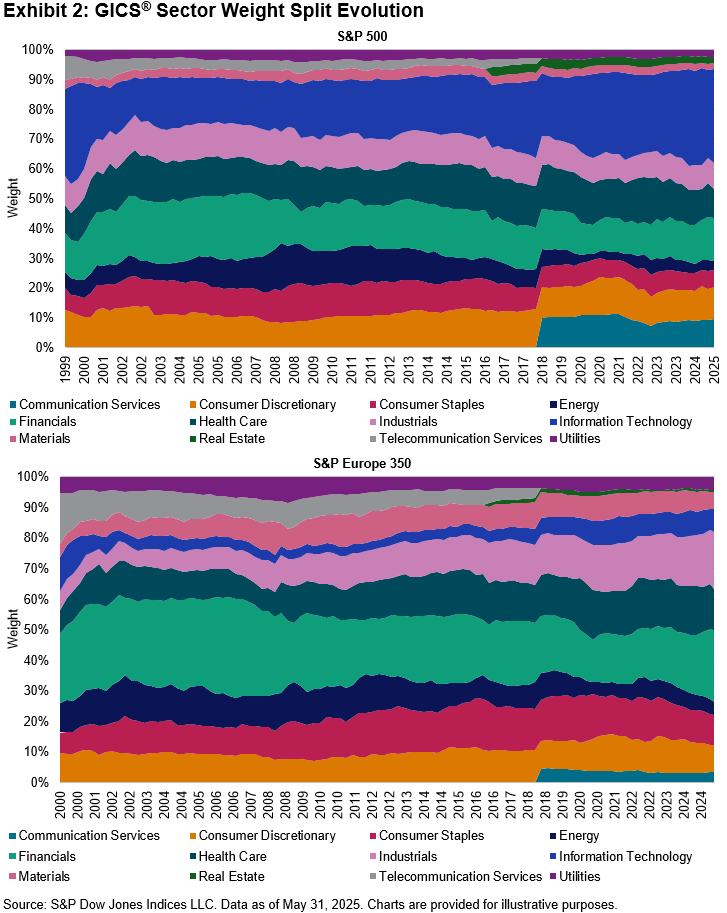

One possible advantage of European equities is its sector exposure compared to U.S. markets. As of May 31, 2025, the S&P Europe 350 had greater weights in Financials, Industrials and Healthcare, while The 500™ was predominantly weighted toward Information Technology (see Exhibit 2). This difference could help mitigate sector risks and lead to a more diversified industry representation. Furthermore, the S&P Europe 350 is less concentrated in its largest constituents, with its top five companies accounting for just over 12% of the index, in contrast to nearly 25% in The 500, making the index performance more broad based.

