The S&P 500® recently entered a “correction,” a term used when the price index falls by more than 10% from its highs. It may yet decline further, the fact of which might tempt market participants to delay equity purchases until, say, the index has declined by 20%—which would define the start of a “bear market.” The potential relative merits of “waiting for a discount,” as examined historically via the nearly seven-decade-long record of the S&P 500, offer an intriguing perspective.

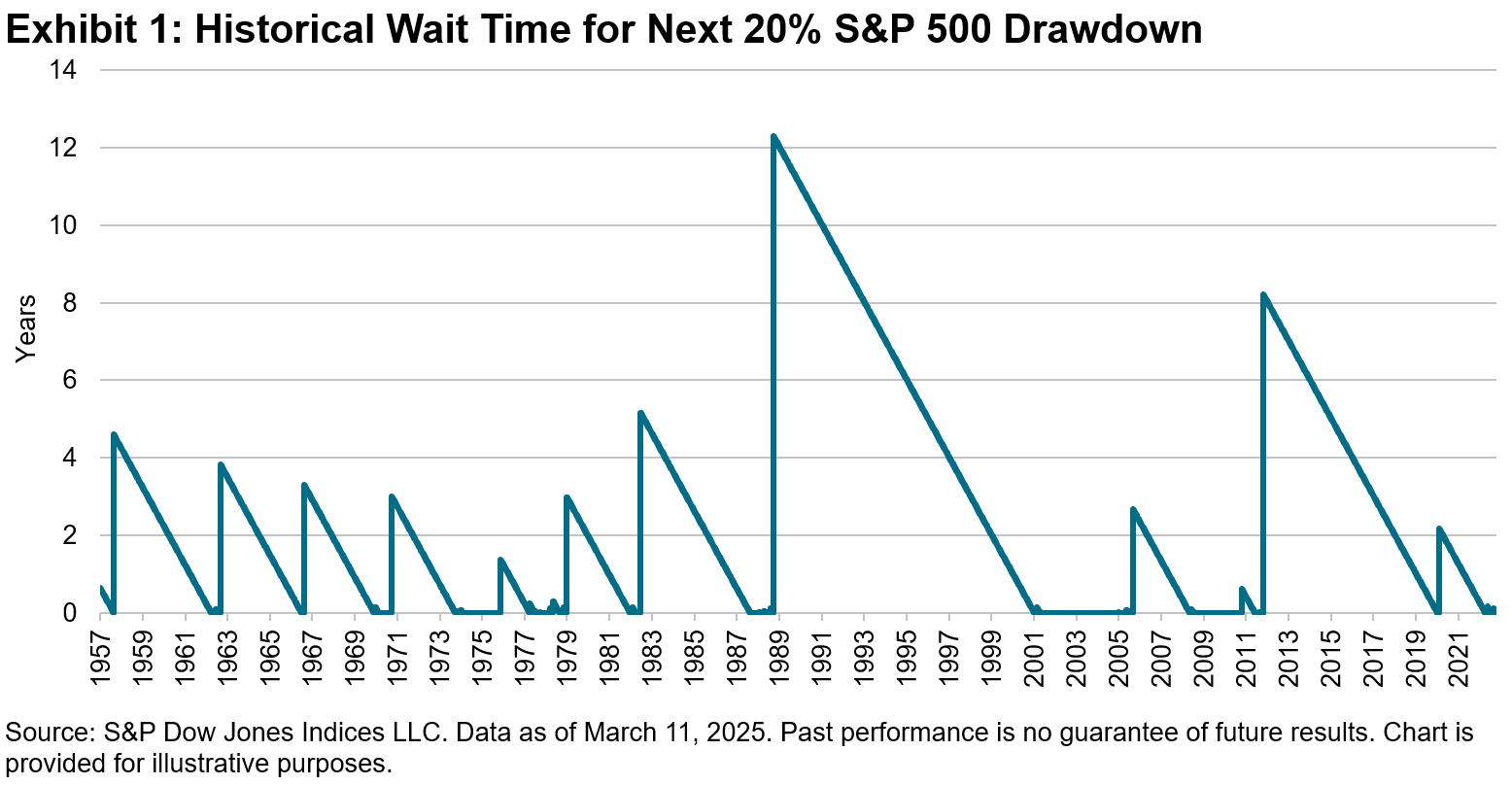

We began with every trading day in The 500™’s history on which the closing index level was not already 20% or more below the prior all-time high. For such days, we then measured how long it was before a 20% decline first occurred and what the overall change in the index level was over that period. Exhibit 1 shows the length of time in years of such waiting periods, historically.

The average waiting time was 3.0 years, while among the smaller sample of days when the index was already 10% or more down from a high (but not yet 20% down), the wait for a bear market was almost as long—equal to 2.1 years.

