The Global Industry Classification System (GICS®) celebrated its 25th birthday in August 2024. Jointly maintained by S&P Dow Jones Indices (S&P DJI) and MSCI, GICS offers a common way to talk about market segments and their respective performances.

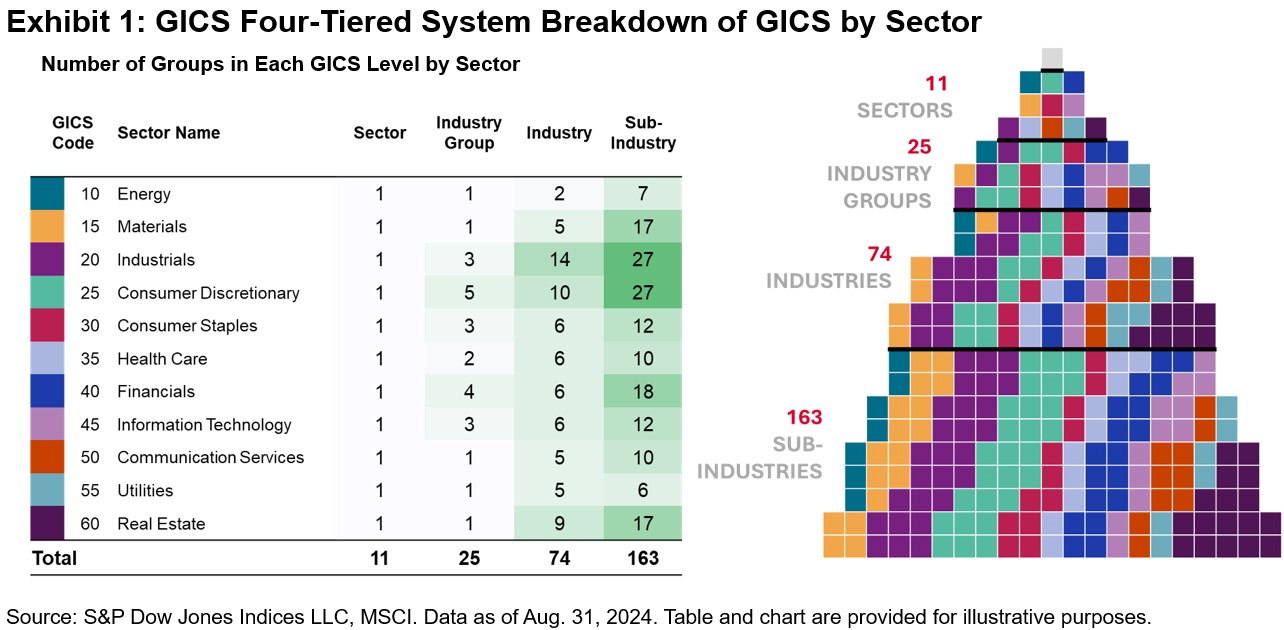

GICS primarily uses revenues to group companies according to their principal business activities, with earnings and market perception among other factors that are also considered. Each company is assigned to one of the more than 160 sub-industries, which then determines—in decreasing granularity—its industry, industry group and sector classifications. Exhibit 1 provides an overview of the latest GICS structure.

Grouping companies by their principal business activities means that companies in the same sector typically have shared sensitivities to common drivers of returns and macroeconomic variables. Crucially, though, these sensitivities may differ across sectors. Hence, sector-based perspectives may be relevant for market participants looking to implement sectors in either active or passive portfolio construction, or both.

Sectors and the detailed GICS framework allow for attribution analysis for broad-based benchmarks like the S&P 500® to determine which segments are leading or lagging and how they impact returns.

