Recent activities indicate that indexing is on the rise in wealth management.

A previous blog introduced Cerulli Associates’ new whitepaper, which explores how index-based strategies are reshaping U.S. wealth management.1 Financial advisors with at least 10% of client assets invested in exchange-traded funds (ETFs) are allocating 46% of client assets to index-based strategies today, with expectations that this figure could hit 49% by 2026.2

But what’s driving this shift? In this blog, we examine the strategic factors behind indexing’s rise—including changes in advisors’ value propositions, the growth of asset allocation models and the rising use of direct indexing.

A New Advisor Playbook: From Performance to Planning

The wealth management landscape is evolving. Research from Cerulli Associates shows advisors are pivoting away from investment management as their core differentiator, with financial planning now taking center stage.

Why have advisors’ value propositions shifted? The research shows that clients have turned their focus to goals—such as funding retirement or college—rather than beating benchmarks. For example, 57% of affluent investors prioritized advisors who understand their needs, while 45% aimed to outperform the market.3

This shift aligns with a rise in index-based strategies, which have lower fees—an attractive feature for advisors focusing on holistic planning over outperforming benchmarks.

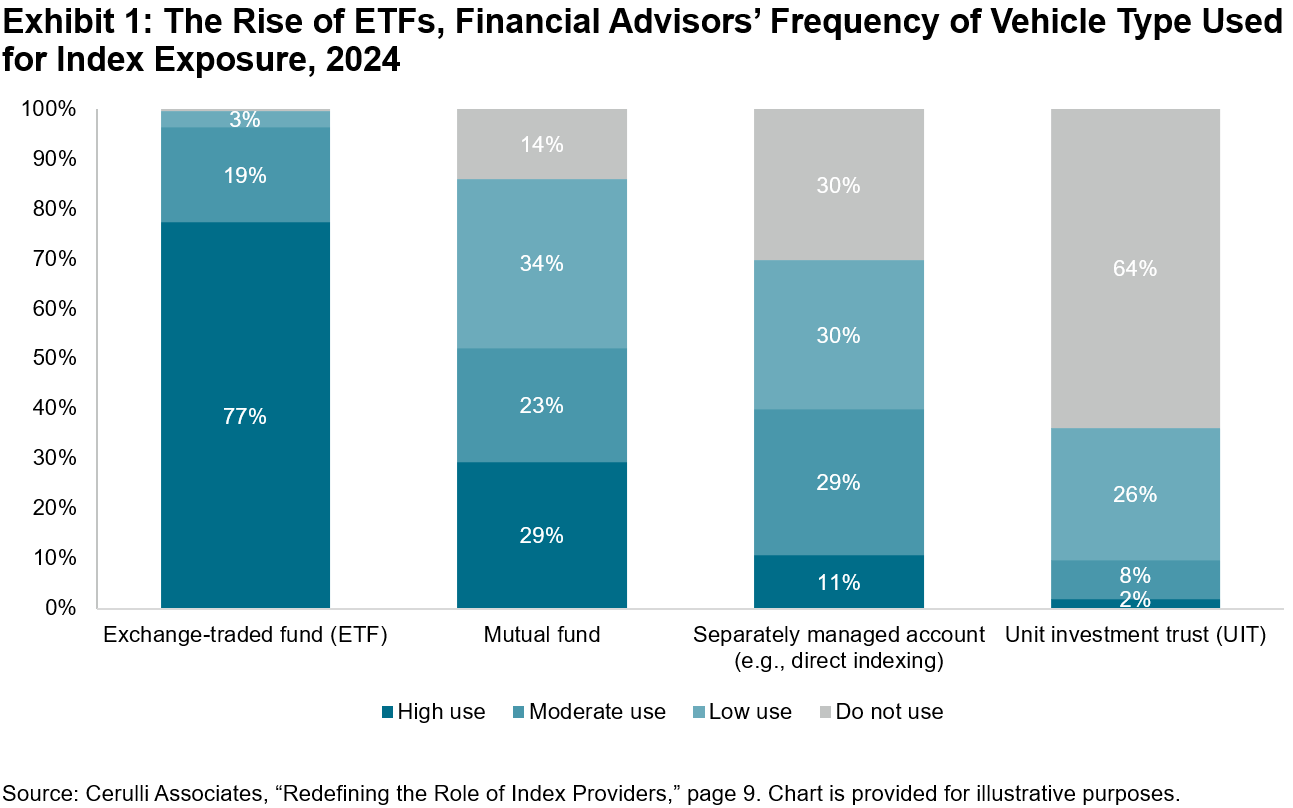

ETFs are the leading vehicles for index-based strategies, with over 75% of advisors reporting high usage, a factor contributing to indexing’s momentum (see Exhibit 1).

Asset Allocation Models: Outsourcing Meets Efficiency

Hand in hand with this trend is the rise of asset allocation model portfolios. These outsourced solutions, often built with index-based ETFs, are increasingly popular. Cerulli Associates pegged model assets at USD 2.1 trillion in 2023, projected to hit USD 2.9 trillion by year-end 2025.4

The growing use of asset allocation model portfolios is supported by a constant push/pull dynamic: wealth management home offices are actively promoting their adoption among advisors, while advisors themselves are increasingly attracted to the benefits these portfolios offer. For home offices, model portfolios can help create a more consistent client experience, reduce compliance risks and streamline decision-making, while advisors are drawn to the increased efficiency they offer, freeing up time for client-facing work.

