S&P 500 Quality, Value & Momentum Multi-Factor Index

Multi-factor strategies offer a comprehensive approach to index-based investing by combining diverse factors that exhibit low correlations across different market environments. By integrating these factors, multi-factor indices have historically shown lower volatility and better performance, while avoiding the need to time individual factors to align with specific economic trends or market phases.

A notable example is the S&P 500® Quality, Value & Momentum (QVM) Multi-Factor Index, launched on Jan. 30, 2017, which has demonstrated notable performance. In this blog, we will explore the index’s methodology and examine its characteristics, risk/return profile and performance attribution.

Methodology Overview

The S&P 500 QVM Multi-Factor Index tracks 100 stocks from the S&P 500 that exhibit the strongest combination of quality, value and momentum. Utilizing a bottom-up approach, the index selects “all-rounders” that have the highest scores, on average, across all three factors. The S&P 500 QVM Multi-Factor Index aims to provide a richer multi-factor exposure and help address the factor dilution often seen in top-down approaches.1

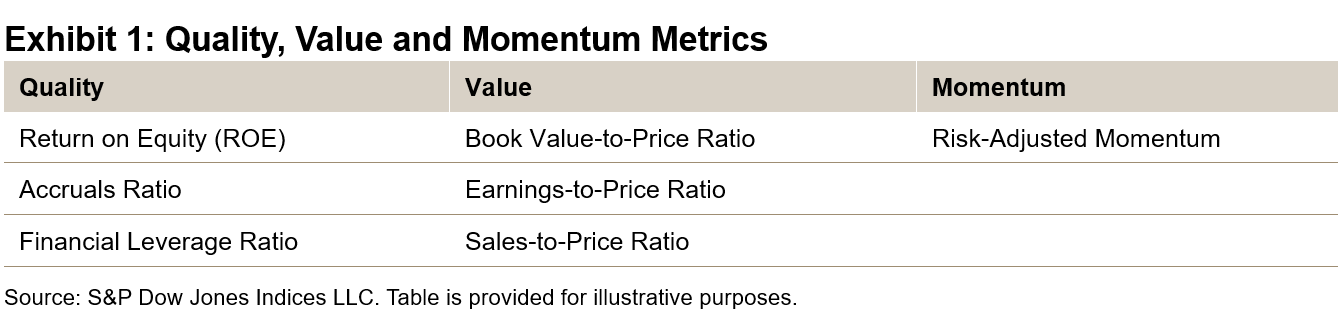

Selected constituents are weighted by the product of their market capitalization and multi-factor score. Exhibit 1 summarizes the metrics used to construct the S&P 500 QVM Multi-Factor Index.