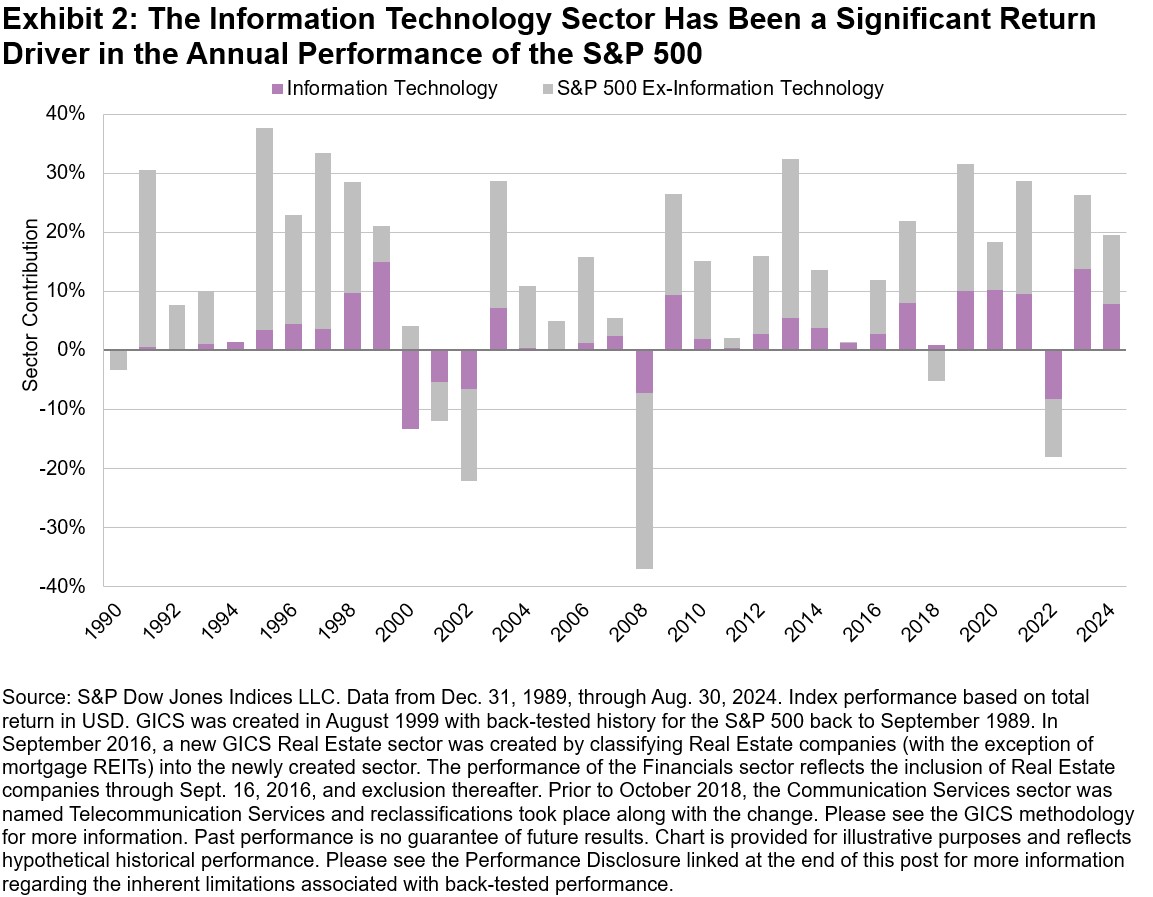

Exhibit 2 provides a full breakdown of the contribution of the IT sector to the S&P 500’s calendar year performance since the 1990s. Amid investors’ recent focus on the anticipated impact of artificial intelligence on IT companies’ growth prospects, IT has accounted for 40% of the S&P 500’s performance so far in 2024. In contrast, IT was a relatively nascent sector in the early 1990s, explaining why Technology had little to no impact on the S&P 500’s annual returns.