Direct Indexing: Precision Meets Personalization

Direct indexing is becoming an important vehicle for how advisors build portfolios at the nexus of two trends in wealth management: high-net-worth clients’ demand for both increased efficiency and greater personalization.5

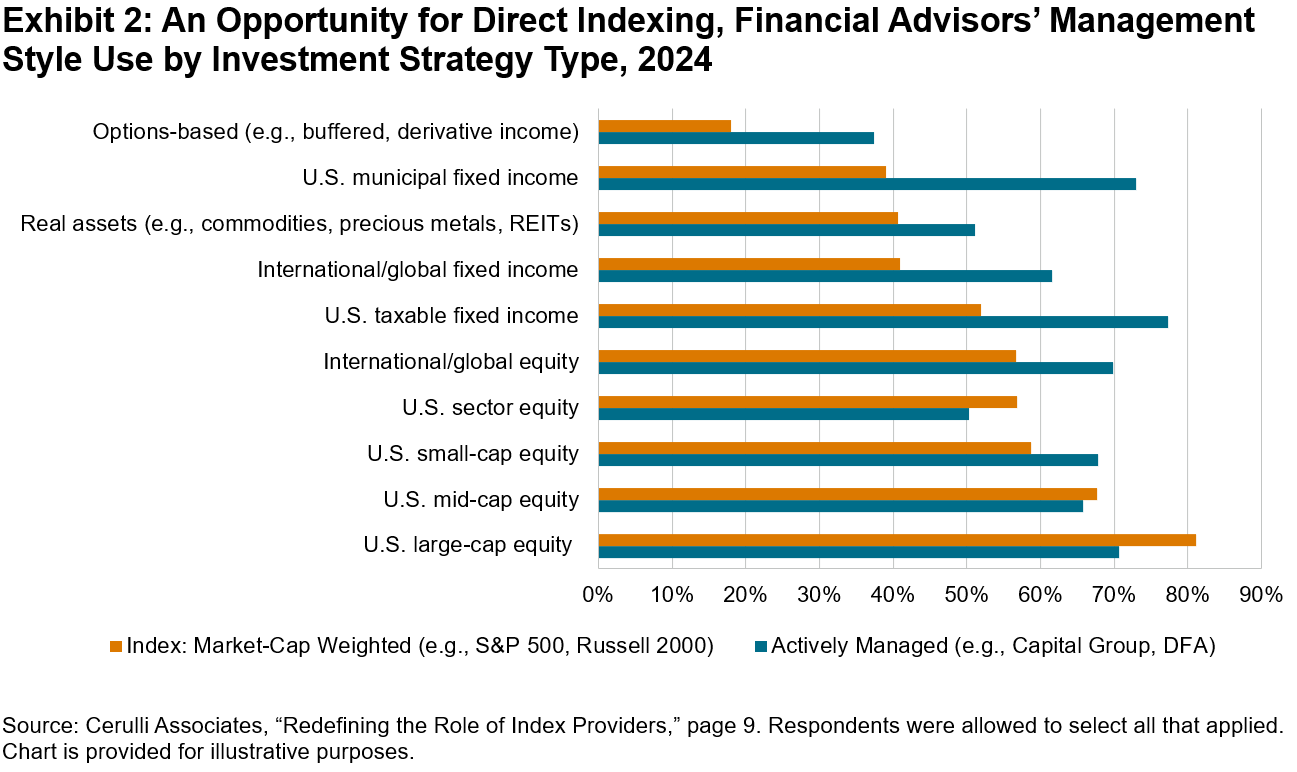

Advisors are increasingly using separately managed accounts (SMAs) to track indices while customizing for tax optimization or client preferences. Cerulli Associates has a positive outlook on the potential growth of direct indexing among the affluent and high-net-worth client segments, particularly in equity-based strategies. One reason is that 81% of advisors use index-based strategies for U.S. large-cap equity, where efficiency is prioritized, versus 52% for taxable fixed income, where active approaches are still implemented (see Exhibit 2).6

What’s Next?

These factors—planning over performance, model portfolios and direct indexing—aren’t just trends; they are fundamentally reshaping how advisors operate. Index providers have a role in these mega-trends, as they deliver the data, intellectual property and other tools designed to help asset managers and wealth managers track markets with precision and efficiency.

In upcoming blogs, we will explore how asset managers and wealth managers may further implement index providers’ solutions and services.

1 The Cerulli Associates whitepaper “Redefining the Role of Index Providers” was sponsored by S&P Dow Jones Indices.

2 Please see Executive Summary of Cerulli Associates’ “Redefining the Role of Index Providers.”

3 Please see page 4 of Cerulli Associates’ “Redefining the Role of Index Providers.”

4 Please see page 8 of Cerulli Associates’ “Redefining the Role of Index Providers.”

5 For more information on the growth of direct indexing, please read “Harnessing the Power of Direct Indexing.”

6 Please see page 10 of Cerulli Associates’ “Redefining the Role of Index Providers.”

The posts on this blog are opinions, not advice. Please read our Disclaimers.