The S&P 500® Momentum Index has been one of the best-performing of all the S&P 500 Factor Indices in the past few years. A closer inspection of the drivers of performance identifies constituent selection as paramount, highlighting the importance of dynamically retreating from the largest of the mega caps in periods when smaller names took the lead.

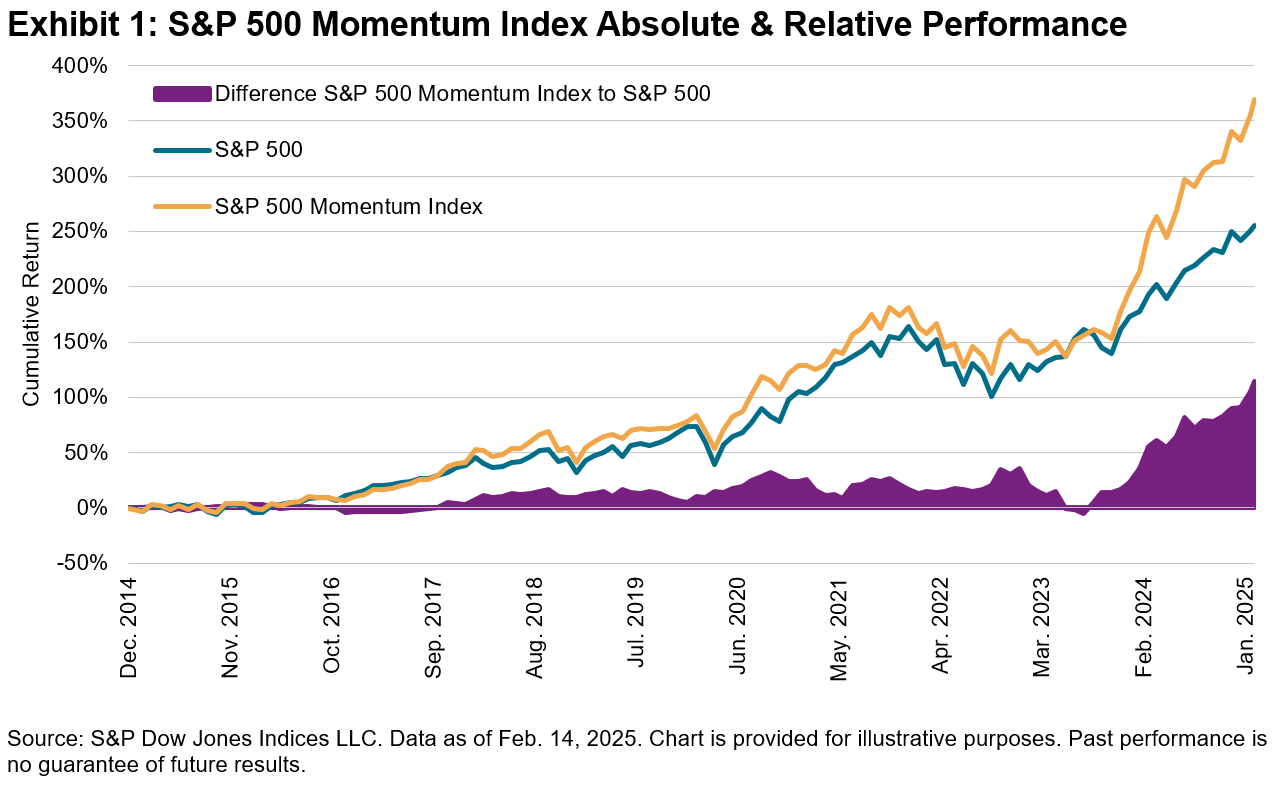

Launched just over a decade ago, the index tracks the performance of the 100 securities within the S&P 500 that exhibit the greatest persistence in their relative performance.1 Exhibit 1 shows the cumulative total return of the index since its launch in comparison to The 500™, as well as the cumulative difference. The S&P 500 Momentum Index has performed particularly well in recent years; the index concluded 2024 on a high note, surpassing The 500 by an impressive 21% over the year to reach a cumulative lifetime excess return of 98.6%.

