By weighting the constituents of the S&P 500® based on top-line revenue, the S&P 500 Revenue-Weighted Index offers an alternative to traditional benchmarks that are weighted by float market cap (FMC). This approach aims to better reflect the fundamental strength of each company, while offering better valuations and enhanced diversification. In this blog, we will analyze its methodology, examine short- and long-term performance, explore style tilts and assess diversification.

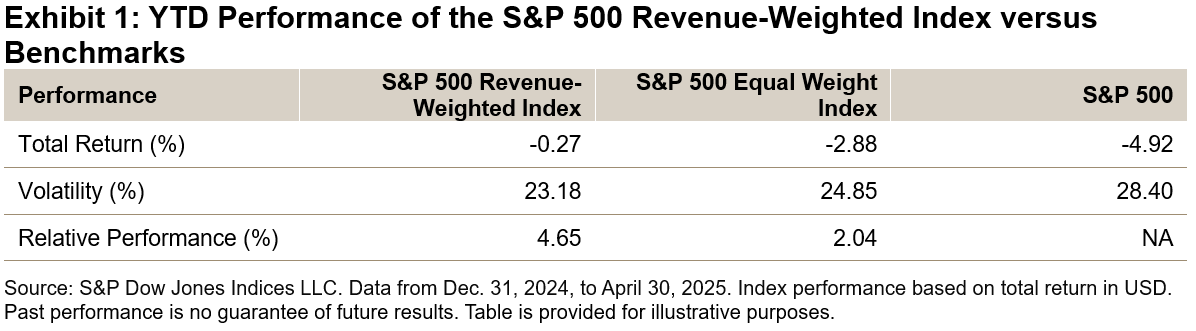

Year-to-Date Performance

So far this year, the S&P 500 Revenue-Weighted Index has outperformed The 500™ by more than 4.5% and surpassed the S&P 500 Equal Weight Index by more than 2.0% (see Exhibit 1).

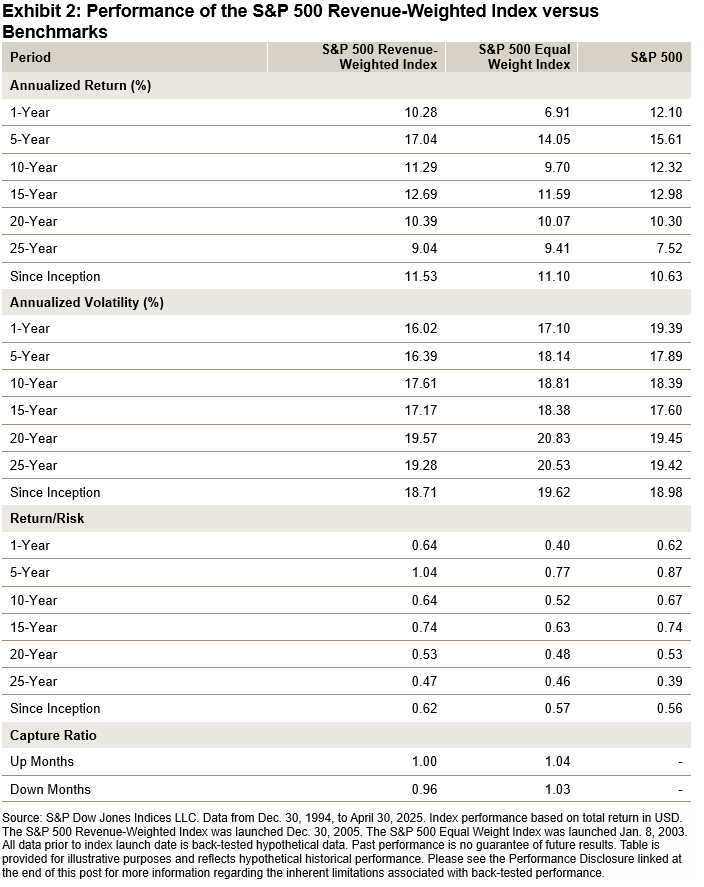

Long-Term Performance

This recent outperformance is consistent with its historical track record. As shown in Exhibit 2, the S&P 500 Revenue-Weighted Index has outperformed both the S&P 500 and S&P 500 Equal Weight Index in terms of total return and risk-adjusted return over the long term, all while maintaining consistently lower volatility.

