First published in 2002, the S&P Indices versus Active (SPIVA®) U.S. Scorecard measures the performance of active mutual fund managers against their respective S&P DJI benchmarks over various time horizons and across asset classes. In 2015, we extended the analysis to include institutional accounts to understand how institutional asset owners fared versus mutual funds against their respective benchmarks and the impact of fees on performance.

In our 2023 edition, we have further expanded our purview of assessing active manager performance to now include separately managed accounts (SMAs)/wrap accounts. SMAs may offer potential benefits such as increased customization, greater transparency and direct ownership of securities in a portfolio. With the addition of these accounts, we can examine the performance of professionally managed portfolios held by retail investors against their respective benchmarks.

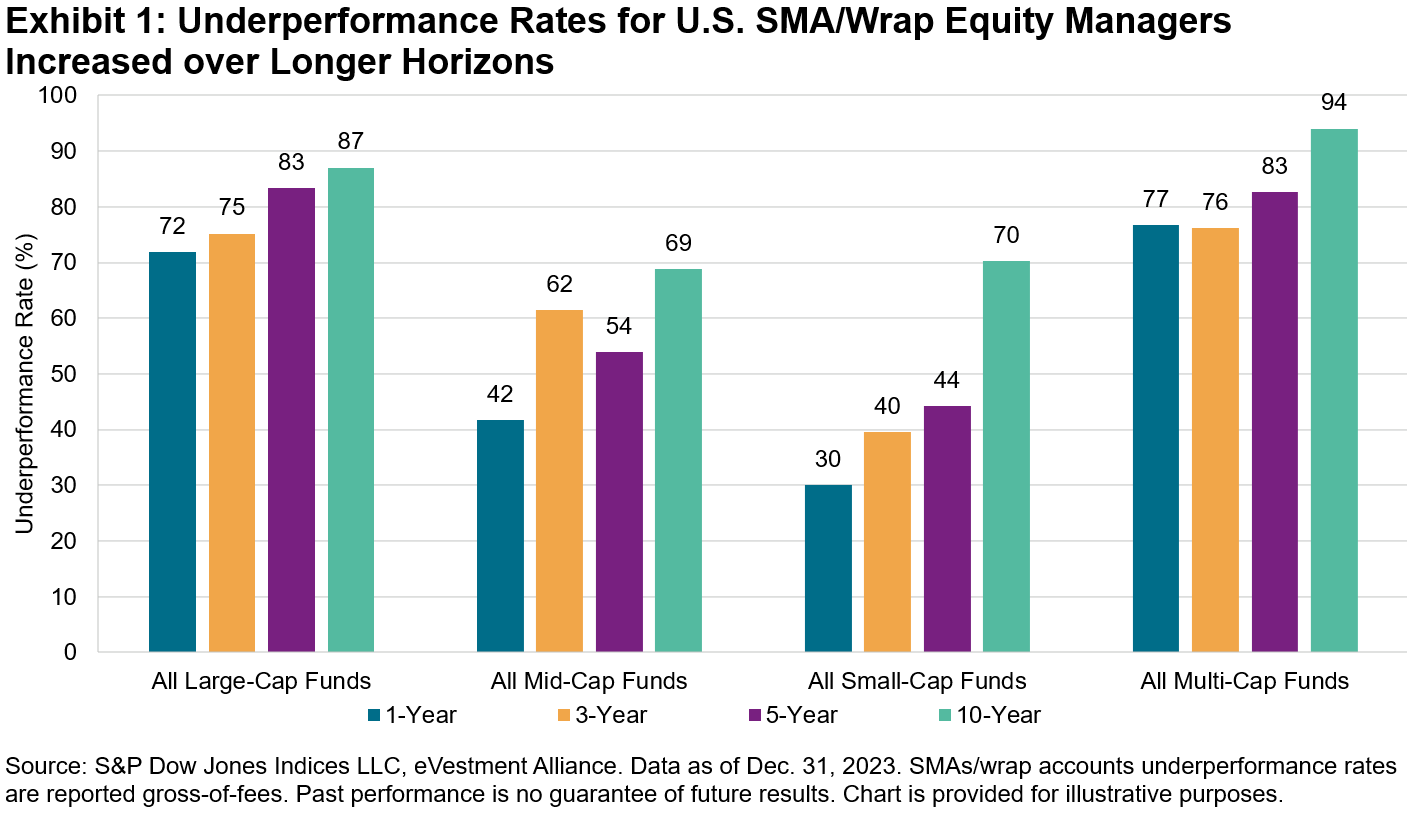

Our reported SMA/wrap categories span across equities and fixed income. In 2023, in our most closely watched category of All Large-Cap Funds, 72% of SMA/wrap managers underperformed the S&P 500® on a gross-of-fees basis, lagging their institutional account and mutual fund peers (see Exhibit 1). Large-cap managers may have been hampered by the dominance of mega-cap stocks, especially if they were underweighted in comparison to their benchmark weights.

In contrast, mid- and small-cap managers fared much better. Only 42% of mid-cap and 30% of small-cap managers underperformed their respective benchmarks. One potential explanation for these results may be style bias opportunities among smaller-cap managers, who may have benefited by taking strategic tilts toward outperforming larger-cap stocks, with the S&P 500 outperforming the S&P MidCap 400® and the S&P SmallCap 600® by 9.9% and 10.2%, respectively.

