The financial landscape has transformed significantly in recent years, with market participants increasingly recognizing the value of sustainability characteristics. One embodiment of this shift is the S&P 500® ESG Leaders Index, launched on Feb. 7, 2022, which is a best-in-class ESG index designed to measure the performance of securities with stronger than average ESG characteristics, while excluding those with controversial business activities that have negative social or environmental impacts.

The S&P 500 ESG Leaders Index outperformed the S&P 500 over the past one- and two-year periods in annualized terms, while maintaining a tracking error of 2.0% (see Exhibit 1). Understanding the nuances behind this outperformance requires a critical analysis of the factors at play—specifically stock selection and sector weighting, akin to our earlier research1 on the S&P 500 ESG Index.

![]()

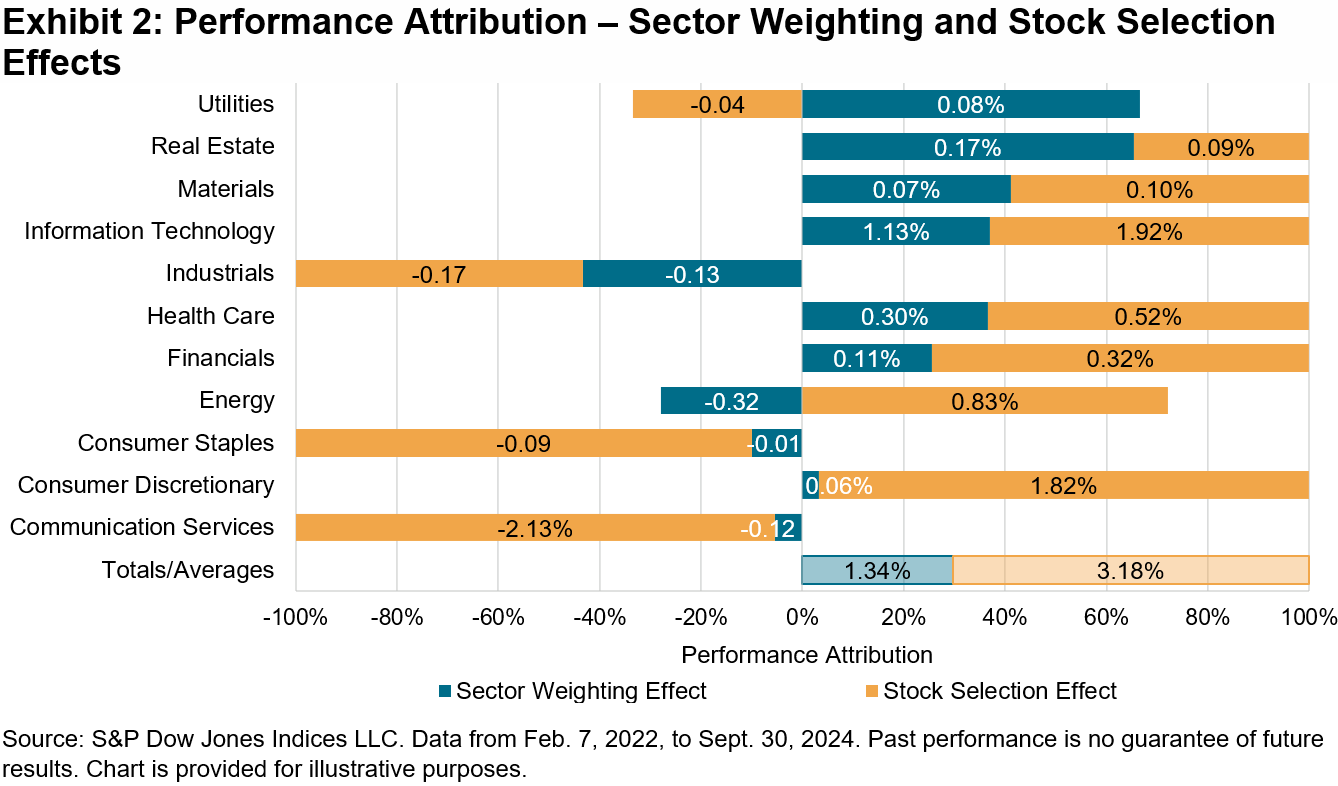

Exhibit 2 provides insights via a Brinson2 attribution framework, allowing us to quantify sector contributions to the S&P 500 ESG Leaders Index’s excess return relative to the S&P 500. To emphasize the relative impact of sector weighting and stock selection effects, Exhibit 2 shows the proportion of the total impact (so that their absolute values sum to 100%), with the actual return impact shown in the labels. The findings suggest that the outperformance of the S&P 500 ESG Leaders Index was predominantly driven by stock selection effects rather than sector weighting. Nearly 71% of the outperformance can be attributed to the stock selection effect, underscoring the index’s strategic focus on maintaining sector neutrality.

