Rebalance Review of the S&P Global Clean Energy Transition Index – H1 2025

Launched in 2007, the S&P Global Clean Energy Transition Index has been a headline benchmark for measuring clean energy-related companies’ performance over the past 17 years. In April 2021, we launched the S&P Global Clean Energy Select Index to measure the performance of the 30 largest companies in global clean energy businesses listed on developed market exchanges.

S&P Global Clean Energy Transition Index Rebalance in April 2025

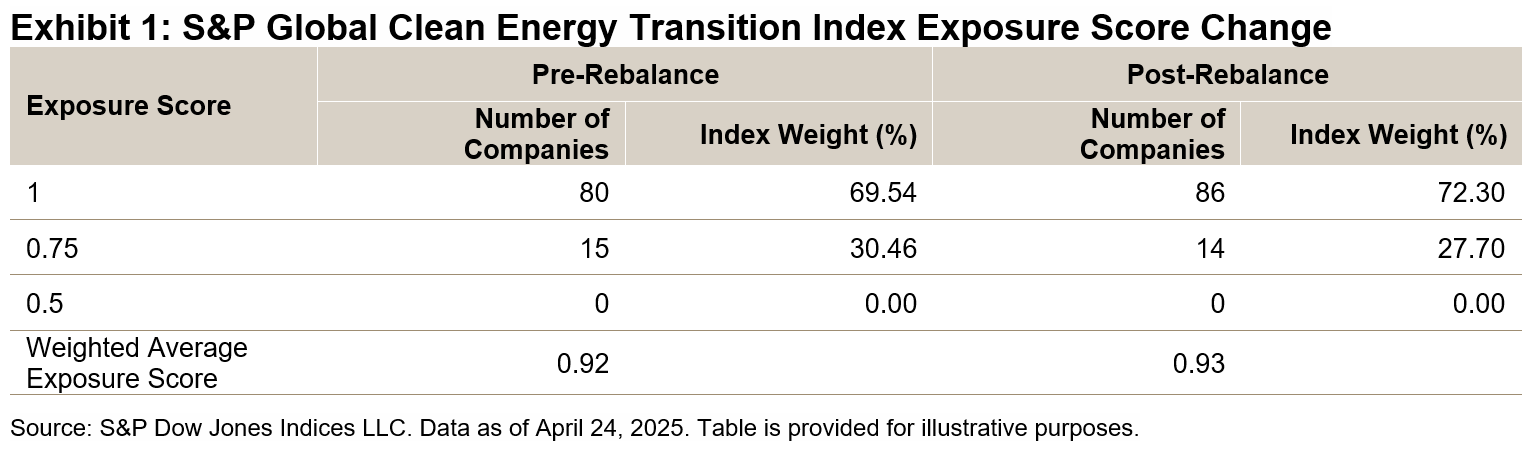

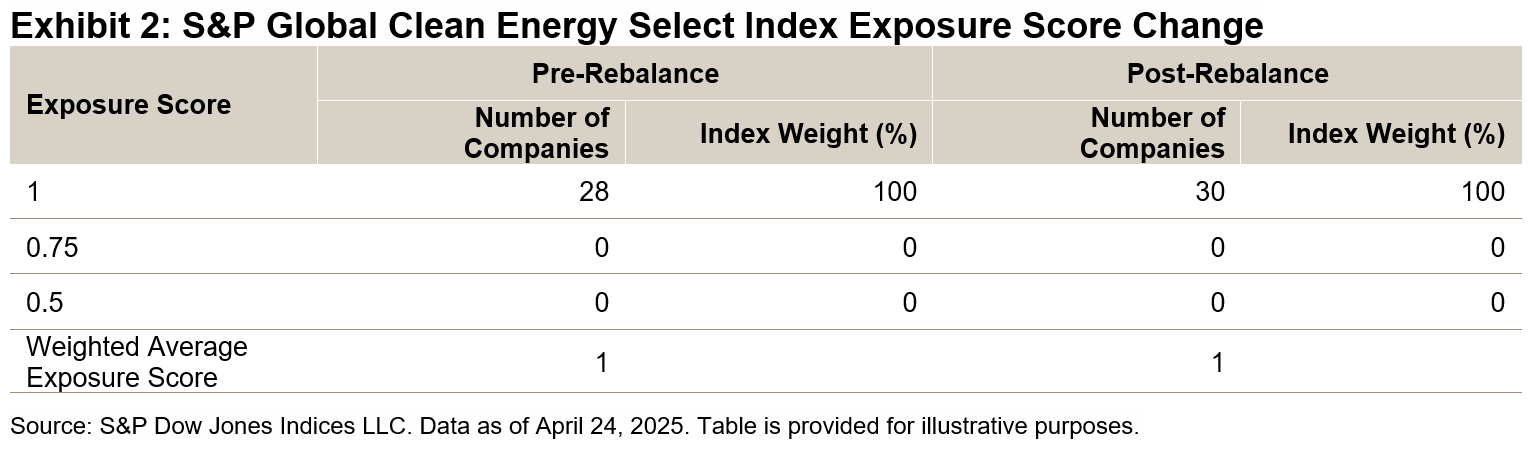

The index methodology calculates exposure scores for each company to assess their clean energy business purity, utilizing the GICS® classification system, FactSet’s Revere Business Industry Classification System (RBICS) and S&P Global Trucost’s power generation data. Companies are categorized into four exposure score buckets, ranging from 0 to 1 in increments of 0.25, reflecting increasing levels of clean energy business relevance. Both indices had their semiannual rebalances on April 24, 2025. Exhibits 1 and 2 show the change in exposures before and after the April rebalance for both indices.

For the S&P Global Clean Energy Transition Index, the weighted average exposure score increased slightly from 0.92 to 0.93 (see Exhibit 1). The S&P Global Clean Energy Select Index consists of 30 companies with an exposure score of 1 listed on the developed market exchanges (see Exhibit 2).

In the geographical exposure breakdown, prominent changes in the S&P Global Clean Energy Transition Index following the rebalance include a 3.67% weight increase for the U.S. and a 0.96% increase for China, alongside a 1.25% decrease for Spain. Meanwhile, in the S&P Global Clean Energy Select Index, China’s weight rose by 4.37% and New Zealand’s weight rose by 3.46%, while the weight of Canada declined by 2.05%.