Upside Participation and Downside Protection

The historical capture ratios (Exhibit 2) show that the S&P 500 Revenue-Weighted Index has typically participated one-for-one in up markets,1 while delivering significant outperformance during down markets. This aligns with the design of revenue-weighted indices, which tend to provide a closer reflection of the broader economy and avoid overweighting overvalued stocks.

Methodology

The S&P 500 Revenue-Weighted Index assigns weights to its constituents proportional to their revenues from the past four quarters. To provide broader coverage and reduce concentration risk, individual constituent weights are capped at 5%, and the index rebalances quarterly in March, June, September and December.

Weighting by revenue may better reflect the broader economy, as revenue is directly tied to economic activity. Additionally, revenue serves as a direct indicator of a company’s ability to generate income and is less susceptible to accounting manipulations.

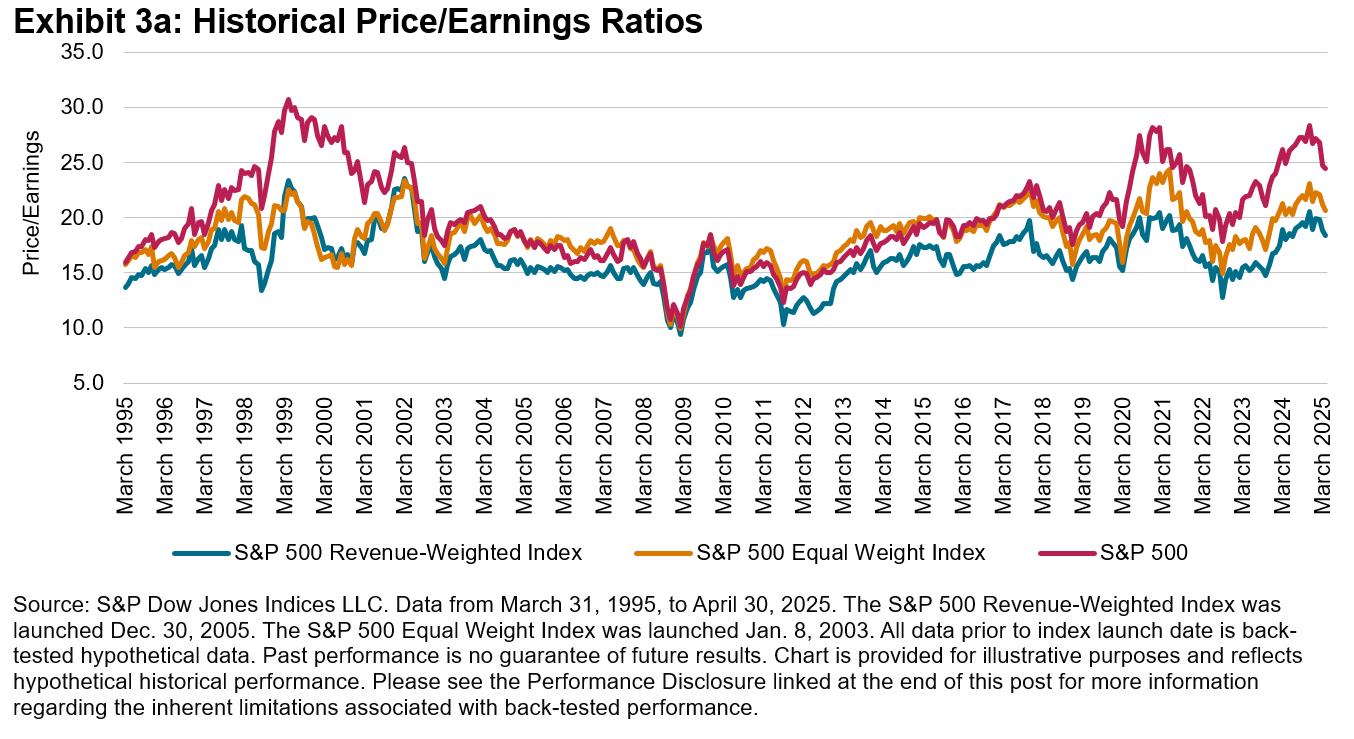

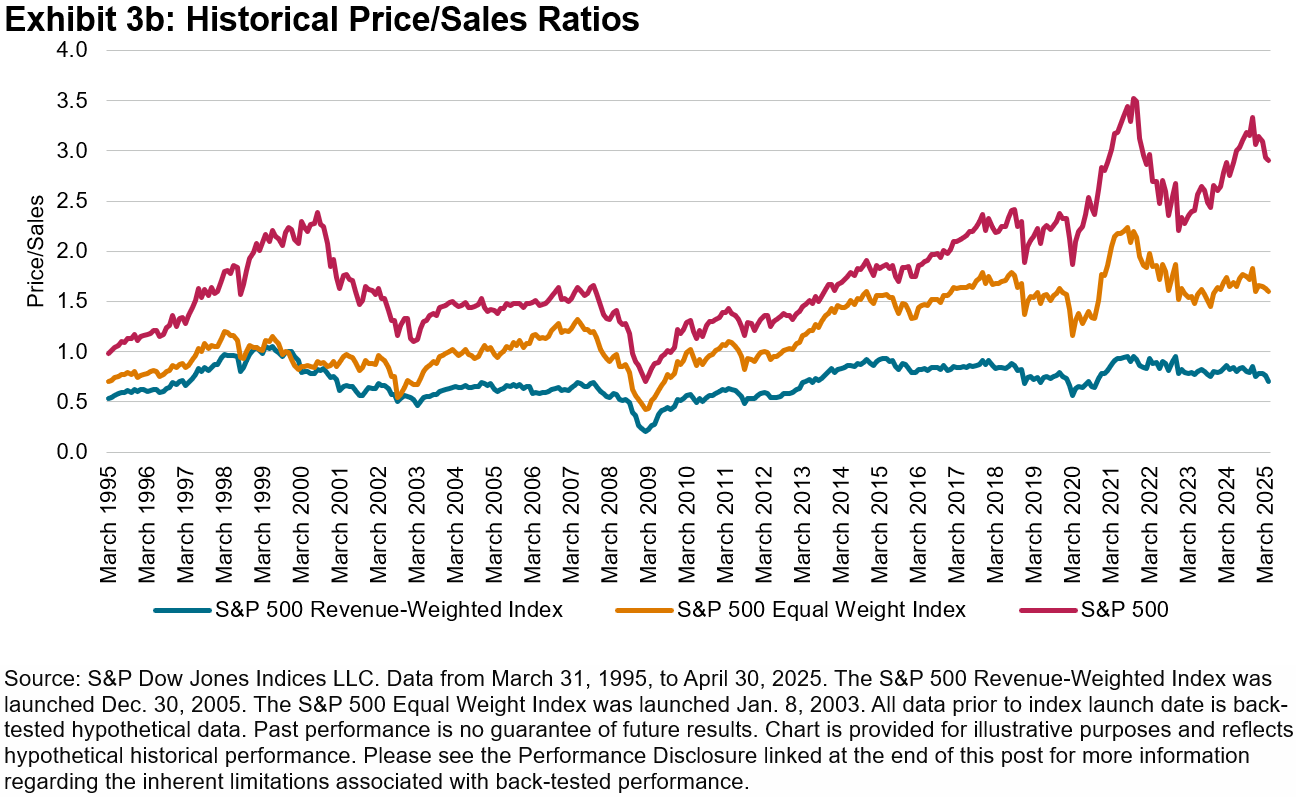

Valuations

As illustrated in Exhibits 3a and 3b, the S&P 500 Revenue-Weighted Index generally exhibited better valuations than the S&P 500 Equal Weighted Index and The 500.2