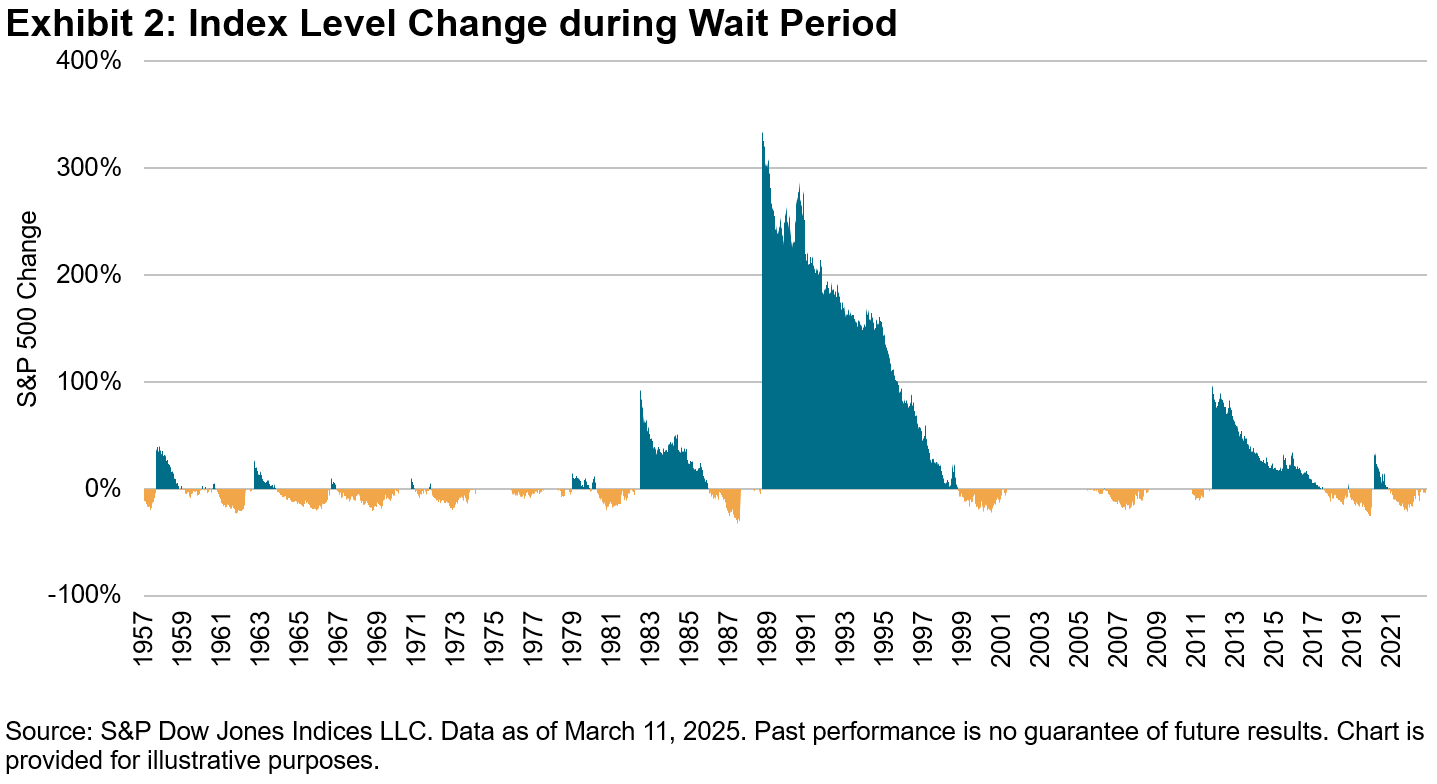

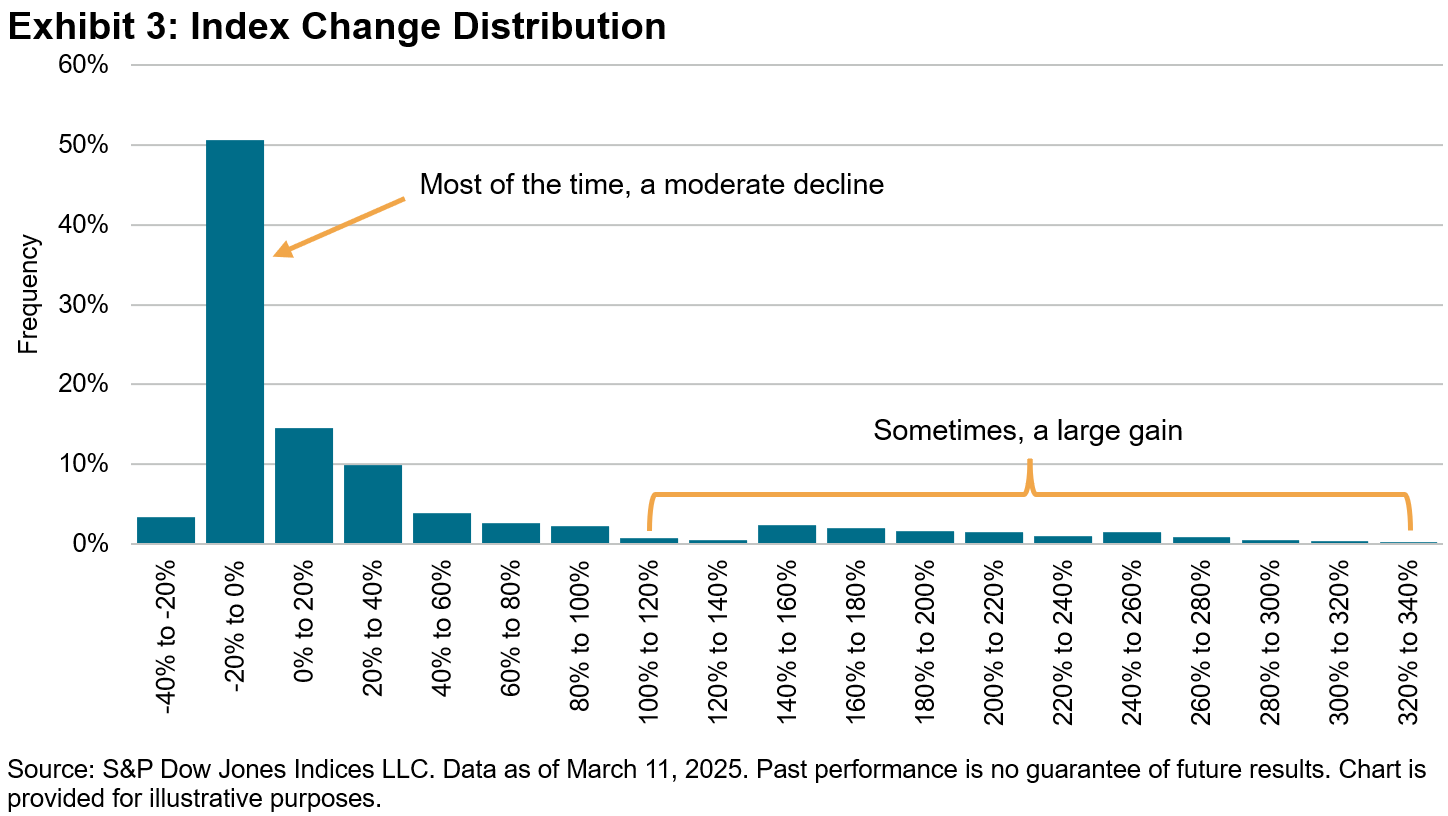

Sometimes, the index rose more than enough to offset the subsequent decline. At the historical extreme: from Nov. 29, 1988, it was over 12 years until the next bear market began, by which time the index had risen a cumulative 336% (including the final decline). Exhibit 2 shows the change in the index level during the waiting period associated with each starting point in history, and Exhibit 3 shows the accompanying distribution of those index changes, ignoring zero values.

Most of the time, waiting meant a slightly lower index level—the median index change was a decline of 1.7%. However, some of the time, the index change was highly positive, which led to an average index change equal to a 30.0% increase. Restricting to the days when the index was down 10% or more, but not yet 20% down, the average index change during the wait was, again, almost as material, equal to a 22% increase.

