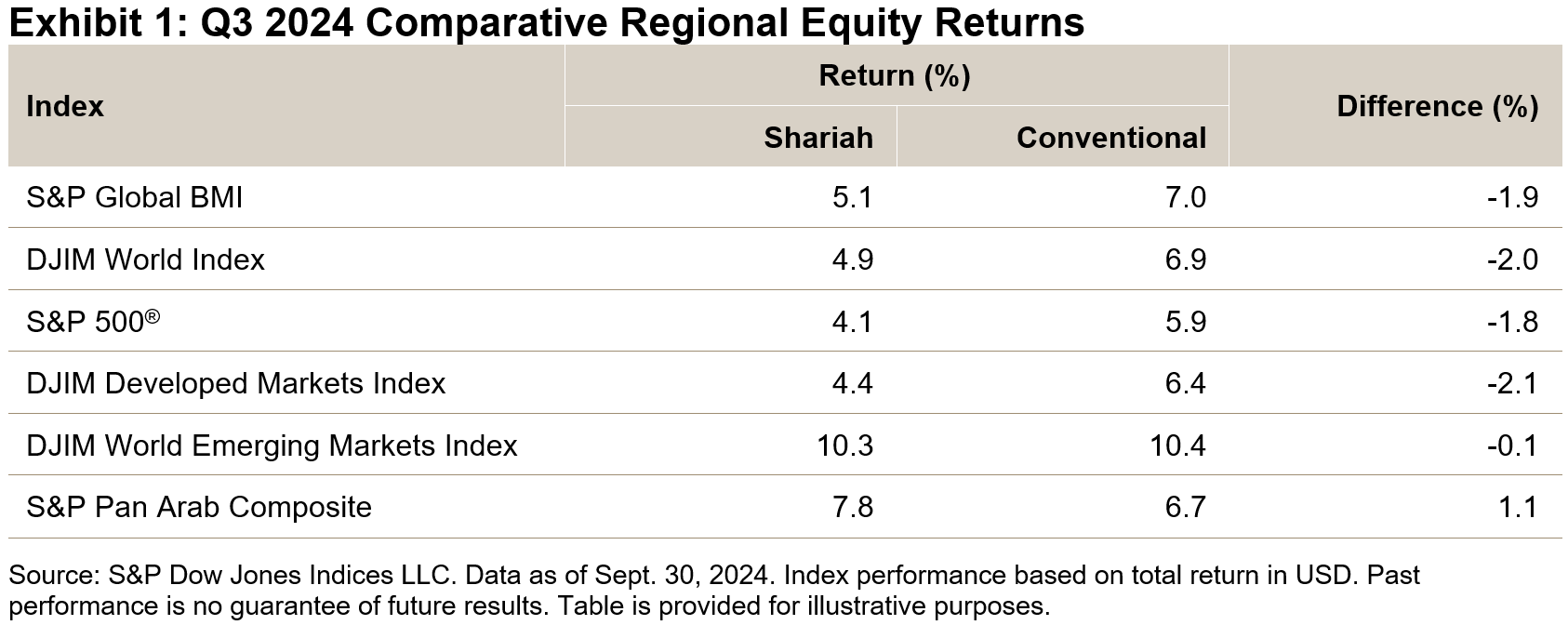

Global equities continued to trend higher in the third quarter of 2024, as central banks in many parts of the world moved to ease monetary policy on the back of moderating inflation. The S&P Global BMI rose 7.0% for the quarter and was up 18.1% YTD. Emerging market regions drove the market up, with an impressive 10.4% return, almost catching up with the performance of developed market regions YTD. MENA equities also turned around and joined in the global upward trend, with the S&P Pan Arab Composite rising 6.7%, led by UAE (up 11.9%) and Qatar (up 9.3%).

Meanwhile, Shariah-compliant global equity benchmarks fell short of their conventional counterparts; the S&P Global BMI Shariah and Dow Jones Islamic Market (DJIM) World Index both underperformed by about 2% in Q3 2024, narrowing their excess returns versus conventional benchmarks to 0.5% YTD (see Exhibit 1).

