The financial services consulting firm, Cerulli Associates, recently published a research study on the use of index-based products within the U.S. retail wealth management market. Their whitepaper aims to shed light on how asset managers, asset allocation model portfolio providers, wealth manager home offices and financial advisors can better utilize index provider solutions.1

The study is the culmination of 293 financial advisor survey results, which are diversified across channel, practice assets under management (AUM), core market client size and advisor age. It excludes advisors with less than USD 50 million in AUM and those with more than 25% in institutional assets or defined contribution plans. The paper also aggregates the findings of 25 executive interviews with asset managers, technology providers, wealth manager home offices and individual financial advisors.

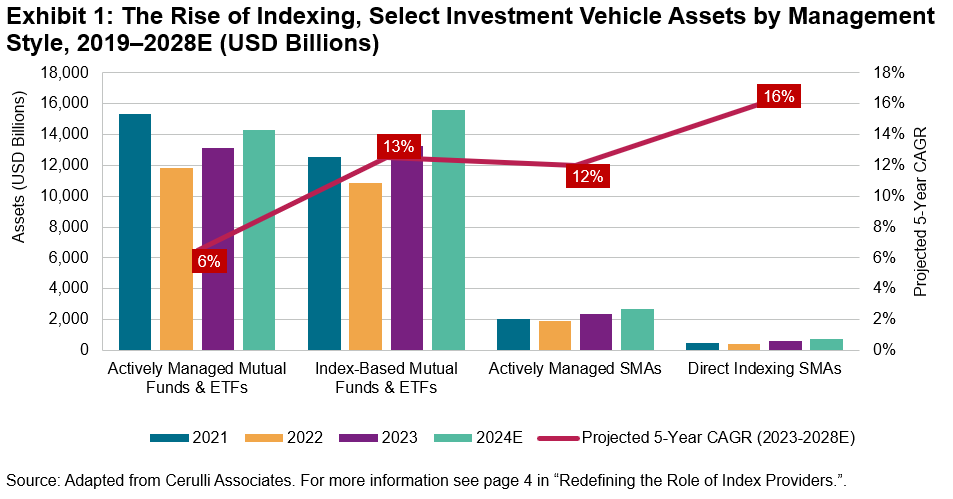

According to the research, the U.S. wealth management industry is experiencing a shift in value proposition where end-investors are increasingly relying on their financial advisor for their financial planning expertise rather than their investment management acumen. When asked to identify which factors are most important when selecting an advisor, 57% of affluent (i.e., USD 100,000 or more in investable assets) clients indicated that an advisor who takes the time to understand their needs and goals is extremely important, while only 45% said the same about the performance of their investments relative to the overall market.2 Fund flow data supports this shift as the positive growth of index-based exchange-traded funds (ETFs) and mutual funds, as well as direct indexing separately managed accounts (SMAs), have outpaced their actively managed counterparts, a trend that is projected to continue through 2028 (see Exhibit 1).