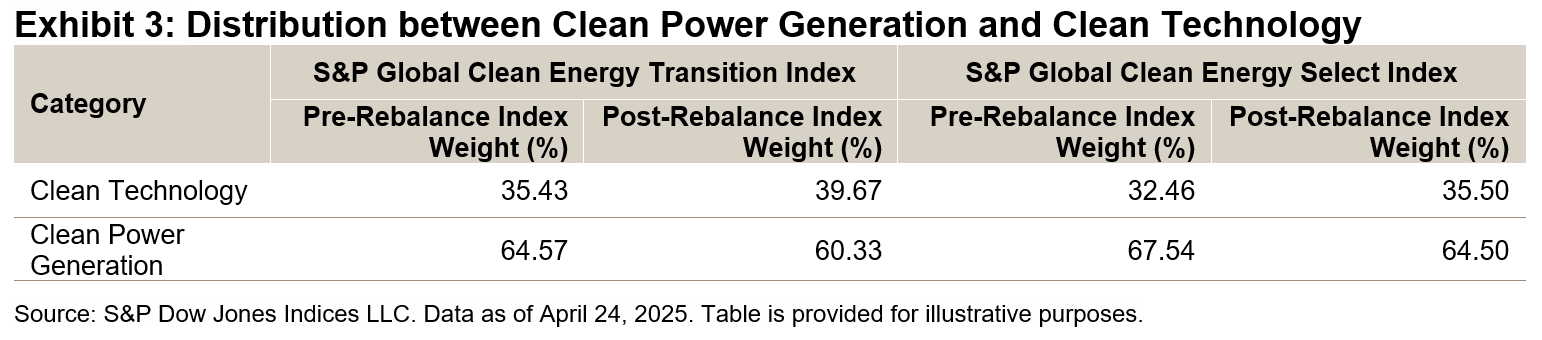

In the energy category, companies are classified into Clean Technology and Clean Power Generation based on RBICS subindustries. Clean Technology encompasses subindustries that focus on clean energy systems and manufacturing, while Clean Power Generation includes various wholesale power and electric utilities subindustries.

During the recent rebalance, the weights for clean technology increased in both indices (see Exhibit 3), primarily driven by significant gains in the weights of the Photovoltaic and Solar Cells and Systems Providers subindustries, as well as Fuel Cell Equipment and Technology Providers. Conversely, the index weight for clean power generation declined, largely due to a 1.22% decrease in the Europe Mixed Wholesale Power RBICS subindustry for the S&P Global Clean Energy Transition Index and a 1.74% decrease in the same subindustry for the S&P Global Clean Energy Select Index.

S&P Global Clean Energy Transition Index Performance YTD in 2025

As of May 30, 2025, the S&P Global Clean Energy Select Index achieved an 8.84% total return YTD in USD terms, while the S&P Global Clean Energy Transition Index gained 11.54%. Both indices outperformed the S&P Global BMI, which stood at 5.5% for the same period.

Regarding regional performance, companies domiciled in Germany within the S&P Global Clean Energy Transition Index were up 71.63% YTD. South Korea followed with an increase of 53.77%, while Brazil gained 37.61%.1

The S&P Global Clean Energy Transition Index tracks the dynamic changes in the clean energy transition and reflects the performance of clean energy-related companies, serving as a key benchmark for the global clean energy sector.

1 Source: S&P Dow Jones Indices LLC and FactSet. Data as of May 30, 2025.

The posts on this blog are opinions, not advice. Please read our Disclaimers.