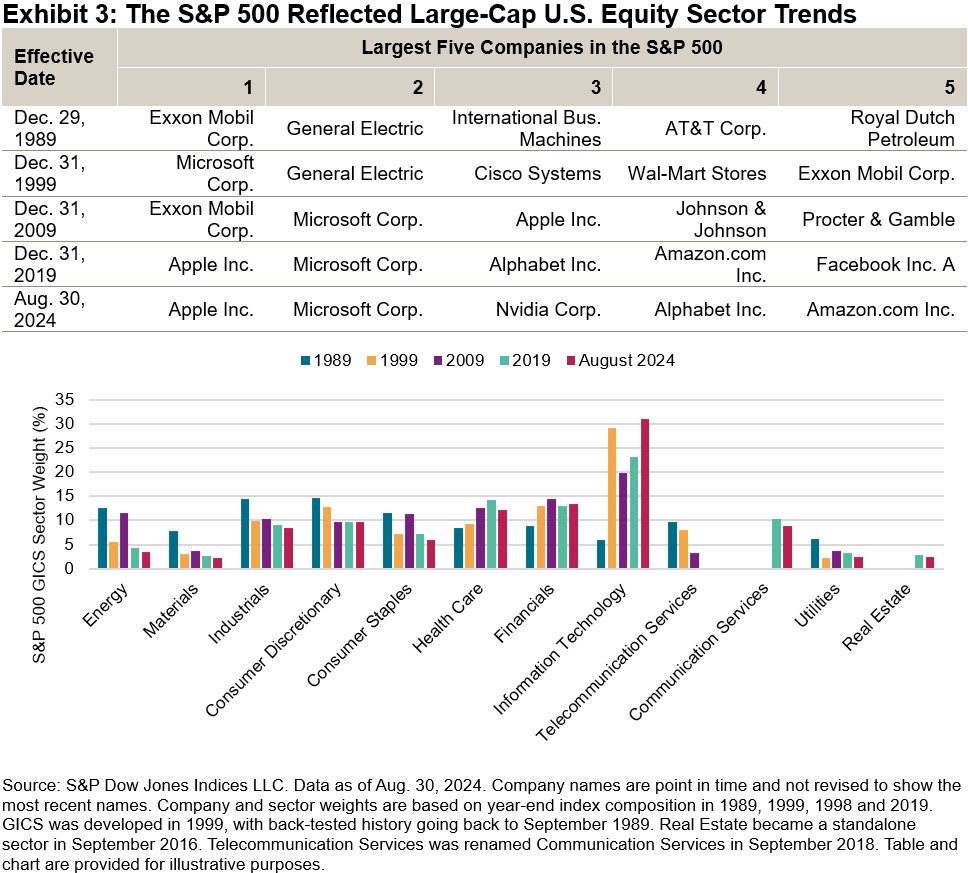

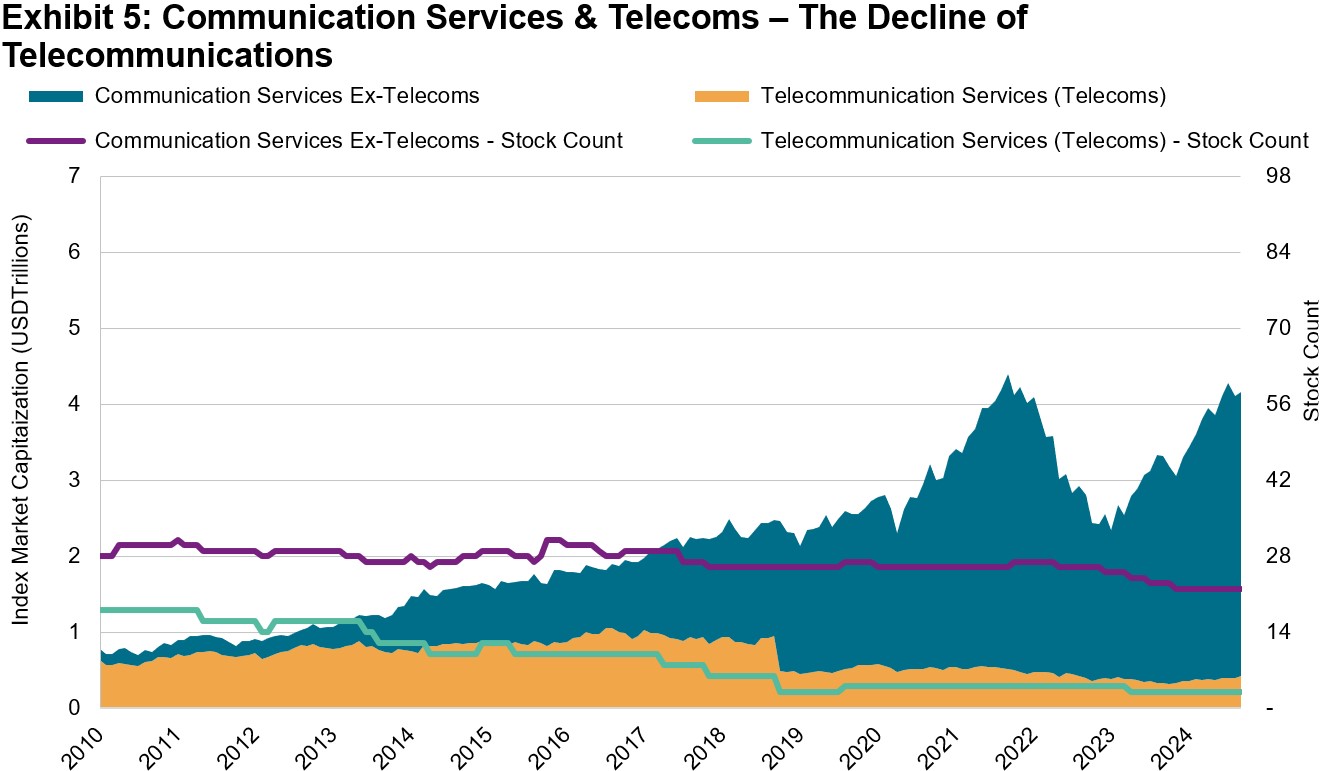

Exhibit 3 shows the evolution of the largest companies in the S&P 500, as well as the index’s GICS sector weights, which reflect the increased importance of Information Technology companies and the decline of traditional/old economy sectors such as Energy, Industrials and Telecommunication Services.