Periods of Outperformance and Current Drivers

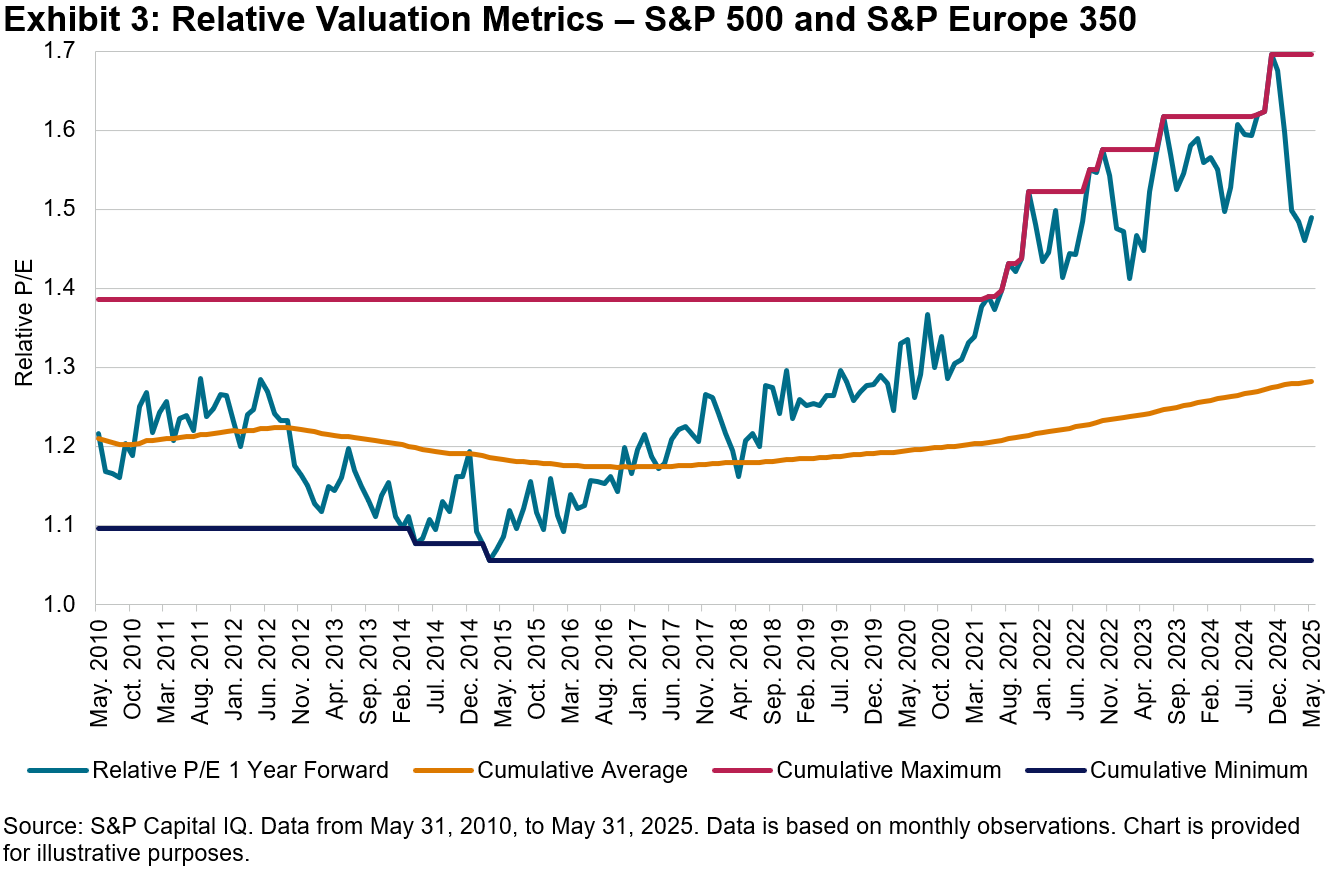

European equities have outperformed their U.S. counterparts over different periods in recent decades, driven by valuation disparities, sector and style rotation and divergent macroeconomic policies. Today, Europe is undergoing a structural transformation, with substantial investments in infrastructure, energy transition and defense—underpinned by revised fiscal frameworks and enhanced EU-level funding mechanisms. These developments could foster new avenues for growth and reignite investor interest. As of May 31, 2025, the S&P Europe 350 traded at a forward price-to-earnings ratio of 15.13, below its 15-year average. In contrast, the S&P 500 commanded a significantly higher multiple of 22.09—a premium of approximately 50% relative to its European counterpart, positioning this premium midway between its mean of 28% and peak of 70% over the past 15 years (see Exhibit 3).

European Equities: Passive Strategies Lead

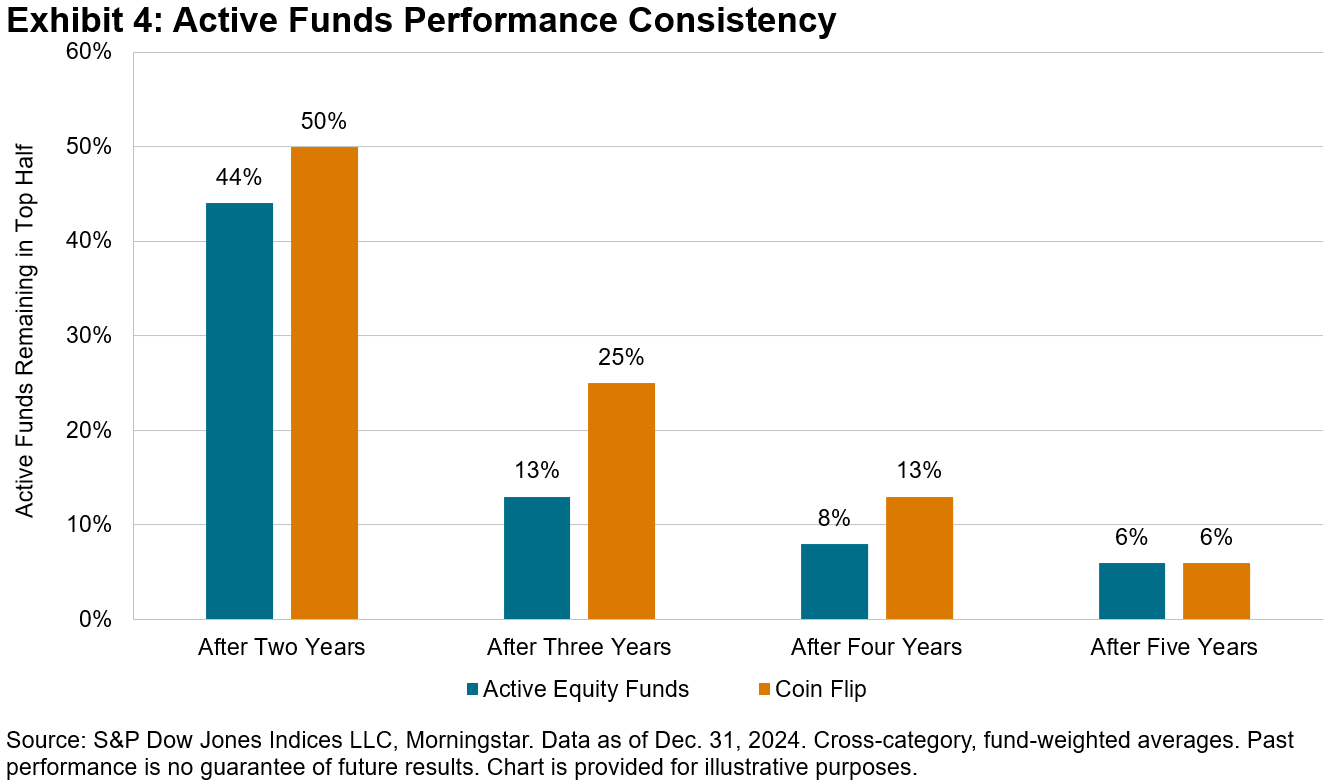

Our SPIVA Europe Year-End 2024 Scorecard shows that the majority of active funds underperformed their benchmarks over short- and long-term periods. On average, EUR-denominated Europe Equity active funds trailed the S&P Europe 350 by 5.11%. Furthermore, our Europe Persistence Scorecard has observed that maintaining consistent outperformance can be challenging for active managers over extended timeframes (see Exhibit 4).

Conclusion

When considering diversification beyond U.S. markets, European equities stand out due to attractive valuations, distinct sector composition and compelling structural trends. These factors suggest that Europe may be well positioned for long-term growth. In this context, European equity indices like the S&P Europe 350 could prove to be effective tools for navigating this evolving market landscape.

The posts on this blog are opinions, not advice. Please read our Disclaimers.