The S&P 500® continues to be a trusted benchmark for the broad U.S. market, measuring the performance of U.S. large-cap companies across various sectors. As the market moves, certain stocks and sectors grow to represent a larger share of the index, highlighting their significant influence on the economy. While this is the natural result of market-cap weighting, some market participants are exploring alternative strategies in pursuit of enhanced diversification.

In this blog, we introduce the S&P 500 Diversified Sector Weight Index, which aims to mitigate concentration risk and address sector imbalances by reweighting companies within The 500™. This innovative approach employs a hierarchical equal sector weight methodology, utilizing Syntax’s FIS® sector taxonomy.

FIS’s Sector Taxonomy

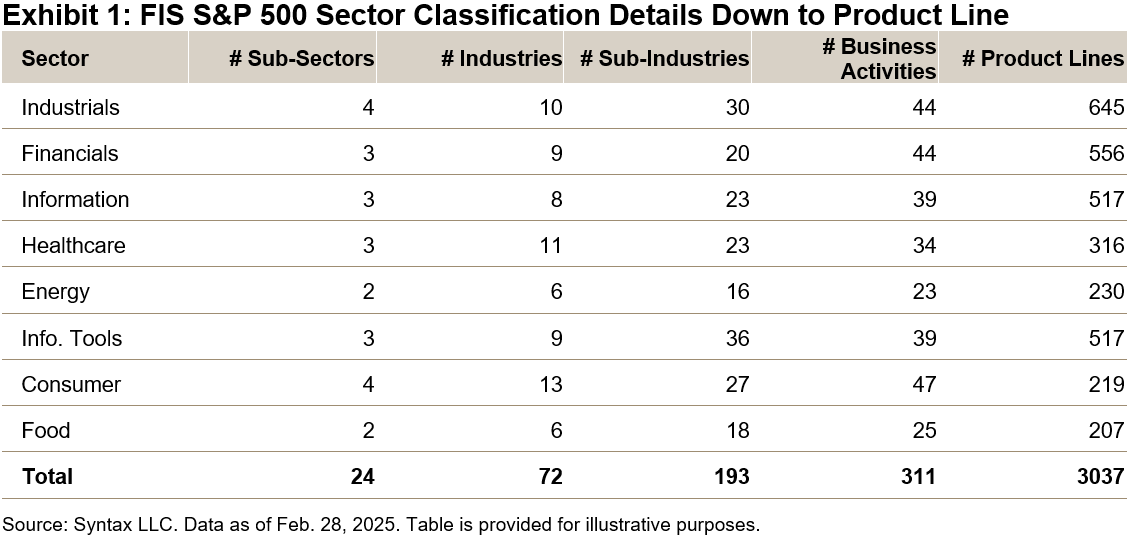

This six-level classification system captures the diverse business models and product lines of companies. As shown in Exhibit 1, the FIS sector taxonomy consists of 8 sectors, 24 sub-sectors, 72 industries, 193 sub-industries, 311 business activities and over 3000 individual product lines in the S&P 500 universe.

Index Methodology

The S&P 500 Diversified Sector Weight Index equally weights each of the eight primary sectors defined by Syntax FIS with quarterly rebalancing.1 Within each sector, level 2 sub-sectors are equally weighted, as are level 3 industries, and so forth down to business activities level (see Exhibit 2). At the lowest level, within each business activity,2 stocks are weighted proportionally based on the revenue generated within that specific activity.

Diversification Beyond Primary Business

Unlike traditional classification systems that categorize companies solely by their primary business segment, the FIS classification scheme enables a single company to be represented across multiple sectors and industries. As a result, if a company generates revenue from more than one business activity, its final weight in the index is the sum of the weights from each of its business activities.

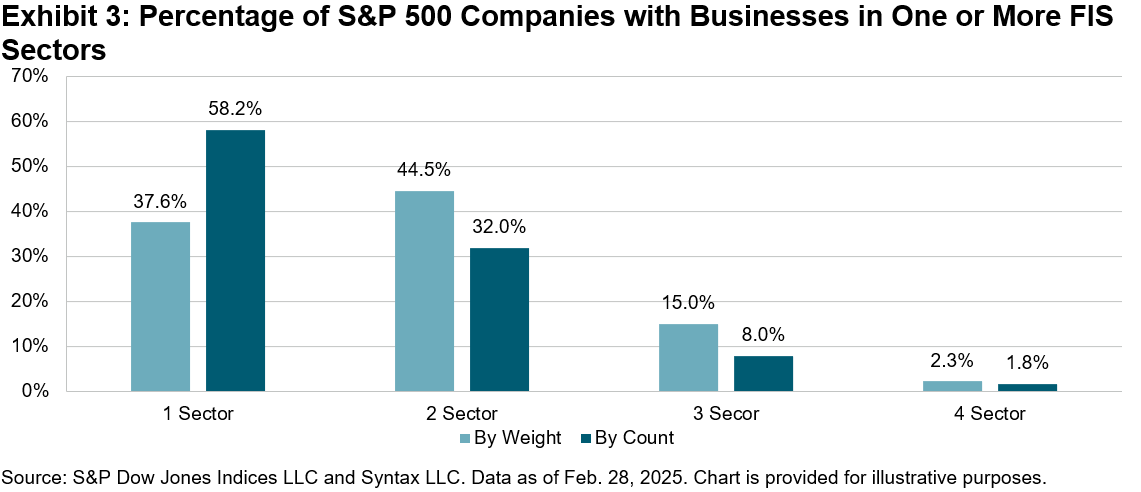

As shown in Exhibit 3, over 41% of S&P 500 companies engage in business activities across more than one FIS sectors, collectively accounting for 62% of the index’s total weight.