Live Performance of the S&P 500 QVM Multi-Factor Index

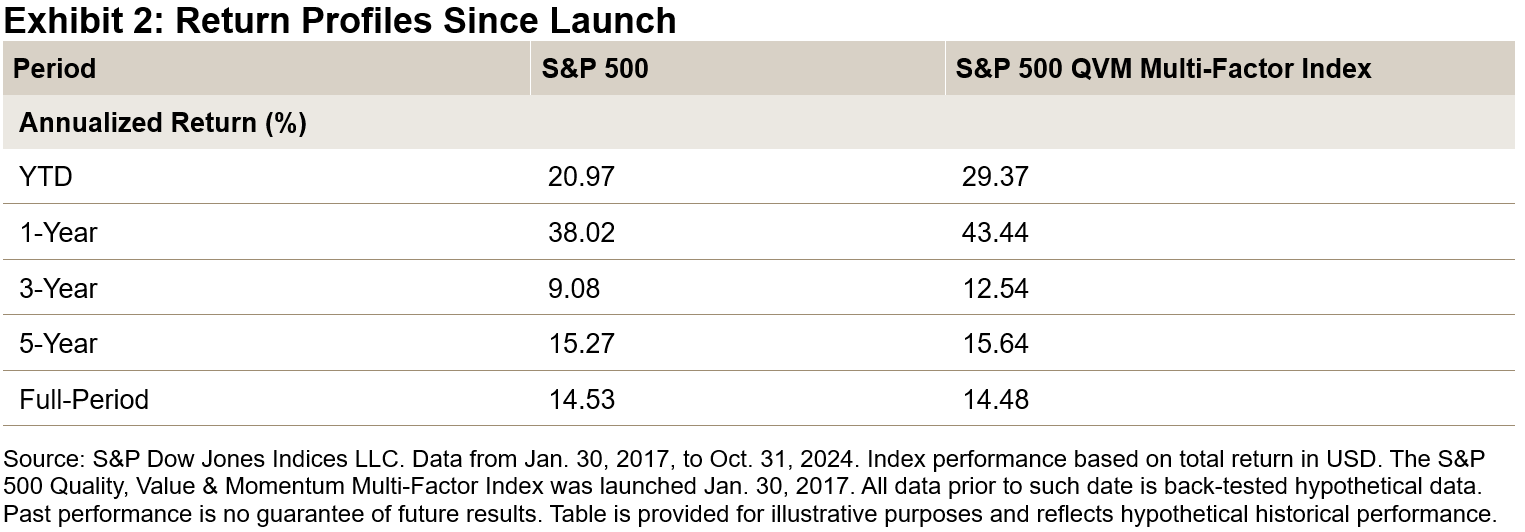

Since its launch date, the S&P 500 QVM Multi-Factor Index has shown strong performance, in line with its benchmark. Notably, its three-year return has exceeded that of the S&P 500 by 3.45% annualized, which is quite remarkable given the recent performance of this large-cap benchmark.

Back-Tested Performance of the S&P 500 QVM Multi-Factor Index

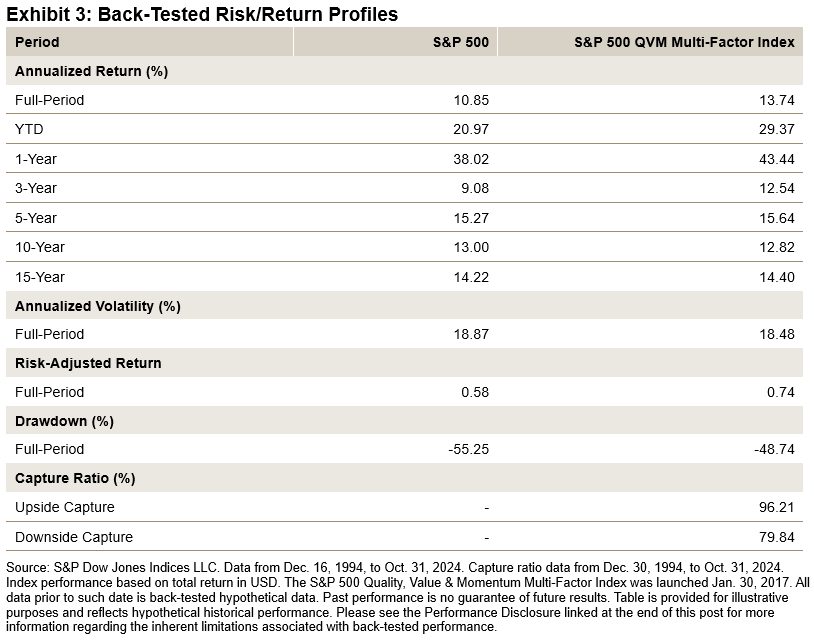

Over the longer term, including back-tested performance, the S&P 500 QVM Multi-Factor Index has outperformed its benchmark both in absolute and risk-adjusted terms. Additionally, the index has exhibited reduced volatility, lower drawdowns and lower downside capture.