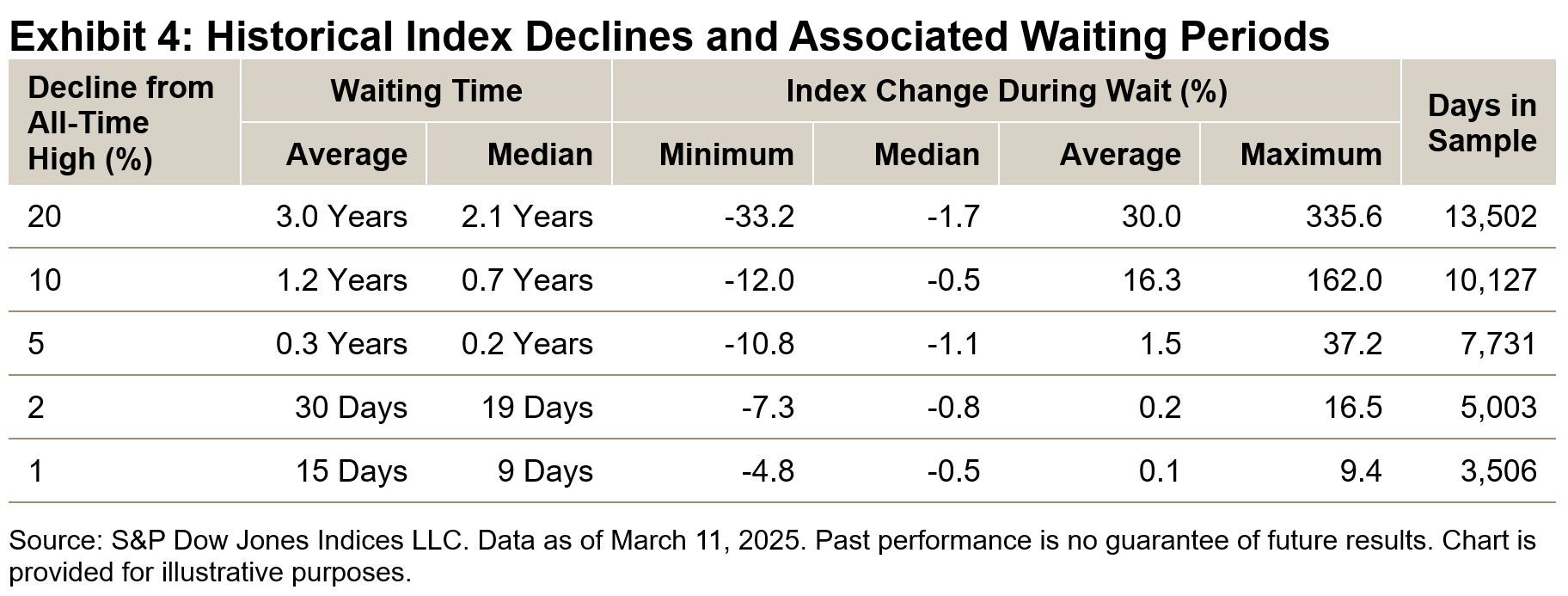

Exhibit 4 shows equivalent statistics using declines of 1%, 2%, 5%, 10%, as well as the original 20%. The sample size of “start points” get smaller down the table, as the proportion of days when the index was already in such a decline increases.

Overall, the pattern was similar for smaller declines: the median index change during the wait for a discount was a small decrease, but the average index change was positive, and the maximum index change was much higher. In other words, most of the time, waiting resulted in a small discount. But some of the time, waiting meant missing out on large gains.

The well-known money manager Peter Lynch once quipped that “Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.” That may be true. As to whether the current S&P 500 downturn represents a buying opportunity, of course, only time will tell.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