A Short- and Long-Term View of Performance

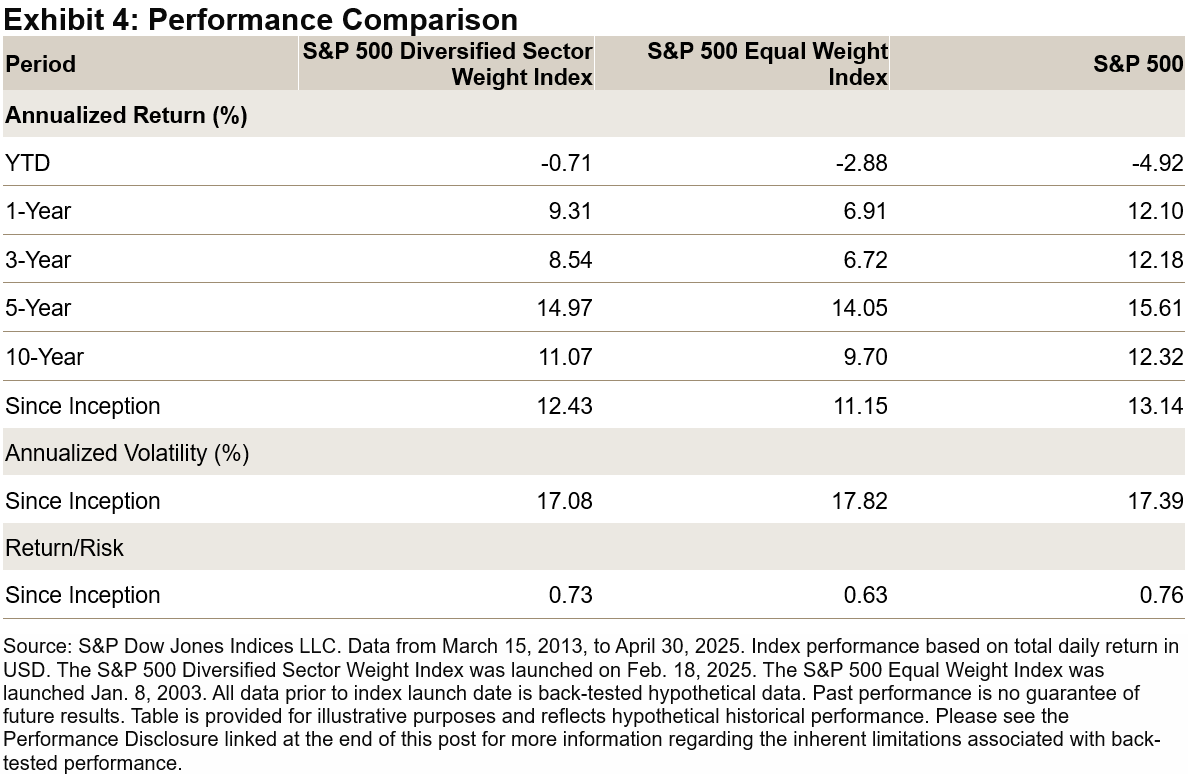

Exhibit 4 illustrates that S&P 500 Diversified Sector Weight Index has historically outperformed the S&P 500 Equal Weight Index in terms of both absolute returns and risk-adjusted returns, across both short- and long-term periods.