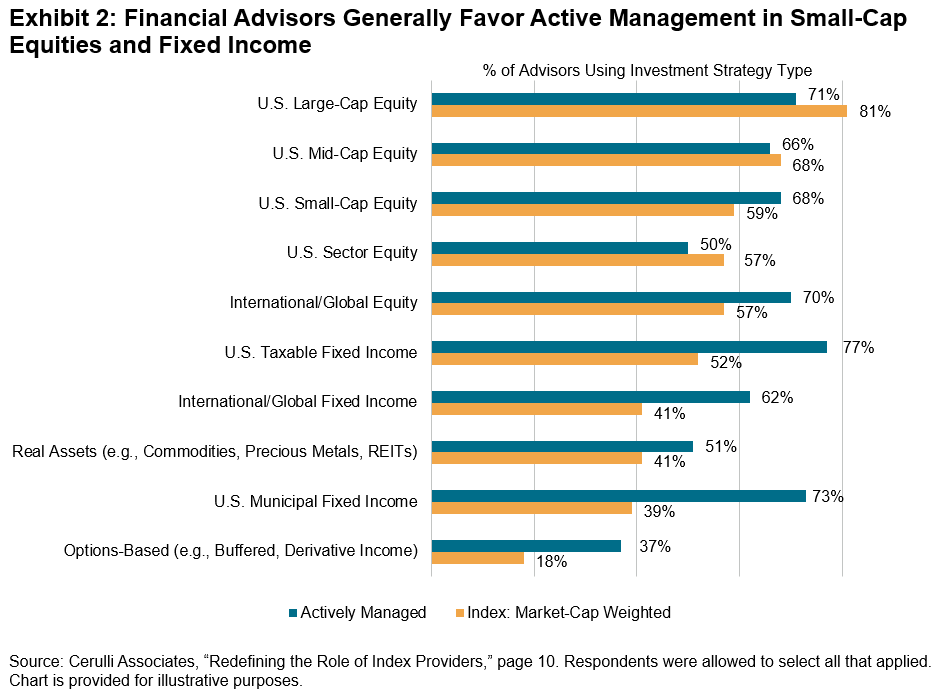

Although Cerulli Associates forecasts increased usage of index-based strategies, Exhibit 2 indicates that advisors currently pursue an active approach in sub-asset classes they perceive as being less informationally efficient, such as small-cap equities, international fixed income, U.S. taxable and municipal fixed income, options-based assets and real assets. However, a future shift could be in the cards. Cerulli Associates’ research suggests that financial advisors could expand their usage of index-based products beyond equities to fixed income as well,3 paralleling the growth of indexing in fixed income.4

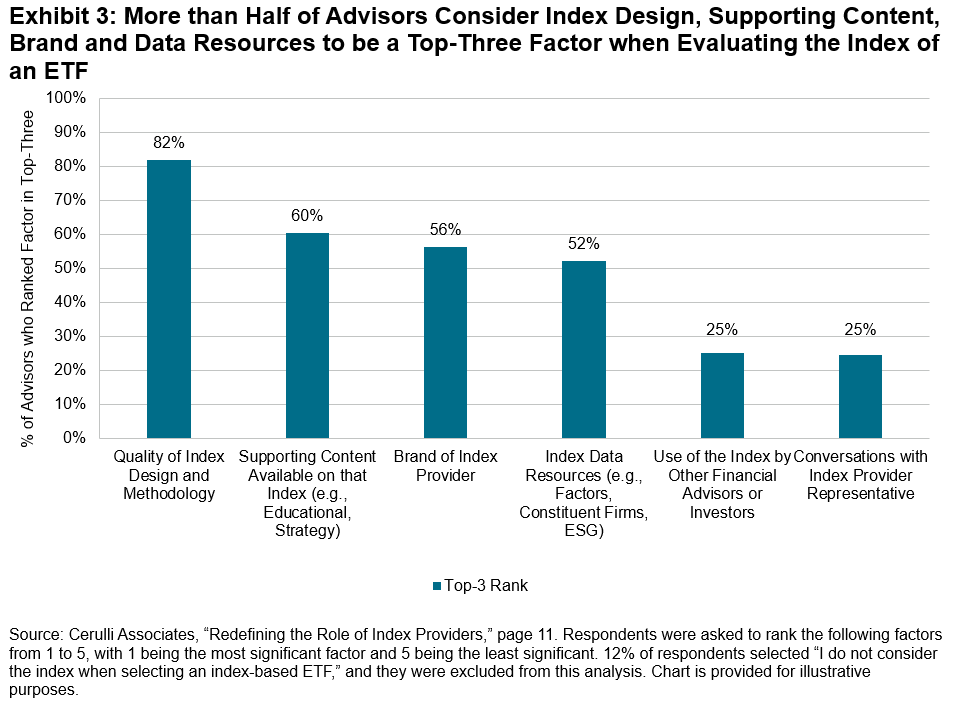

In addition to surveying advisors on how they utilize index-based products, they also extracted insights on how they evaluate them. For example, Exhibit 3 shows that 82% of advisors indicated that the quality of the index design and methodology was a top-three factor when considering the index that underlies an ETF, and 60% of advisors said the same of index provider content and education. To learn more about how financial advisors think about index providers, Cerulli Associates created a series of advisor profiles located in the appendix of the whitepaper.

As the landscape of index-based products becomes increasingly crowded, the recent findings from Cerulli Associates highlight that asset and wealth managers should thoughtfully consider how to leverage index providers’ solutions to stand out from the crowd.5 Strategies include going beyond traditional index data to drive product development and leveraging brand and content for product marketing and distribution. Embracing these strategies can not only differentiate firms but may also position them for success in the evolving retail wealth management market.

1 The Cerulli Associates whitepaper “Redefining the Role of Index Providers” was sponsored by S&P Dow Jones Indices.

2 Please see page 4 of Cerulli Associates’ “Redefining the Role of Index Providers”.

3 Please see page 10 and 11 of Cerulli Associates’ “Redefining the Role of Index Providers” for more information on ETF product growth.

4 For more information on the growth of indexing in fixed income, please read “The Hare and The Tortoise – Assessing Passive’s Potential in Bonds”.

5 Please see section 4, pages 12-17 of Cerulli Associates’ “Redefining the Role of Index Providers” for more information.

The posts on this blog are opinions, not advice. Please read our Disclaimers.