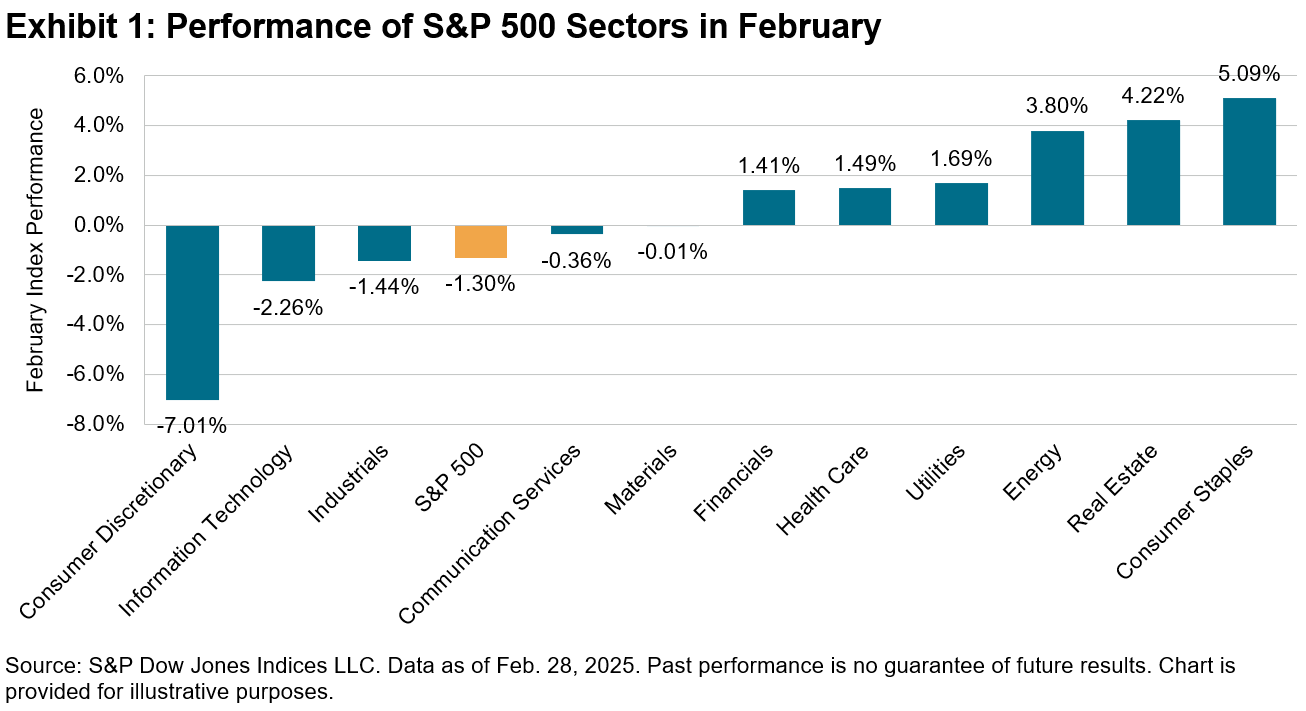

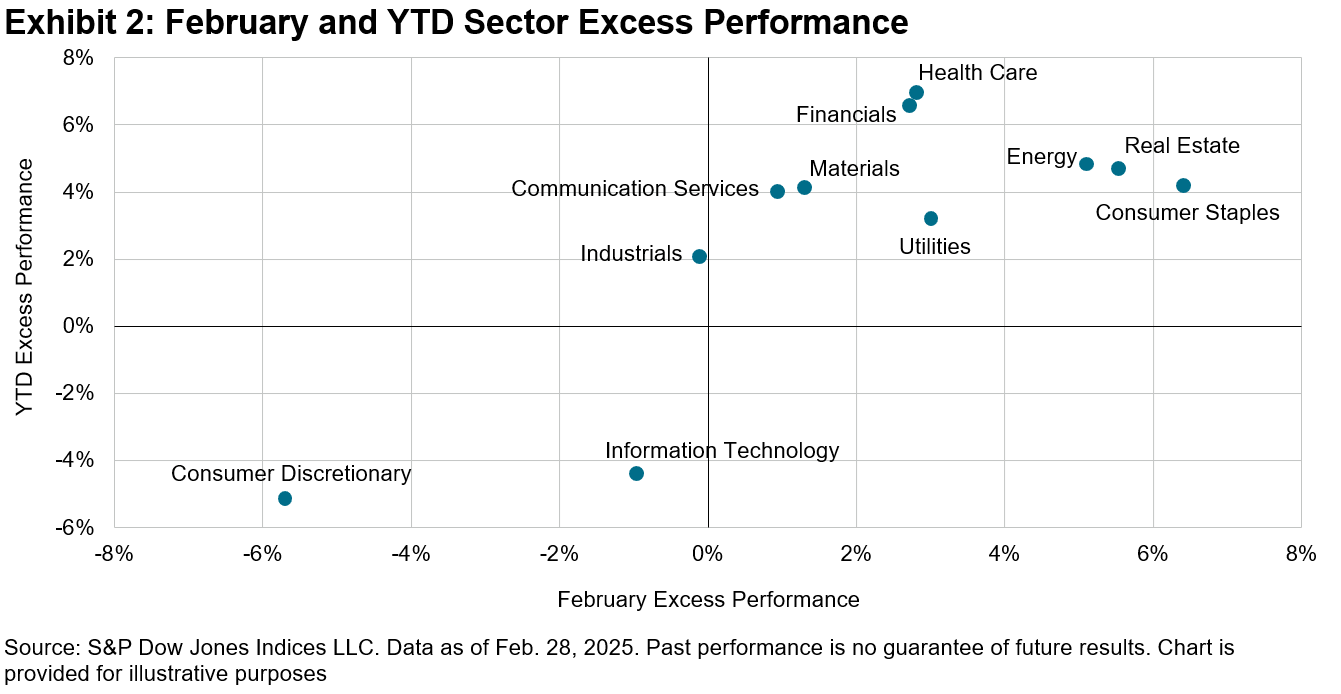

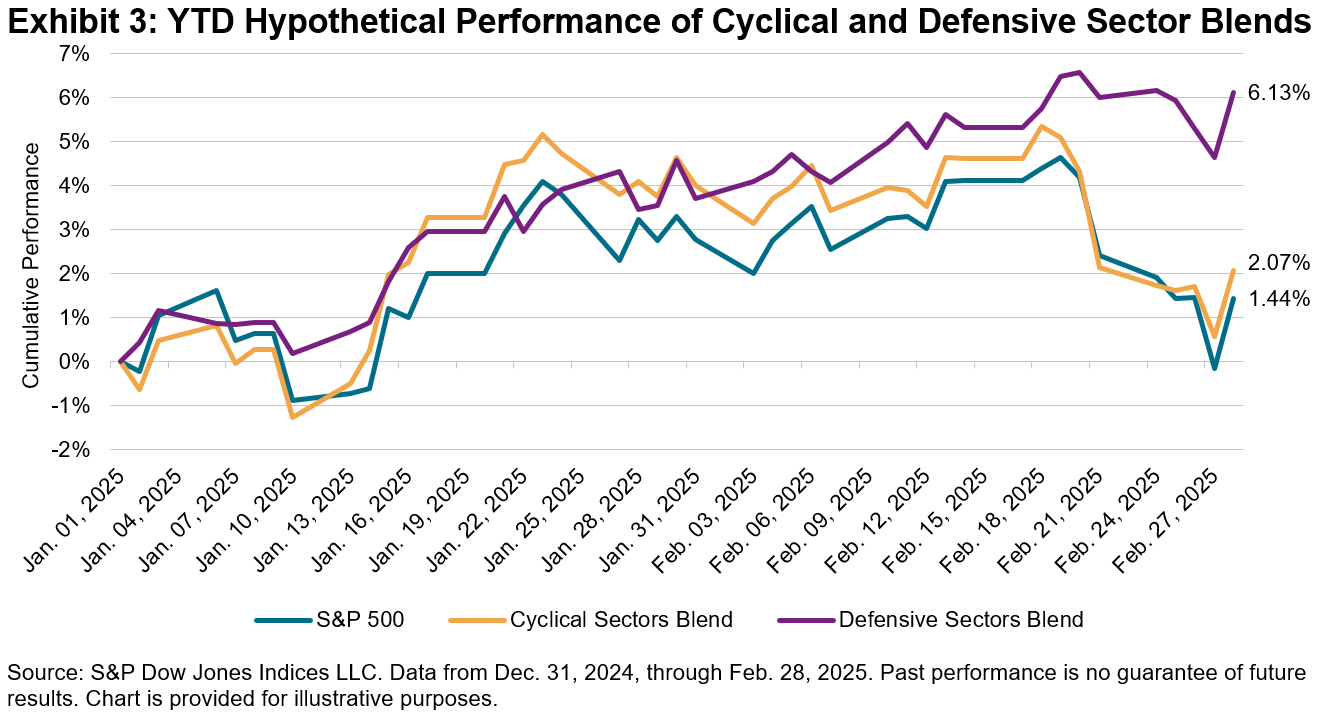

Headwinds and tailwinds affecting each sector in January generally persisted in February, as Consumer Discretionary and Information Technology extended their previous month’s underperformance, while eight other sectors outperformed The 500 in February, and nine sectors surpassed the broad benchmark YTD (see Exhibit 2). Industrials was the only sector that trailed slightly in February yet maintained excess performance YTD.

Headwinds and tailwinds affecting each sector in January generally persisted in February, as Consumer Discretionary and Information Technology extended their previous month’s underperformance, while eight other sectors outperformed The 500 in February, and nine sectors surpassed the broad benchmark YTD (see Exhibit 2). Industrials was the only sector that trailed slightly in February yet maintained excess performance YTD. In a

In a  Although two months of 2025 are in the rearview mirror and, in many ways, the road ahead remains unclear, the performance of S&P 500 sectors sheds some light on how investors view prospects for different segments of the economy and provides a useful framework for making thoughtful tilts in preparation for whatever comes next.

Although two months of 2025 are in the rearview mirror and, in many ways, the road ahead remains unclear, the performance of S&P 500 sectors sheds some light on how investors view prospects for different segments of the economy and provides a useful framework for making thoughtful tilts in preparation for whatever comes next.