Characteristics of the S&P 500 Diversified Sector Weight Index

Sector Level Diversification

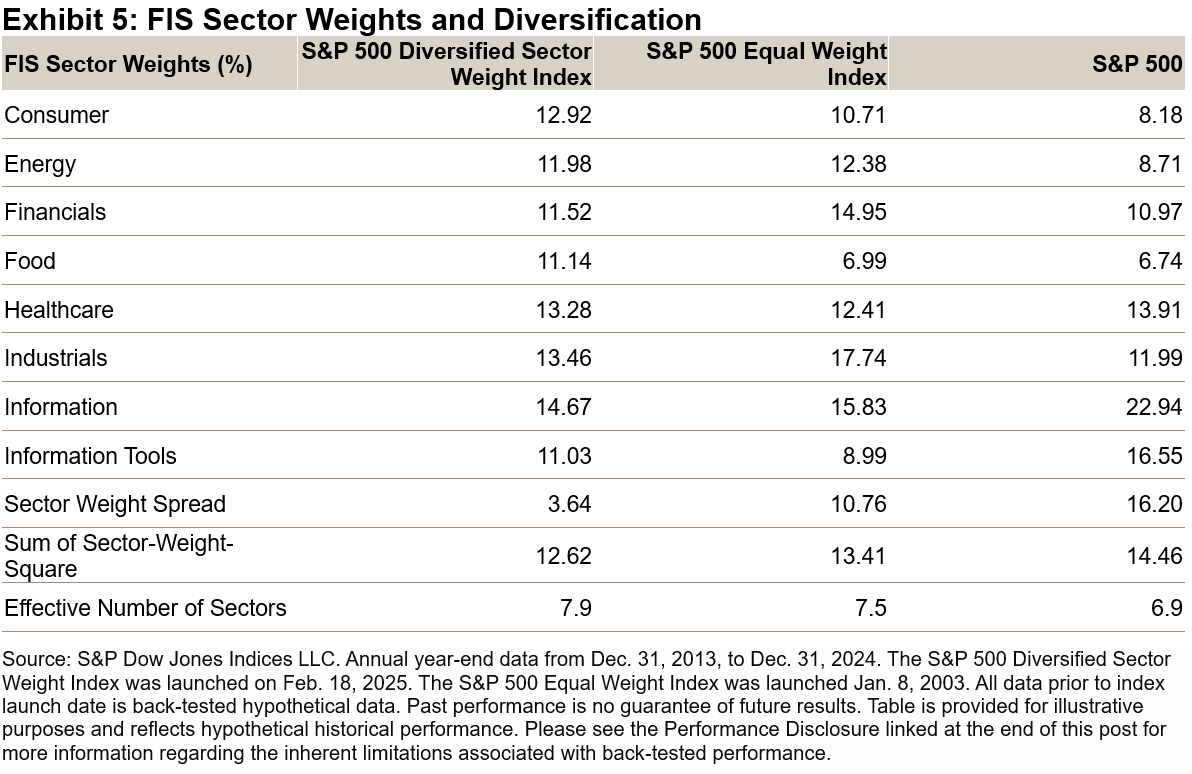

Exhibit 5 illustrates that the S&P 500 Diversified Sector Weight Index boasts the smallest sector weight spreads and a higher effective number of sectors3 compared to its counterparts.

Stock Level Diversification

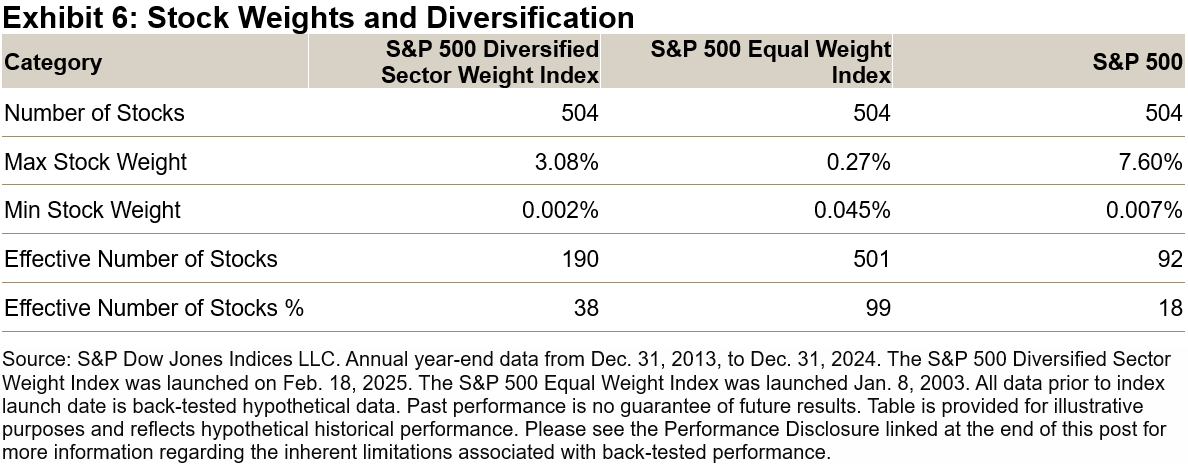

Although primarily designed to equalize sector weights and balance business risks, the S&P 500 Diversified Sector Weight Index has also historically reduced single-stock concentration. Compared to The 500, it maintained a higher effective number of stocks and featured lower maximum stock weights (see Exhibit 6).

Conclusion

The S&P 500 Diversified Sector Weight Index has had a more balanced representation of sectors and business risks within the S&P 500 universe. Furthermore, it has historically had lower single-stock concentration. Moreover, the S&P 500 Diversified Sector Weight Index has historically outperformed the S&P 500 Equal Weight Index.

1 Please refer to S&P 500 Diversified Sector Index methodology for more detailed info.

2 Within each Business Activity, each company is assigned a weight based on the product of (1) the weight of that Business Activity and (2) the trailing last 12 months’ revenue that the company derives from that Business Activity, divided by the sum of revenue that all companies derive from that Business Activity. If a company derives revenue from multiple Business Activities, a company’s final weight is the sum of the weights from each of the company’s Business Activities.

3 Effective number of sectors is defined as the inverse of the sum of squared sector weights for each index.

The posts on this blog are opinions, not advice. Please read our Disclaimers.