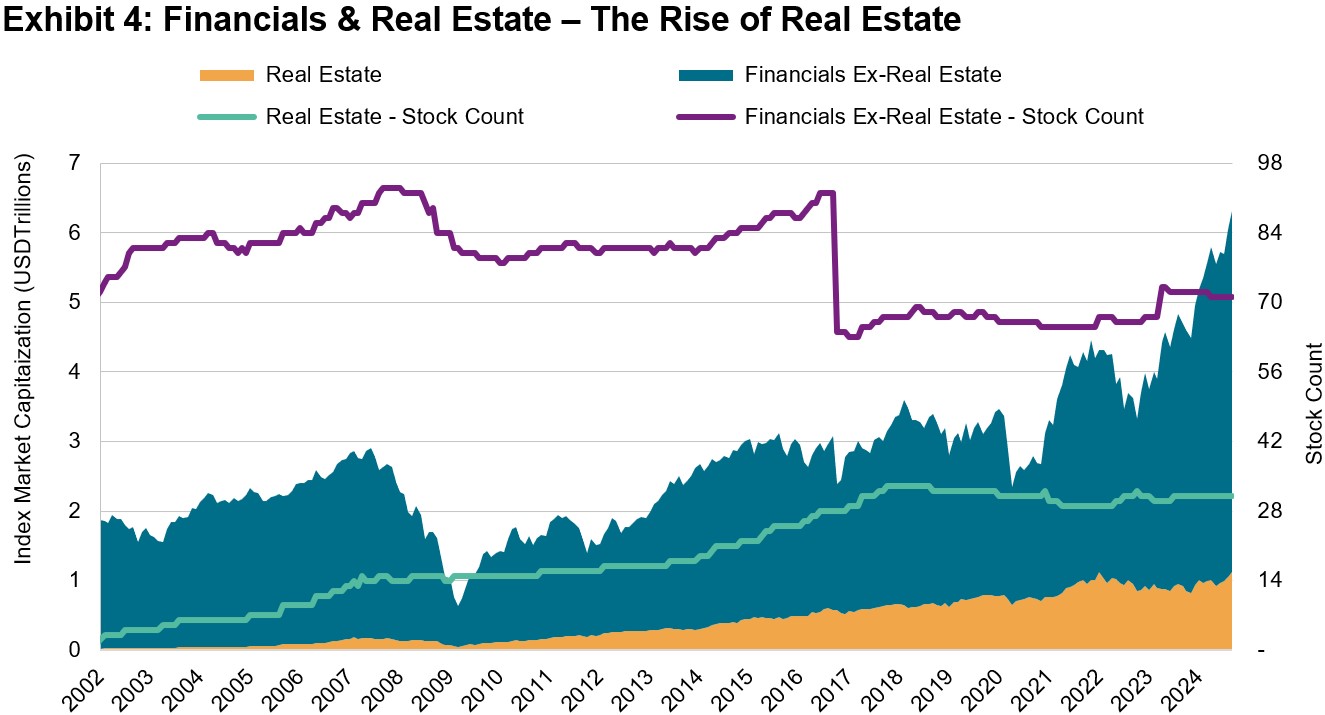

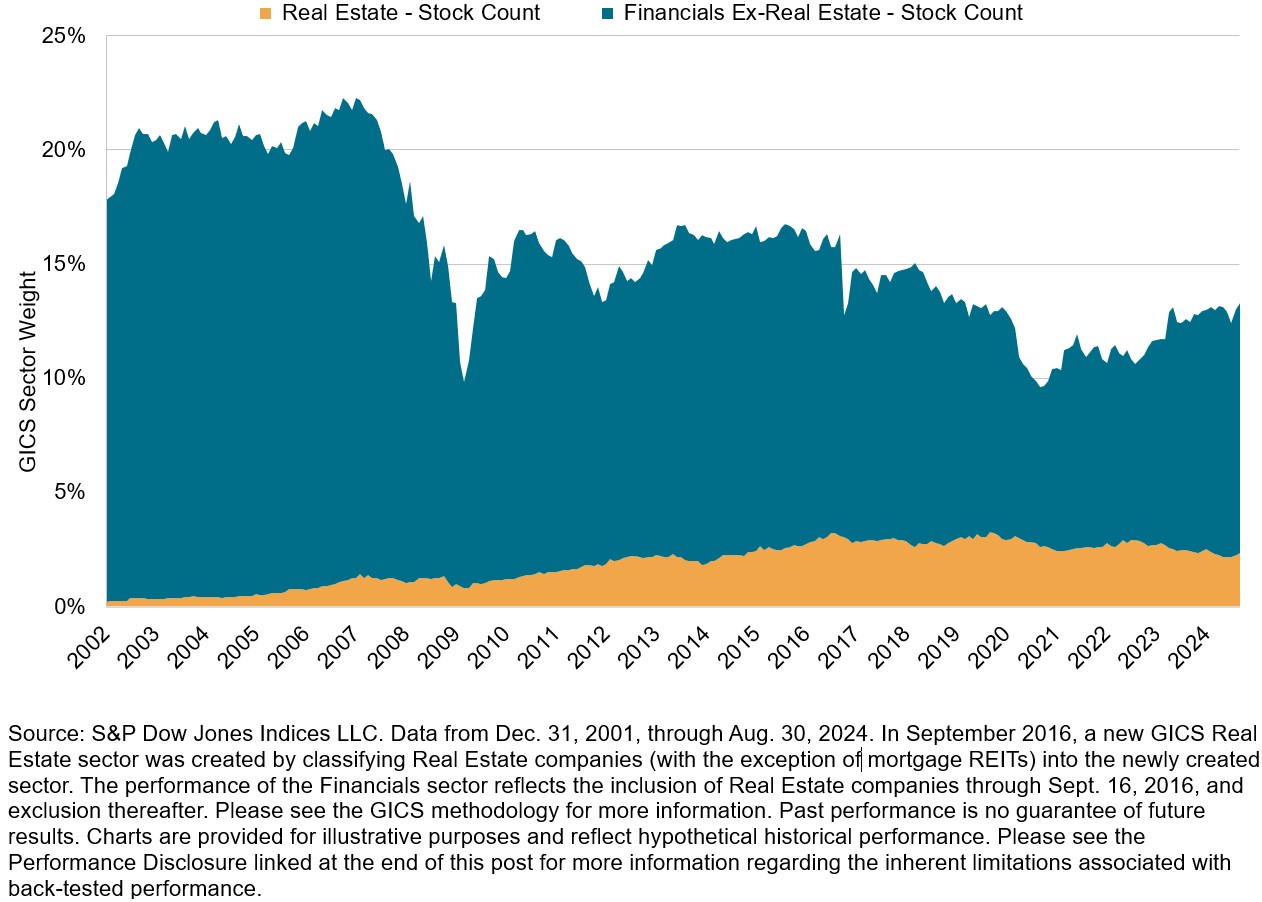

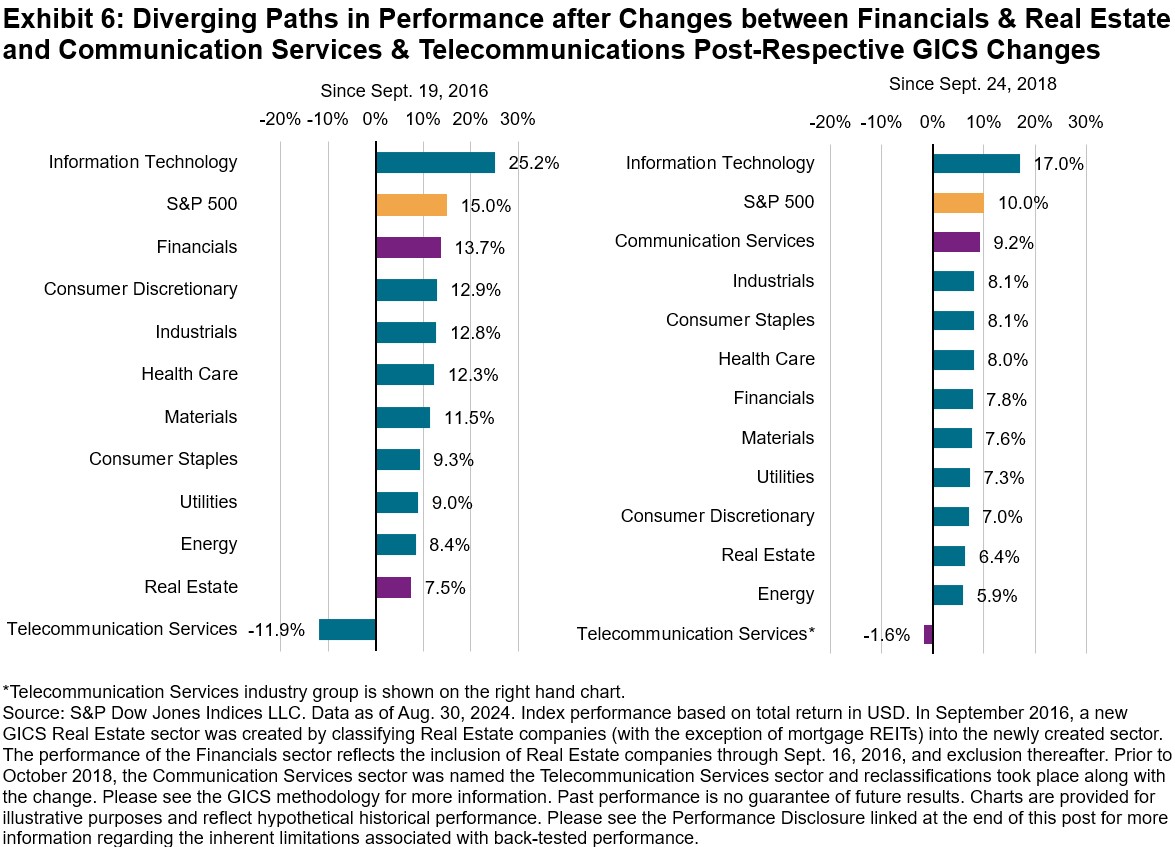

GICS is not a static structure: There have been several changes over time to reflect the market evolutions. One of the largest changes came in 2016 when Real Estate became a standalone sector; previously it was part of Financials. This change reflected growing representation of real estate investment trusts (REITs) and the distinct characteristics of Real Estate companies compared to the rest of the Financials sector.