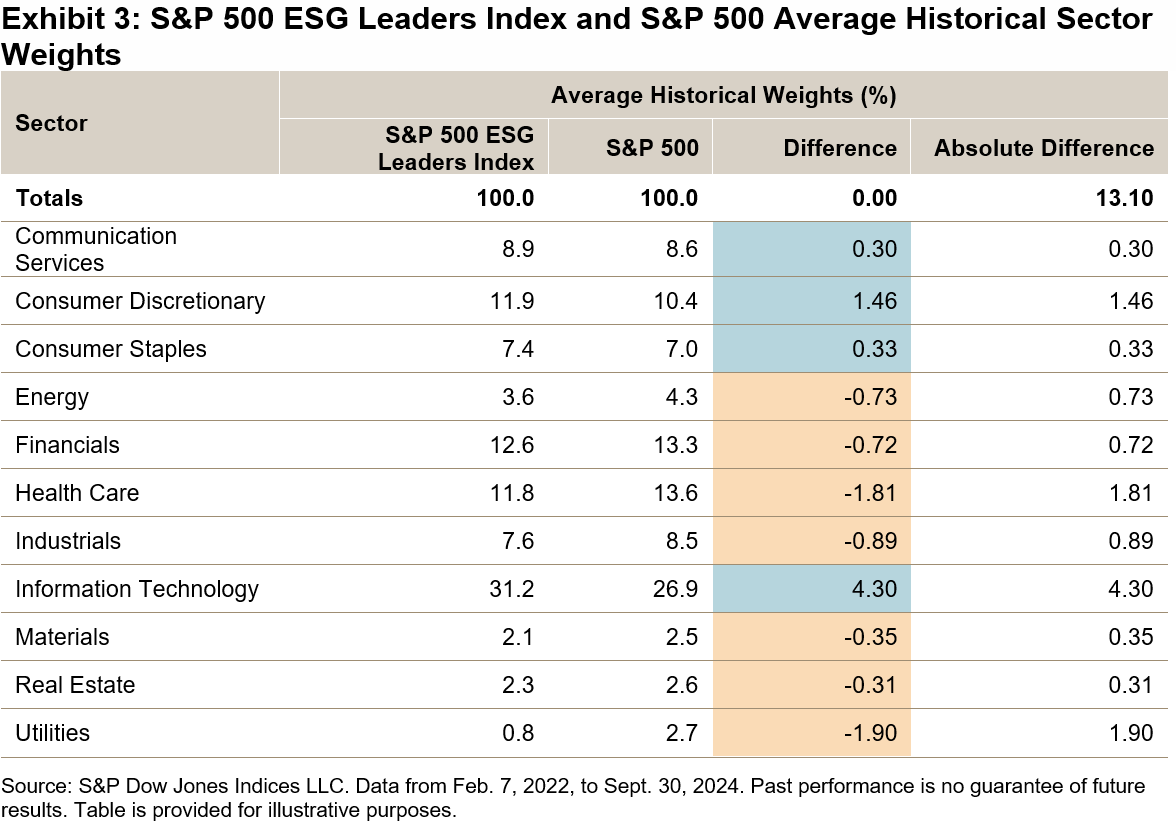

Diving deeper into sectoral effects, the analysis reveals that out of the 11 sectors included in the framework, only Utilities and Real Estate exhibited sector weighting effects that outpaced stock selection effects (see Exhibit 2). Furthermore, the average historical sector weights for the S&P 500 ESG Leaders Index and their differences from the S&P 500 are summarized in Exhibit 3.

The observations in Exhibits 2 and 3 underscore an important achievement for the S&P 500 ESG Leaders Index—it achieved a notable degree of sector neutrality compared to the S&P 500, thus helping to mitigate the risk associated with over-concentration in particular sectors. For market participants aiming to incorporate sustainability into their investment strategies, this level of sector neutrality can be attractive as it may contribute to minimizing tracking differences and maintaining a similar sector-risk profile.

With an increasing emphasis on sustainability, understanding how sustainability-focused indices can perform in relation to broad market benchmarks is essential. The S&P 500 ESG Leaders Index shows how a sustainability-focused index can adhere to a degree of sector neutrality and have similar performance to the S&P 500. Further studies and insights into various sustainability indices can be explored through S&P Dow Jones Indices’ Sustainability Index Dashboard, enriching our understanding of this significant shift in investment paradigms.

1 For a thorough analysis of the outperformance of the S&P 500 ESG Index compared to the S&P 500, see Beyhan, Maya, “Charting New Frontiers: The S&P 500 ESG Index’s Outperformance of the S&P 500,” S&P Dow Jones Indices LLC, Sept. 06, 2024.

2 For more information on this widely used performance attribution model, see Brinson, Gary P., Hood, L. Randolph, Beebower, Gilbert L., “Determinants of Portfolio Performance,” Financial Analysts Journal, July-August, 1986.

The posts on this blog are opinions, not advice. Please read our Disclaimers.