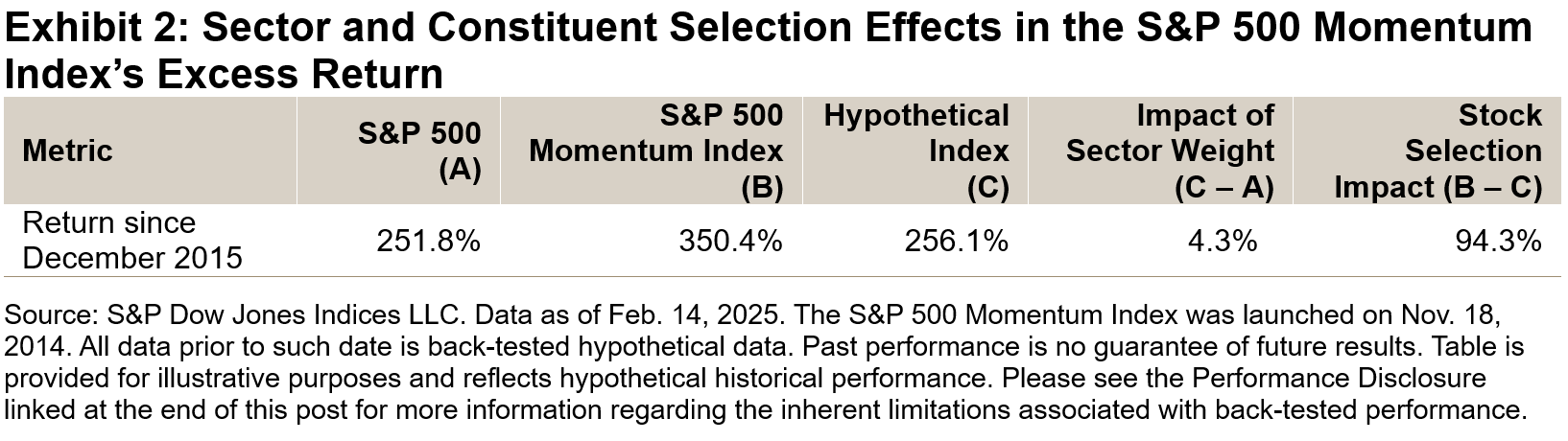

So, what drove such strong performance? Exhibit 2 examines the relative impact of the sector over- and under-weights maintained by the S&P 500 Momentum Index over its history. More specifically, Exhibit 2 compares three return streams: the S&P 500, the S&P 500 Momentum Index and a hypothetical index composed on a monthly basis from S&P 500 sector indices, weighted in the same proportions as the S&P 500 Momentum Index’s sectors. The difference between the first and third indices illustrates the impact of the S&P 500 Momentum Index’s sector weights, while the difference between the second and third indices shows how important stock selection was compared with just sector weights. The analysis shows that there was only a 4.3% difference between The 500 and the hypothetical index, meaning that only marginal excess performance came from sector weights, while nearly 95% of the excess return was driven by constituent selection.2