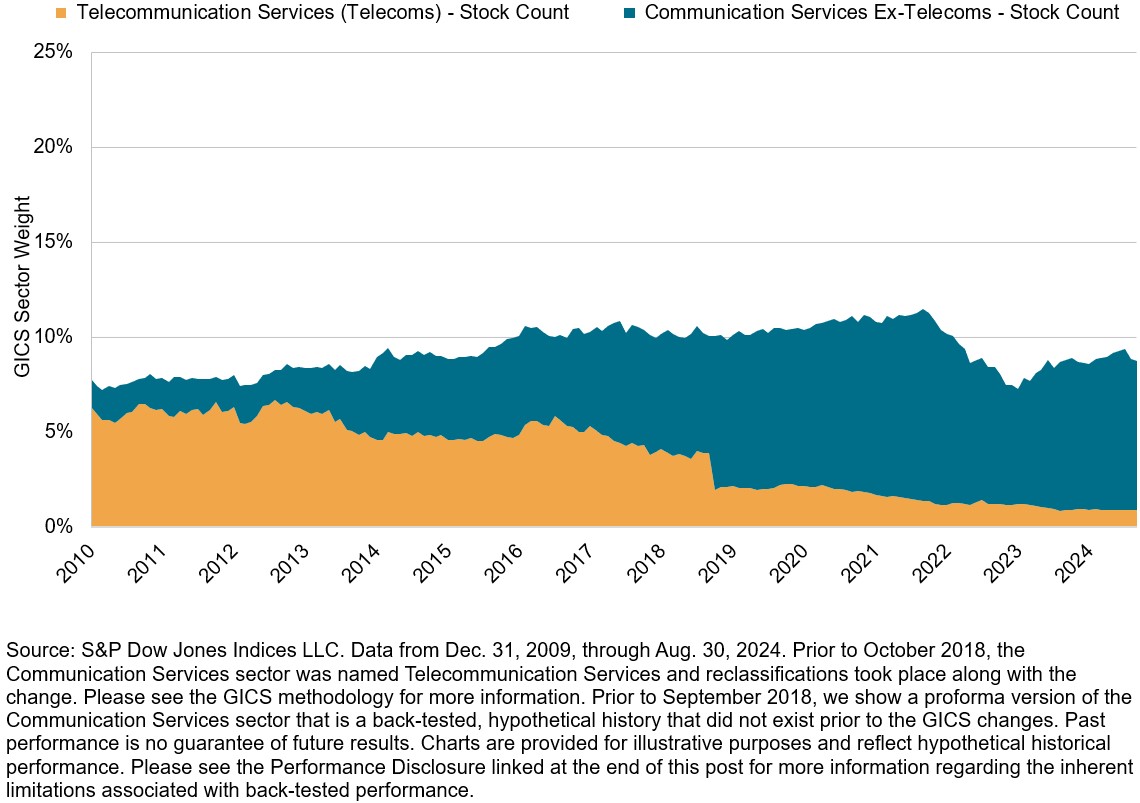

Another key change came in 2018, when the Telecommunication Services sector was renamed Communication Services and various companies were moved across the GICS structure. This was in response to changes in the ways people communicate: from telephone to email, text and social media.

When we look at the performance of these new and old sector segments, we can see clear distinctions in performance, between Financials and Real Estate as well as Communication Services and Telecommunications, as shown in Exhibit 6.

While we looked at the S&P 500 in this blog, the power of GICS is that similar analysis can be performed on any broad-based index across different markets. Looking at several emerging and frontier markets, we can see that “old economy” sectors such as Financials and Real Estate still dominate local indices, exhibiting potential opportunities for diversification with U.S. equity sectors.

GICS remains an effervescent tool for a range of market practitioners and reflects today’s trends. GICS also has the flexibility to adapt and change over time, as seen with the 2016 Real Estate and 2018 Communication Services transformations. Here’s to the next 25 years and beyond!

The posts on this blog are opinions, not advice. Please read our Disclaimers.