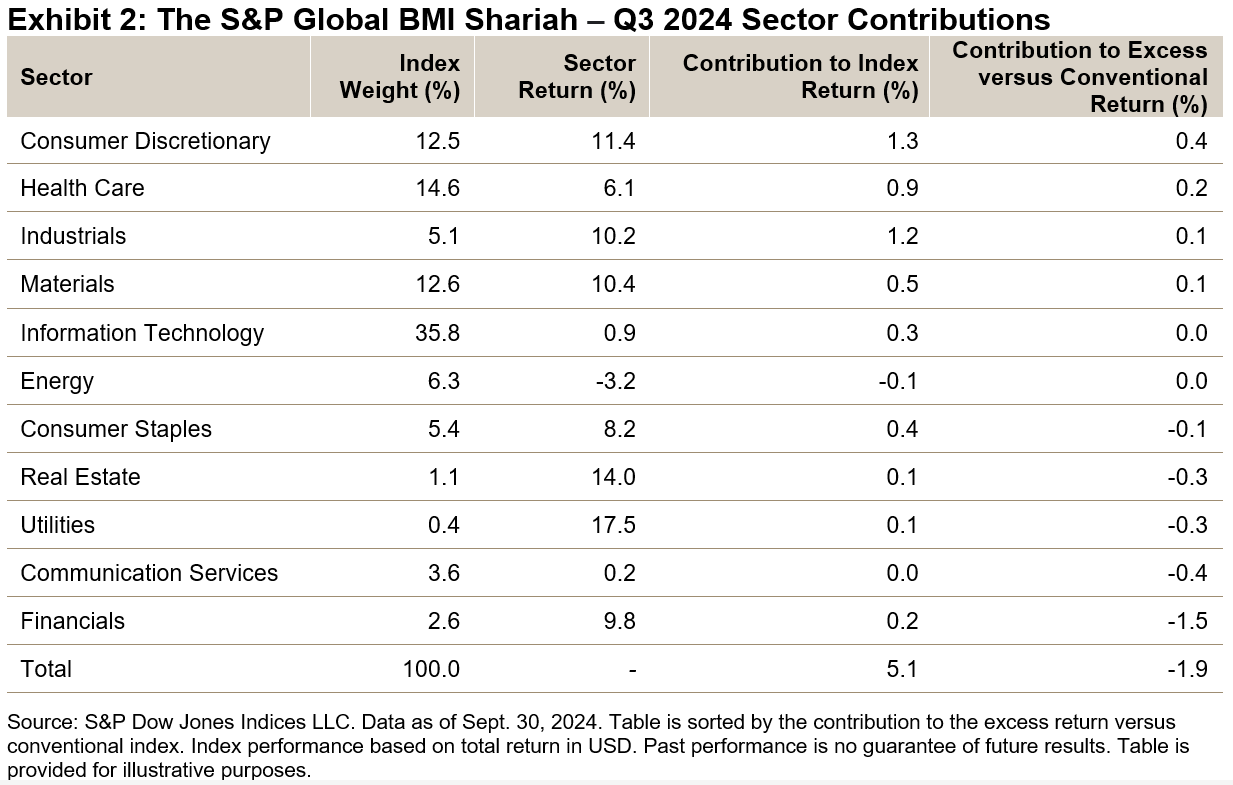

Drivers of Shariah Index Performance in Q3 2024

While the global equity market continued its upward trend into the third quarter, there were notable rotations underneath the surface. In contrast to the first half of 2024, which was characterized by the outperformance of large-cap Information Technology and Communication Services companies, the market strength broadened across smaller companies and other sectors in Q3, including Financials in particular. In more detail, a full 1.5% of the 1.9% return differential between the S&P Global BMI and S&P Global BMI Shariah was due to the latter’s relative underweight in the Financials sector, as shown in Exhibit 2. Communication Services also contributed negatively, as within the sector, Shariah-compliant, large-cap Media & Entertainment companies underperformed the non-compliant, indebted Telecommunication Services companies. Utilities, which was among the best-performing sectors in Q3, also contributed to the underperformance of the shariah indices through its reduced weightings.

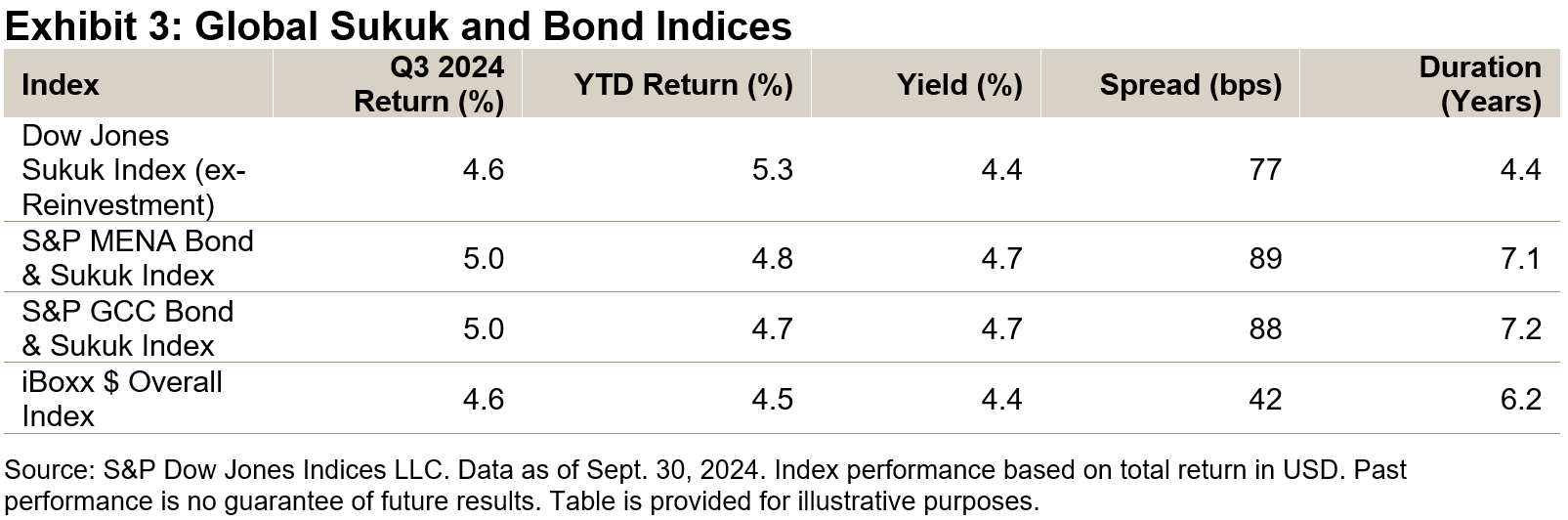

Global Sukuk Rallied in Q3 2024

Fixed income markets witnessed a strong rally on the back of the global rate cycle taking a sharp turn downward. U.S. dollar-denominated investment grade bonds, as measured by the iBoxx $ Overall Index, and its sukuk equivalent—the Dow Jones Sukuk Index (ex-Reinvestment)—both gained 4.6% in the third quarter, as a larger compression in credit spreads offset the lower duration of sukuk. The sukuk benchmark’s yield fell to 4.4%, with a spread of 77 bps over the U.S. Treasury bonds, as of the end of September 2024.

This article was first published in IFN Volume 21 Issue 44 dated October 30, 2024.

The posts on this blog are opinions, not advice. Please read our Disclaimers.