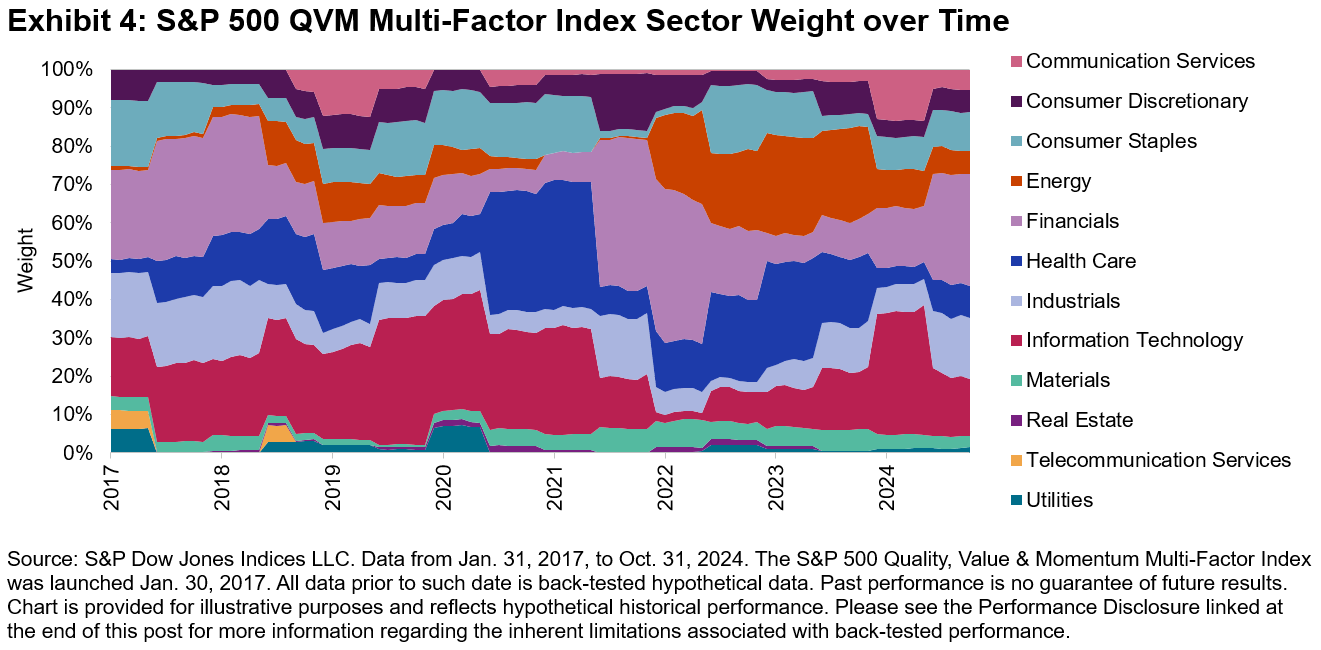

Live Sector Weights of the S&P 500 QVM Multi-Factor Index

Exhibit 4 shows how the sector weights of the S&P 500 QVM Multi-Factor Index have changed over time. On average, the largest sector weights in the index have been Information Technology, Financials and Health Care.

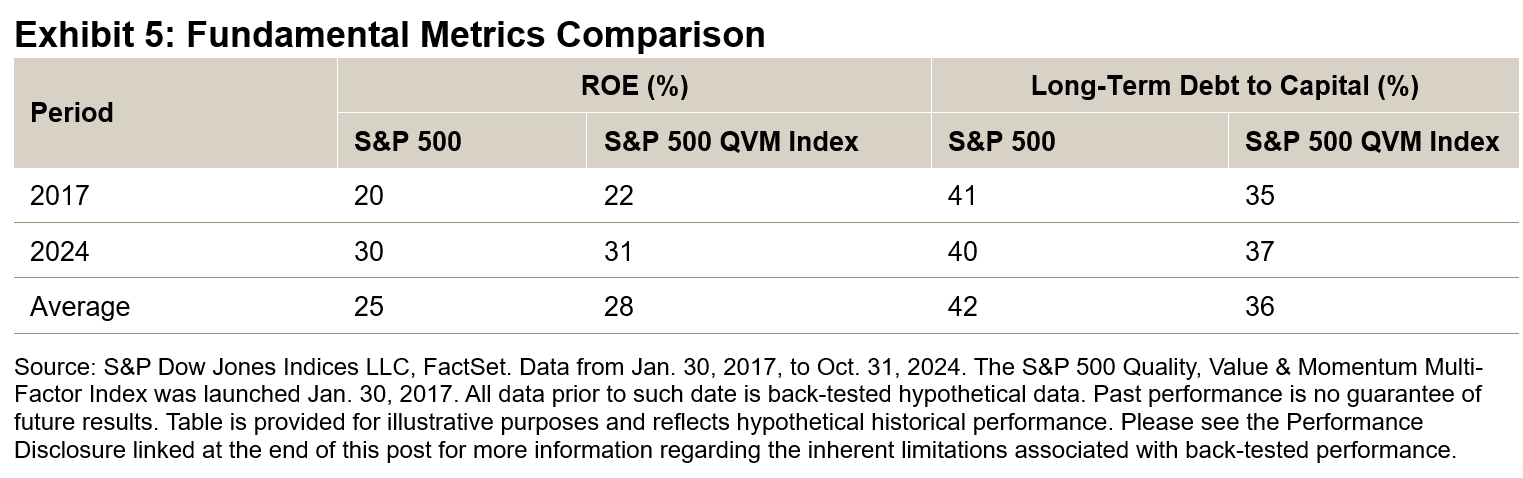

Fundamental Metrics of the S&P 500 QVM Multi-Factor Index

Exhibit 5 shows the ROE and long-term debt to capital metrics of the S&P 500 QVM Multi-Factor Index since its launch. On average, the index has shown a higher ROE and a lower long-term debt to capital ratio compared to its benchmark.