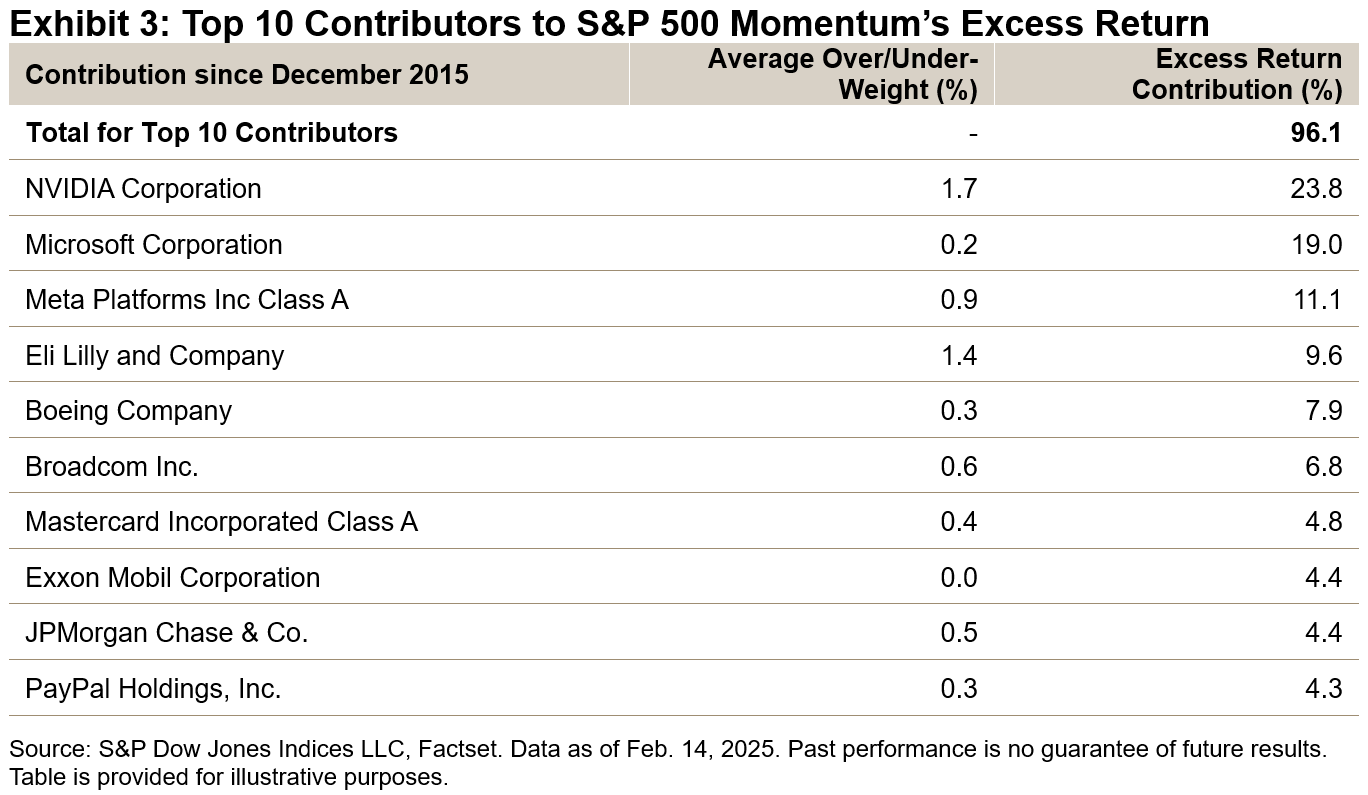

Drilling down into the particular constituent selections that aided or hindered relative performance over the 10-year period, there was a high degree of concentration in the relative contributions. In fact, the majority of the excess return came from just 10 companies. Exhibit 3 shows constituents that had the highest contribution to the S&P 500 Momentum Index’s excess return performance and indicates whether the index under or overweighted these stocks (on average).

A cursory glance at the names in Exhibit 3 identifies some familiar names, especially to those who have been following (and perhaps worrying about) the increasing dominance of the so-called Magnificent Seven; Nvidia, Microsoft and Meta were among the most significant contributors to excess returns.