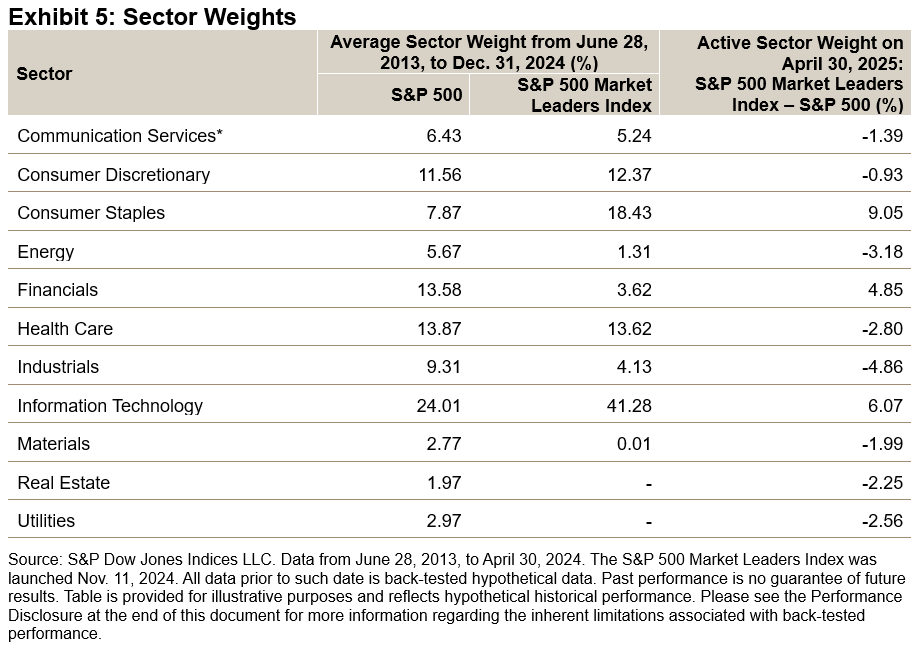

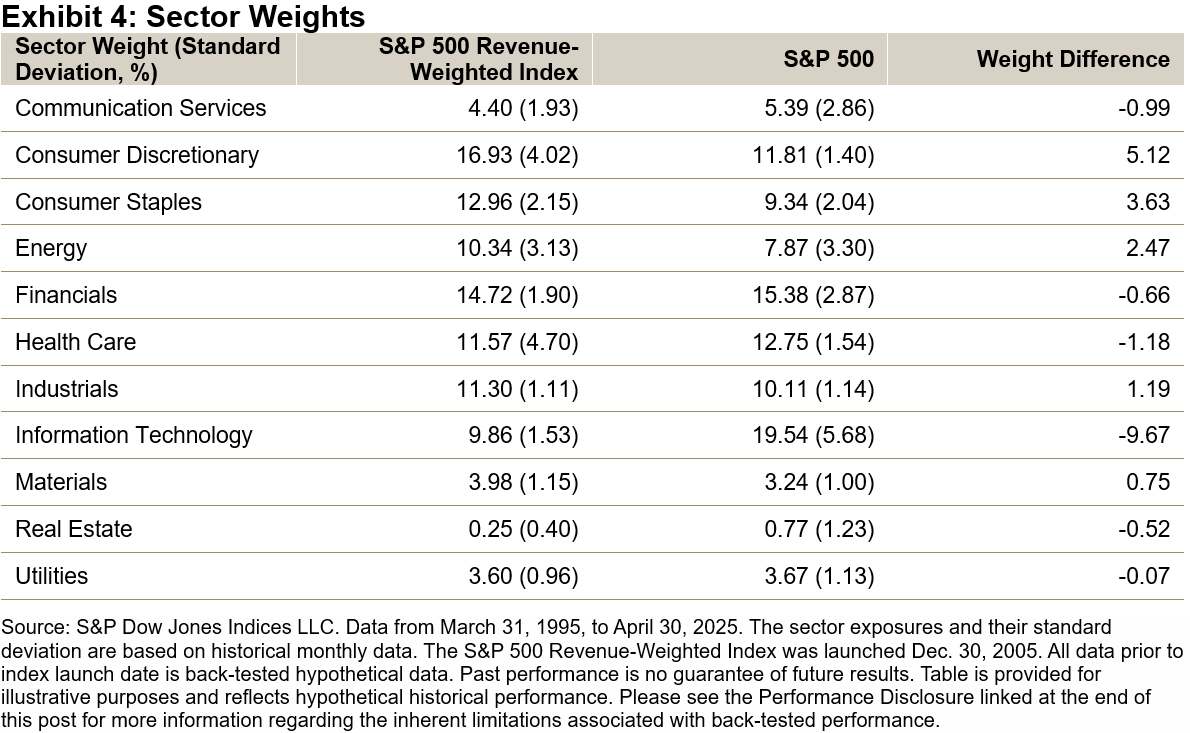

Sector Weights

As shown in Exhibit 4, revenue weighting has often resulted in more stable sector weights (as measured by lower standard deviation) compared to the weighting scheme driven by price, as revenues tend to be relatively stable. Moreover, the S&P 500 Revenue-Weighted Index held the largest weight in Consumer Discretionary, while Information Technology was the largest sector in The 500.

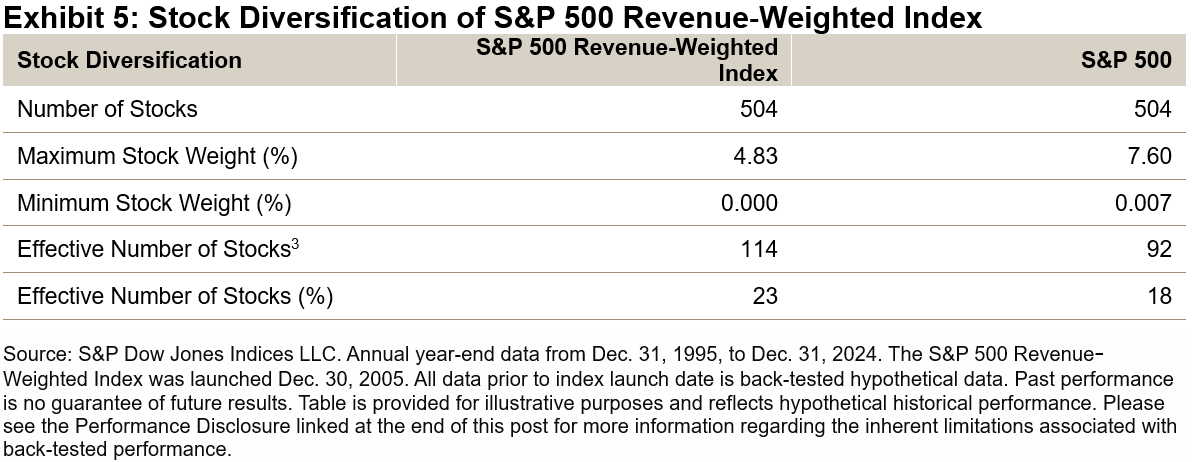

Diversification

When examining individual stocks, the S&P 500 Revenue-Weighted Index demonstrated greater diversification than The 500, featuring a lower max stock weight and a higher effective number of stocks (see Exhibit 5).

Conclusion

The S&P 500 Revenue-Weight Index presents an alternative to traditional market cap-weighted benchmarks, emphasizing fundamentally strong companies based on revenue. It has consistently delivered robust total returns and risk-adjusted outperformance over both the short and long term. In comparison to FMC-weighted benchmarks, it has historically offered greater value tilt, reduced concentration risk and more stable sector weights.

1 The market is defined as the monthly performance of the underlying benchmark (i.e., S&P 500) from Dec. 31, 1994, to March 31, 2025.

2 Historic price/book ratios show a similar trend to price/earnings and price/sales ratios.

3 Effective number of stocks is the inverse of the Herfindahl-Hirschman Index (HHI), which is the sum of squared stock weights for each index in each period.

The posts on this blog are opinions, not advice. Please read our Disclaimers.