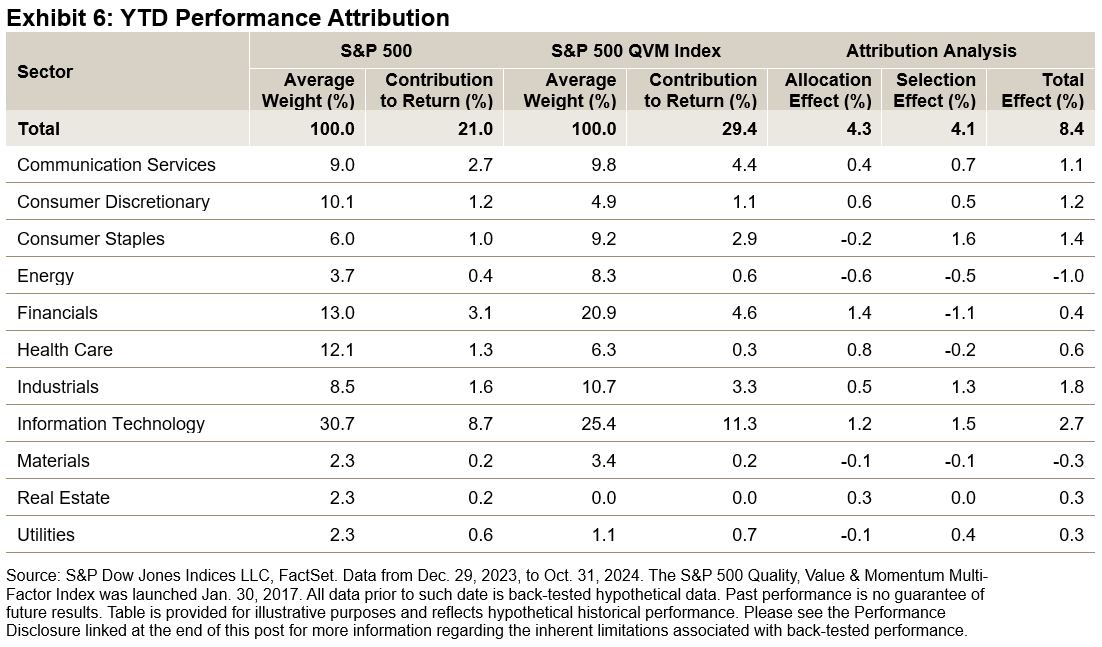

YTD Performance Attribution of the S&P 500 QVM Multi-Factor Index

Exhibit 6 evaluates the YTD performance of the S&P 500 QVM Multi-Factor Index using the Brinson attribution method. It reveals that the recent outperformance can be attributed to both allocation and selection effects, which contributed 4.3% and 4.1%, respectively. Notably, the selection effect played a significant role, showcasing the effect of a bottom-up multi-factor strategy based on a composite of quality, value and momentum factors.

Conclusion

Multi-factor strategies offer an approach to navigating the complexities of selecting and timing individual factors. These strategies have historically led to improved risk-adjusted returns and more stable excess return outcomes, thanks to their diverse factor makeup.

The S&P 500 QVM Multi-Factor Index employs a bottom-up methodology that selects stocks with high average multi-factor scores across quality, value and momentum. Over the long term, the index has beaten the S&P 500, demonstrating significant outperformance over the recent three-year period. With historical benefits such as long-term return outperformance, reduced volatility and enhanced multi-factor exposure, the S&P 500 QVM Multi-Factor Index is a unique index with a diversified factor makeup.

1Innes, Andrew, The Merits and Methods of Multi-Factor Investing,” S&P Dow Jones Indices, April 2018.

The posts on this blog are opinions, not advice. Please read our Disclaimers.