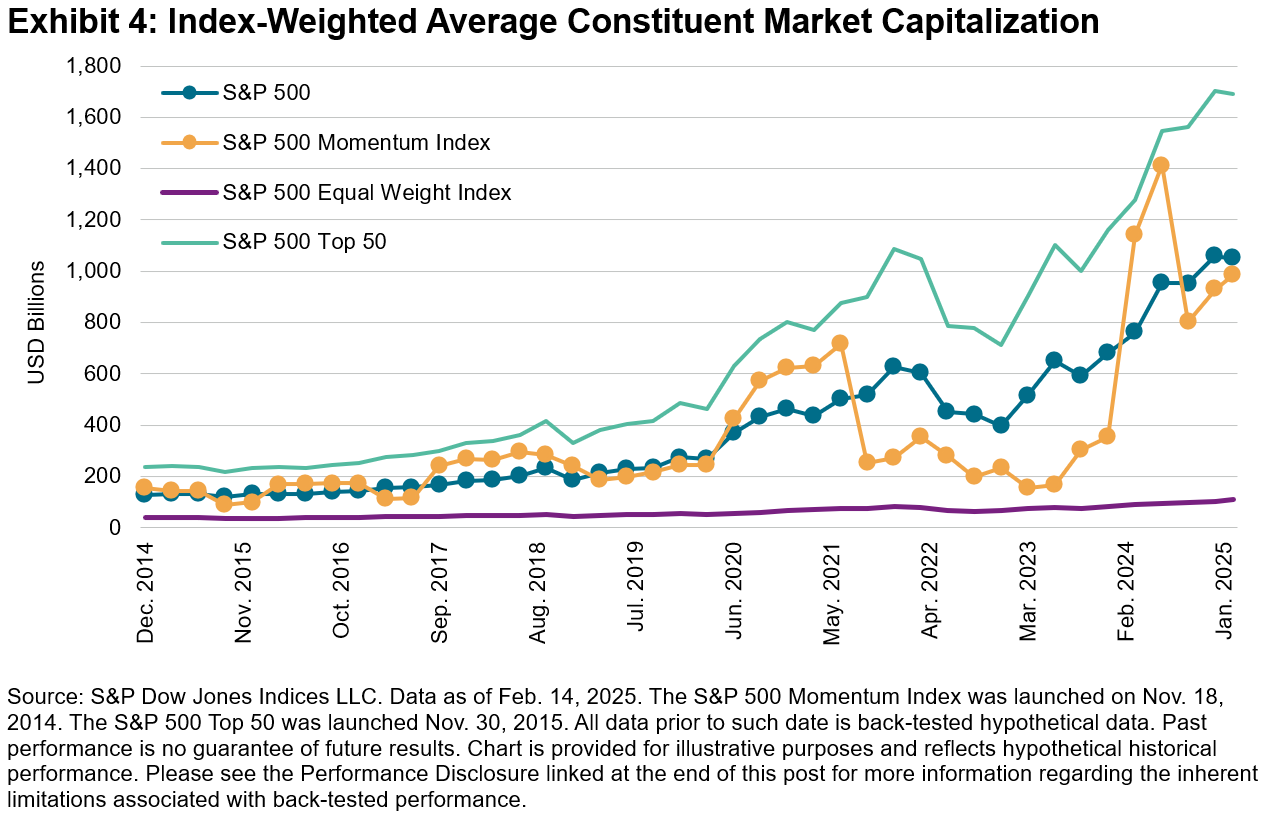

But was the S&P 500 Momentum Index simply riding a multi-decade trend for outperformance in the largest of large caps, and if so, what might happen if those large caps fall out of favor? As a reminder, the index undergoes rebalancing twice a year, in March and September, which can change the constituent selection and their weights. Exhibit 4 shows the index-weighted average market capitalization (a measure of how “big,” on average, the companies in the index were) of the S&P 500 Momentum Index and The 500 as well as the S&P 500 Top 50 and the S&P 500 Equal Weight Index, for purposes of comparison.

The dynamic nature of the S&P 500 Momentum Index reveals that the index sometimes overweighted the largest constituents, while at other times, it did not. As of the latest data, the S&P 500 Momentum Index was slightly tilted, overall, toward smaller companies than its benchmark. The S&P 500 Momentum Index’s future performance will continue to be driven by the mechanics of its methodology and the qualities of its constituents.

Keep track of our monthly Factor Dashboard for more detailed stats on Momentum and other factors.

1 More precisely, the index rebalances twice a year to comprise the top 100 stocks in the S&P 500 based their trailing 12 months risk-adjusted performance, weighted in inverse proportion to their volatility. The weighting is subject to single stock and sector constraints, and the risk and return of each constituent is measured with a lag. A full methodology is available here

2 A formal “Brinson” attribution confirms the simpler approach used here, with 98.64% of return attributed to stock selection.

What’s driving S&P 500 Momentum performance? S&P DJI’s Dasha Selivanova discusses the important role constituent selection has played in Momentum’s performance run in this episode of The Market Measure.

The posts on this blog are opinions, not advice. Please read our Disclaimers.