Style bias often explains performance across the capitalization spectrum; it may be easier for small- and mid-cap managers to tilt their portfolios toward larger companies with greater liquidity or to let their winners run. Historically, the odds of success for mid- and small-cap managers have improved when larger stocks have outperformed, with majority outperformance for small-cap mutual funds in 7 out of the past 22 years, of which 6 years coincided with large-cap outperformance.

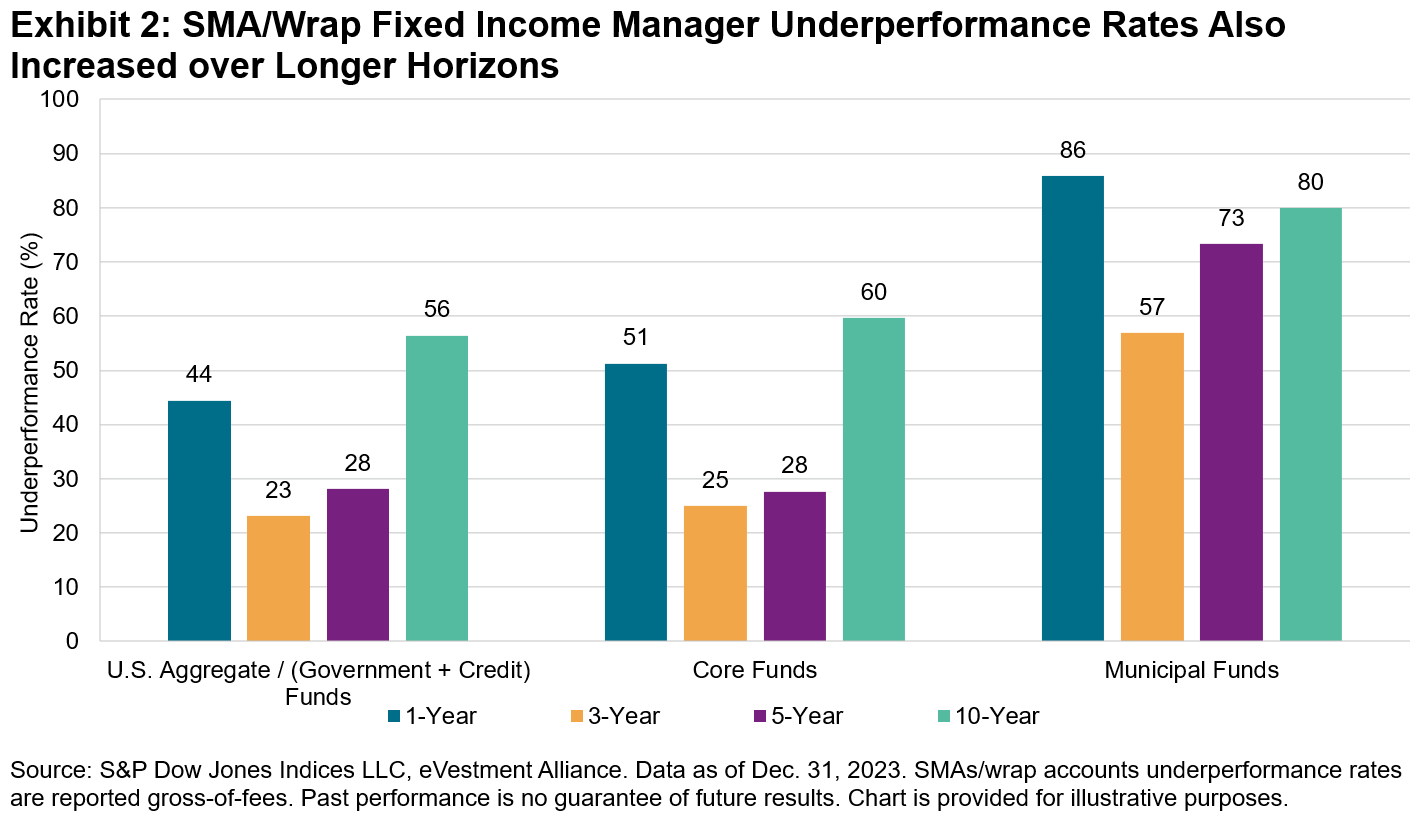

SMA/wrap results within fixed income were mixed in 2023 across our three reported categories (see Exhibit 2). U.S. Aggregate accounts posted majority outperformance, followed by a moderate showing for Core, with 51% of accounts underperforming, and bleaker results within the muni space, with 86% of Municipal accounts underperforming the S&P National AMT-Free Municipal Bond Index.

While there were a few categories with majority outperformance in 2023, our SPIVA scorecards have consistently shown that outperforming a benchmark over time is challenging, and this continues to ring true for SMAs/wrap accounts. Exhibits 1 and 2 show that more than 70% of accounts across equity SMA/wrap categories and more than 50% across fixed income categories underperformed their respective benchmarks over the 10-year period ending Dec. 31, 2023. For more detailed information on how SMAs/wrap accounts fared last year, please see our 2023 SPIVA Institutional Scorecard.

The author would like to thank Anu Ganti and Davide Di Gioia for their contributions to this post.

The posts on this blog are opinions, not advice. Please read our Disclaimers.